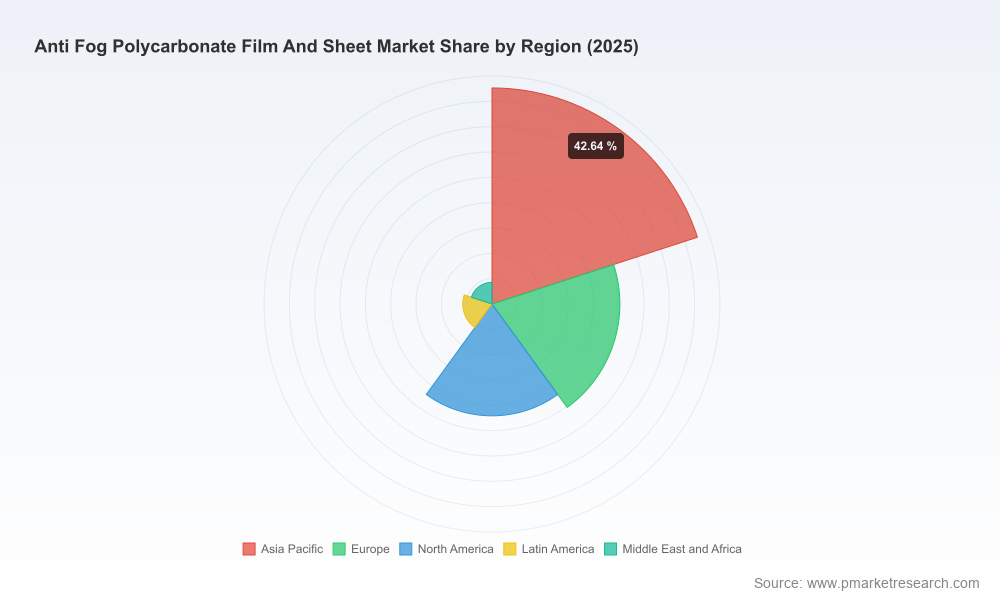

Anti Fog Polycarbonate Film And Sheet Market — Strategic Outlook for 2026: An Executive Preview

Why this preview matters for 2026 corporate decision-making

As companies re-evaluate supply chains, product differentiation, and regulatory exposure going into 2026, the anti-fog polycarbonate film and sheet market is presenting a rare combination of steady demand growth and concentrated innovation risk. PW Consulting’s latest study benchmarks the market against a robust historical run and a clear forward path: the global market expanded from a resilient base in 2020 and reached approximately USD 194.5 Million in 2025, and our base-case forecast delivers a compound annual growth rate of 5.45% across the 2026–2032 horizon, with a projected market size approaching USD 282.0 Million by 2032.

Anti Fog Polycarbonate Film And Sheet Market

These topline dynamics – steady mid-single-digit CAGR and visible capacity investments – make 2026 a strategic hinge year. Executives who use data-driven scenario planning, supply-side reconfiguration, and targeted product innovation plans now will minimize disruption and capture disproportionate share as demand for durable anti-fog performance accelerates in safety, medical, agricultural, and selected industrial applications.

Anti Fog Polycarbonate Film And Sheet Market

What PW Consulting’s report delivers to support boardroom and commercial decisions

- Actionable market sizing and scenario models: bottom-up sizing for 2020–2025, and three forward scenarios for 2026–2032 (base, downside, and accelerated adoption), all delivered with downloadable model templates and sensitivity levers.

- Demand-driver mapping: quantified trigger points for the medical/safety visor segment, greenhouse & architectural glazing, automotive interior applications, and specialty electronics markets, with adoption curves and lead indicators by quarter.

- Supply-chain and cost-stack analysis: raw-material sensitivity (with stress tests for bisphenol A feedstock volatility driven by phenol/acetone markets), coating chemistry cost impacts, and recommended procurement hedging approaches.

- Regulatory and product compliance playbook: timelines and impact matrices for recent REACH/POP-style additions (including new listing criteria and concentration limits), PFAS-free transition strategies, and country-level tariff exposure scenarios.

- Competitive capability matrix and partner shortlist: capability mapping across global converters, specialty coaters, resin suppliers, and coating formulators; supplier scorecards for technical performance, capacity, quality systems, and ESG readiness.

- Go-to-market and product roadmaps: differentiated commercial plays for OEMs versus distributors, conversion guidelines for retrofit and OEM integration, and sample commercial contracts (RFPs, quality annexes, and price‑escalation clauses).

- M&A and investment screen: prioritized acquisition targets, integration risk checklists, and expected deal-return windows under multiple pricing and demand scenarios.

- Operational playbooks: capex calculators for coating and co-extrusion lines, plant siting decision matrix (including proximity to demand and tariff exposure), and a 90/180/360-day implementation checklist for scaling or entry.

Competitive landscape: who matters and why

The market sits at a moderate concentration level: the top three suppliers account for a meaningful portion of global supply while the top five push aggregate share further, creating a landscape where scale, formulation capability, and coater relationships are decisive. PW Consulting’s competitive analysis synthesizes public product portfolios, recent capacity moves, and proprietary supplier interviews to map strategic options for buyers and investors.

