Global Clinical Trial Supplies Market Growth Drivers and Forecast Report 2034

Health |

2026-05-06 13:21:57

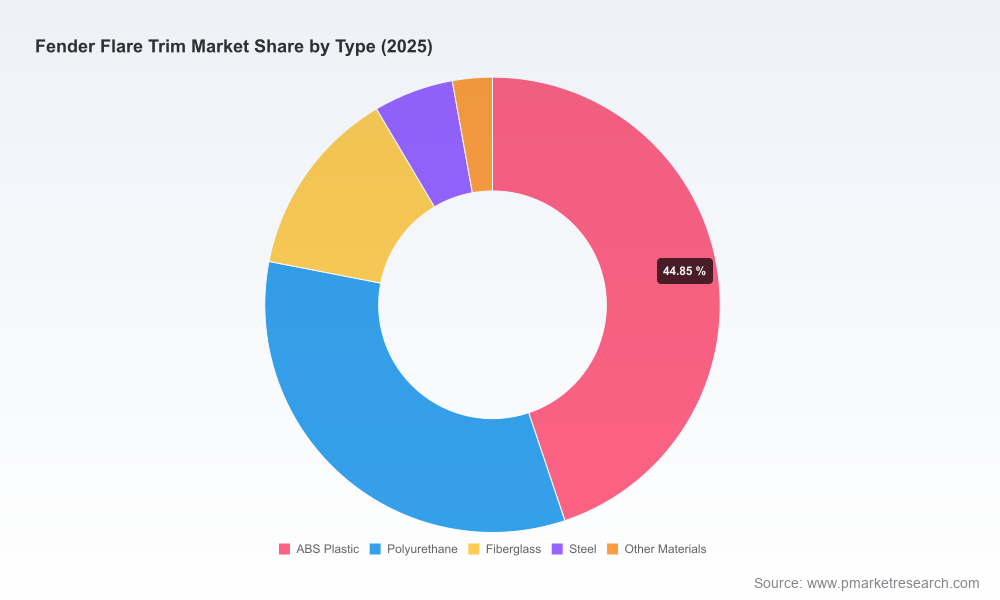

PW Consulting's latest market briefing on the Fender Flare Trim market positions industry leaders and new entrants for decisions that will shape 2026 strategy. Anchored on a 2025 base year analysis and a forward-looking 2026–2032 forecast horizon, the report models a steady mid-single-digit trajectory, with an aggregate market expansion underpinned by vehicle personalization trends, OEM accessory programs, and resilient material supply chains. The market is sized at approximately 1.39 billion USD in 2025 and is projected to move toward just over 2.0 billion USD by 2032, reflecting a compound annual growth rate of 5.45% across the forecast window. Market concentration is meaningful but not prohibitive: the three largest players account for a sizable portion of sales, with the top five controlling a majority—conditions that favor focused differentiation and selective consolidation.

Fender Flare Trim Market

Actionable, time-sensitive guidance: Automotive aftermarket and OEM suppliers face a window in 2026 to convert product portfolios and channel strategies into durable share gains. This preview highlights the strategic levers that generate value in that window without revealing proprietary segment-level figures.

Fender Flare Trim Market

Risk-managed growth planning: With raw-material dynamics and regulatory compliance increasingly influencing sourcing and product design, PW Consulting’s scenario-informed outlook enables procurement and R&D teams to prioritize investments with measured downside protection.

Fender Flare Trim Market

M&A and partnership intelligence: The structure of the market—moderately concentrated with several specialized players—creates targeted opportunities for bolt-on consolidation and capability-led partnerships. We identify priority capability gaps and the archetypal targets likely to accelerate scale or technical differentiation.

Demand drivers — personalization meets utility: Demand for fender flare trims is being driven by two parallel forces: vehicle owners’ growing appetite for customization and OEMs’ increasing inclusion of accessory packages for trucks and SUVs as profitability levers. These demand streams sustain both aftermarket volume and higher-margin OE accessory channels.

