Push Buttons & Signaling Devices Market Share: Competitive Dynamics in a Fragmented Landscape

Other |

2026-03-25 08:58:33

As pharmaceutical formulation strategies evolve and compounding demand accelerates, the suppository base market is attracting renewed strategic attention from manufacturers, distributors, and healthcare service providers. PW Consulting’s latest market research — anchored on a 2025 base year and a 2026–2032 forecast horizon — delivers an evidence-based, execution-focused roadmap for leaders making high-stakes decisions in 2026. Built from a five-year historical series (2020–2025) and a robust forecasting engine, the study shows a steady market trajectory (CAGR: 5.5%) and outlines the operational levers that will determine winners and laggards across the value chain.

Suppository Base Market

Macro clarity with micro implications: The market expanded meaningfully between 2020 and 2025 and, under the base-case forecast, continues to grow through 2032. That trajectory creates choice points for capital allocation — whether to prioritize capacity expansion, vertical integration of raw materials, or focused formulation innovation.

Suppository Base Market

Practical orientation: This report is structured not as an academic exercise but as a playbook. It translates market momentum into immediate, tactical actions and medium-term strategic programs tailored to manufacturers, excipient suppliers, compounding pharmacies, and investors.

Suppository Base Market

Competitive posture: Market concentration metrics reveal a moderately fragmented landscape: the top three players account for roughly one-third of market value, while the top five capture just over two-fifths. That configuration creates space for differentiated niche plays as well as consolidation-driven strategies.

Consistent growth, disciplined opportunities — The market’s 5.5% CAGR points to reliable demand growth rather than volatile spikes. Firms should favor staged, modular investments that preserve optionality rather than large, irreversible bets.

Regulatory and quality hygiene are non-negotiable — Leading hard-fat bases meet European Pharmacopoeia standards and are produced under EU GMP with documented cGMP inspection histories. Companies that cannot demonstrate robust quality and regulatory pedigree will face margin compression and limited access to institutional procurement channels.

Raw material traceability matters — Many hard-fat bases originate from saturated fatty acids derived from vegetable sources such as coconut and palm kernel oils. Securing traceable, ethically sourced raw materials is both a risk and a market differentiator in tender-sensitive segments.

Compounding pharmacy demand shapes product portfolios — The compounding channel favors flexible, easy-to-handle base portfolios (including PEG blends and vegetable-origin hard fats). Suppliers who align pack sizes, documentation, and technical support to compounding workflows unlock disproportionate share gains.

Market sizing and validated forecasting engine (2020–2032) with scenario options and sensitivity to raw-material price shocks.

Supply-chain heatmap and vendor scorecards that rank suppliers on quality, capacity, geographic proximity, and ESG traceability.

Regulatory and standards matrix covering EP, USP touchpoints, and GMP inspection risk vectors for major production geographies.

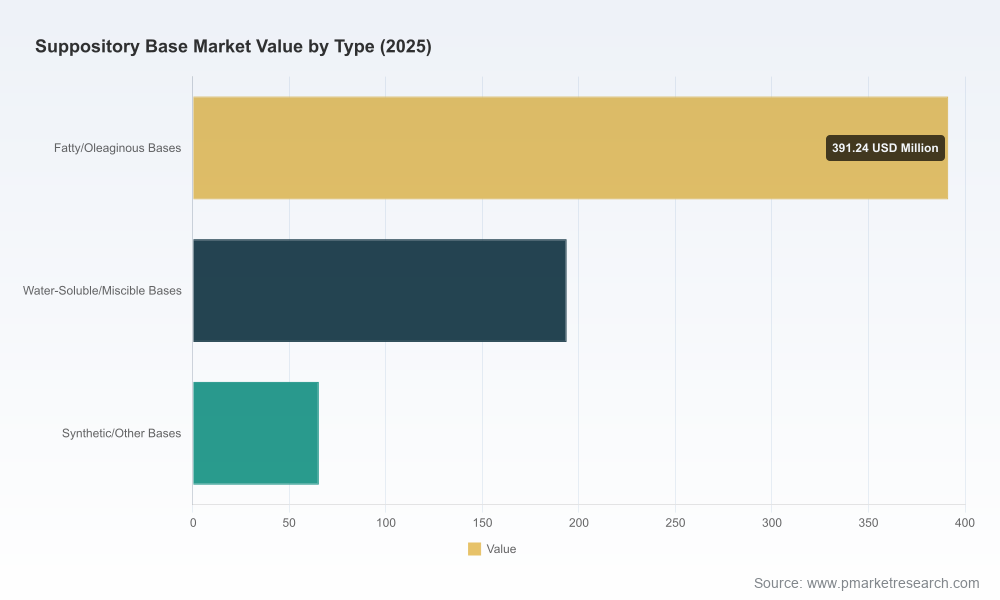

Product feature-and-benefit matrices comparing fatty/oleaginous bases, water-soluble/miscible systems, and synthetic options across handling, melting profile, API compatibility, and mucosal tolerance.