Anti Fog Polycarbonate Film And Sheet Market

- Polyvantis (formerly SABIC Innovative Plastics) — a technology leader with established coated LEXAN™ anti-fog grades engineered for long-term performance in high-humidity PPE and display applications. Strengths: global material know-how, high-performance grade availability, and established OEM relationships.

- FSI Coating Technologies (SDC division) — a coatings specialist driving chemical-formulation differentiation. Recent launches (notably PFAS-free formulations) show how coating chemistry can become a competitive moat for high-value end uses.

- Brett Martin / American Polycarbonate Company — capacity expansion initiatives in North America signal supply-side rebalancing that will affect lead times and logistics economics for multiwall and corrugated products in 2026 and beyond.

- Covestro, Mitsubishi Gas Chemical, Teijin — material innovators developing differentiated film and sheet grades optimized for coatings, optical clarity, and thermal performance; their roadmaps matter for premium automotive and display applications.

- China-based manufacturers (e.g., Excelite, UVPLASTIC, WeeTect, UNQ, WeProFab, G-Crystal) — competitive on price and nimble on custom fabrication and local regulatory adaptation; important partners for scale and regional projects but variable on consistency and long-term warranty offerings.

- Plaskolite, Palram — converters with broad distribution networks and product families suitable for architectural, signage, and certain industrial segments where service and availability trump unit-cost competition.

PW Consulting’s report includes a supplier-fit matrix that aligns each named player to use-case archetypes, contract levers, and integration risk. It also flags which players are best-positioned to support OEMs seeking PFAS-free pathways and which will struggle under stricter POP-style regulatory regimes.

Regulatory, raw-material, and market drivers shaping 2026 choices

- Raw-material cost dynamics: Polycarbonate feedstock volatility – driven by upstream phenol/acetone cycles and bisphenol A price moves – remains a principal margin pressure. Procurement teams should adopt indexed contracts and scenario hedges now to avoid reactive spot purchases when demand spikes.

- Regulatory shifts: New POP-style listings and chemical concentration limits are re-shaping formulation choices. Firms should evaluate coatings and additive choices against near-term concentration limits and available derogations for certain vehicle applications to avoid costly late-stage redesigns.

- Coating chemistry evolution: The market is seeing accelerated adoption of PFAS-free and durable hydrophilic coatings; suppliers introducing validated alternatives now hold a first-mover advantage in many institutional procurement processes.

- Trade and tariff exposure: Changes to tariff regimes increase the value of regional production and local inventory strategies. Organizations should model landed-cost impacts by scenario and prioritize nearshoring or regional partnerships where economics and lead times justify investment.

Strategic implications and recommended 2026 plays

PW Consulting translates market dynamics into clear strategic imperatives tailored to three primary stakeholders:

- OEMs and large institutional buyers: Lock in multi-year supply agreements with dual-sourced suppliers, specify validated PFAS-free coating options in contracts, and require durability performance warranties tied to application-specific test protocols.

- Converters and coating houses: Invest selectively in PFAS-free chemistry and abrasion-resistant topcoats; consider co-investment models with resin suppliers to secure priority allocations and price-fixed windows tied to a transparent feedstock index.

- Resin producers and chemical formulators: Prioritize R&D for sustainable formulations and recycled-content-compatible anti-fog systems. Quantify the premium markets (medical, safety, display) where performance pays and protect licensing/IP where feasible.

- Private equity and strategic investors: Target mid-market converters with proprietary coatings and validated long-term OEM contracts. Use the report’s M&A screen to prioritize assets that deliver immediate accretion under base-case growth and optionality under accelerated-adoption scenarios.

Methodology and what we intentionally leave for the full report

The analysis is built from a hybrid methodology combining bottom-up production and consumption builds, over 120 primary interviews across the value chain, detailed supplier financial and capacity diligence, and price-sensitivity stress tests. Forecasts are provided with transparent assumptions and downloadable models so clients can stress-test their own scenarios.

True to the “preview” purpose of this release, we have deliberately withheld granular regional and application-level split tables and specific contract-level pricing to preserve the commercial utility of the full dataset. Subscribers to the full report receive complete regional and application breakdowns, downloadable Excel models, supplier scorecards, contract templates, and performance-test protocols.

How to use this preview in your 2026 planning cycle

- Immediate (0–90 days): Commission supplier audits for your top two suppliers, implement indexed procurement clauses tied to feedstock stressors, and pilot PFAS-free coatings for at-risk product lines.

- Near-term (90–180 days): Finalize regional sourcing strategy (nearshore vs. global), sign capacity reservation agreements tied to phased payments, and adopt standardized warranty language for anti-fog performance.

- Medium-term (180–360 days): Execute capex/digital investments for in-house coating capability where ROI is compelling, complete one targeted acquisition or strategic partnership, and roll out product transition plans for regulated formulations.

PW Consulting’s Anti Fog Polycarbonate Film And Sheet Market report is designed as a strategic toolkit for leadership teams that must balance supply security, product performance differentiation, and regulatory compliance during a period of predictable growth and unpredictable disruption. To access the full dataset, supplier scorecards, and our downloadable scenario model library, please visit PW Consulting’s report page or contact our industry team for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Anti Fog Polycarbonate Film And Sheet Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com