Pricing and commercial models, including price-elasticity benchmarks and channel margin expectations for compounding, institutional, and retail routes.

M&A and partnership playbooks: screening criteria, valuation benchmarks, and integration risk checklists tailored to both strategic and financial buyers.

Operational toolkits: batch-size optimization templates, quality-control checkpoints specific to suppository bases, and sample validation protocols for rapid market launches.

The market features a mix of specialty excipient suppliers, compounding-focused distributors, and multi-disciplinary chemical manufacturers. The following firms are highlighted for their strategic relevance and recent activity:

IOI Oleo GmbH (Hamburg, Germany) — A recognized producer of hard fat bases under the WITEPSOL® family. IOI’s product stewardship emphasizes GMP-certified production and alignment with pharmacopeial standards. Recent catalog refreshes underscore a consolidation of grade offerings and stronger messaging on quality and traceability, signaling a continued focus on institutional and regulated markets.

Medisca (Montreal, Canada; US operations) — A major supplier to compounding pharmacies, promoting both established and natural-branded base options. Their portfolio breadth and compounding-centric distribution network make them a default partner for pharmacies that require rapid availability and formulation support.

PCCA (Houston, Texas, USA) — Focused on compounding excellence, PCCA’s proprietary base formulations and deep engagement with pharmacy partners position it as a customer-intimate player capable of driving formulation standards at the point of care.

SpecializedRx (USA) — A niche supplier whose assortment includes widely used grades and proprietary blending approaches, SpecializedRx competes on responsiveness and tailored packaging for compounding environments.

Gattefossé (France) — Known for R&D-driven hard-fat base development, Gattefossé differentiates on drug dispersion, stability science, and mucosal tolerance — attributes that matter to pharmaceutical developers of fixed-dose and controlled-release rectal/vaginal products.

Croda Pharma (UK) — As a broader excipient house, Croda supplies bases and related excipients with a focus on integration into larger formulation platforms and cross-application synergies.

Recent market developments reinforce strategic themes: IOI Oleo’s product catalog update expanded clarity around registered hard-fat grades and quality claims, while Medisca’s active promotion of natural and established base grades reflects continued demand from compounding channels. Together, these moves highlight a bifurcated market: regulated, institution-facing quality assurance on one side; nimble, compounding-oriented distribution on the other.

Short-term (0–6 months): Stabilize supply and shore up quality documentation. Prioritize supplier audits for traceability and secure secondary sourcing contracts for core fatty feedstocks to mitigate spot-price exposure.

Near-term (6–18 months): Launch two-pronged commercial strategies — a regulated-market variant emphasizing certified, pharmacopeial-grade bases for institutional accounts, and a compounding-market package that includes technical support, smaller pack sizes, and rapid logistics. Use pilot accounts to validate margin improvements before scaling.

Medium-term (18–36 months): Evaluate M&A or JV options to acquire niche R&D capabilities (e.g., controlled-release dispersion technology) or to gain regional manufacturing footholds. Given the market’s moderate concentration profile, targeted consolidation can accelerate scale economies without triggering severe competitive backlash.

Cross-cutting: Implement an ESG and traceability communication program. Buyers and procurement committees increasingly require transparent sourcing of vegetable-derived feedstocks; proactive disclosures can become a competitive advantage rather than a compliance cost.

Raw material volatility: Price and availability shifts in coconut and palm kernel derivatives can compress margins; hedging and diversified suppliers reduce exposure.

Regulatory tightening: Higher scrutiny of GMP compliance or new pharmacopeial specifications could raise entry costs; maintain up-to-date certifications and invest in inspection-readiness.

Channel substitution: Growth in water-soluble/miscible systems for certain indications can cannibalize fatty-base demand; maintain product development capability to respond to formulation shifts.

Competitive pressure in compounding: Distributors and compounding networks can become gatekeepers; invest in direct pharmacy relationships and co-marketing to retain influence.

Boards and executive committees need analysis that connects numbers to choices. The full PW Consulting report supplies precisely that: transparent assumptions behind the 5.5% CAGR projection, scenario-based financials, and transaction-ready diligence materials. We map strategy to measurable KPIs — time-to-certification, payback periods for capacity builds, and ROIC thresholds for acquisition targets — so leadership can convert market visibility into accountable action.

This briefing highlights the strategic contours of the suppository base market and provides an operational lens for 2026. For companies preparing procurement, M&A, product development, or go-to-market strategies, the full PW Consulting Suppository Base Market report contains the segment-level intelligence, company benchmarks, and downloadable toolkits required to execute with confidence. Access the full report and supporting datasets through our client portal to unlock the granular insights and proprietary models withheld in this summary.

For detailed analysis of this topic, please visit the official page:Suppository Base Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com