Material and supply dynamics: EPDM rubber remains a dominant substrate for edge seals and trims because of its ozone and weather resistance. Its production benefits from global manufacturing footprints and robust distribution networks, reducing short-term supply shocks but keeping input-cost exposure on the radar for 2026 procurement strategies. Separate industry forecasts show the broader synthetic rubber market trending strongly into 2032, reinforcing commodity-demand tailwinds for trim producers.

Regulatory and safety constraints: Automotive trim components are subject to established material and flammability standards. Compliance requirements—such as flammability testing commonly applied to rubber components—are non-negotiable factors in OEM sourcing decisions. Anticipatory compliance and validated test records will continue to be differentiators for suppliers pursuing OEM contracts.

Channel evolution and go-to-market: Peel-and-stick and pre-applied adhesive systems have materially reduced installation friction in both aftermarket and accessory channels. The prevalence of high-quality tapes and adhesive systems is accelerating modularization of trim products, enabling faster fitment and lower returns.

Robust market-sizing and trend analysis: A granular top-down and bottom-up reconciliation for 2020–2025 with a deterministic 2026–2032 forecast, including base-case, upside, and downside scenarios tuned to raw-material cost, vehicle production cycles, and aftermarket demand elasticity.

Go-to-market playbooks: Channel-specific strategies (OEM accessory programs, direct-to-consumer aftermarket, and distributor partnerships) with step-by-step recommendations for product specifications, pricing bands, and promotional levers to optimize margin capture.

Product and materials roadmap: Comparative lifecycle cost analysis across common substrates, tradeoff matrices for weight, durability and cost, and recommended product architectures for short-lead incremental innovation and longer-term material substitution initiatives.

Supply-chain stress-testing: Scenarios and mitigation playbooks that translate EPDM and other rubber market volatility into procurement actions—inventory buffers, multi-sourcing frameworks, and supplier scorecards calibrated for 2026 budget cycles.

Regulatory compliance workspace: A condensed compliance matrix aligning common trim constructions with applicable flammability and material standards and an implementation checklist for supplier qualification during OEM audits.

M&A and partnership blueprint: Target selection criteria, valuation heuristics and integration risk checklists crafted for strategic acquirers seeking manufacturing capacity, adhesive-system know-how, or channel reach.

The Fender Flare Trim market combines specialist suppliers, roll-forming shops, and accessory brands that straddle OEM and aftermarket channels. PW Consulting’s competitive analysis identifies tactical strengths and vulnerabilities for leading participants and suggests near-term moves to secure share in 2026.

Trim-Lok, Inc. (San Clemente, CA) — known for EPDM rubber trims and peel-and-stick adhesive systems. Recent product and catalog activity (expanded Catalog 800 and metric/multilingual editions plus new cut-to-length sealing kits) signals an aggressive product-platform and distribution play. Strategic implication: Trim-Lok’s broadened documentation and kit-based products lower adoption friction for OEM accessory channels—competitors should anticipate shorter procurement cycles and increased spec-reference visibility in OEMs and fleets.

Trimco (USA) — focuses on flexible plastic trims using high-performance acrylic foam tapes. Strength lies in conformability and ozone-resistant formulations. Strategic implication: Suppliers competing on form-and-fit should prioritize adhesive-system performance data and validated fitment guides to neutralize Trimco’s installation advantage.

Johnson Bros. Roll Forming Co. (Berkeley, IL) — custom roll-forming capability that plays well with low-volume, high-complexity programs. Strategic implication: Roll formers are acquisition targets for mid-sized suppliers seeking die-capability and short-run flexibility for accessory niches.

Bushwacker (USA) — a prominent accessory brand offering complete flares and replacement edge trim, with emphasis on minimal gapping and robust fitment. Strategic implication: Brands that own the aftermarket consumer channel have pricing power and margin flexibility; manufacturers should consider white-label partnerships or branded co-launches to access this channel.

Air Design (USA) — supplies OE-style and low-profile flares, often through OEM accessory programs. Strategic implication: Close alignment with OEM accessory qualification processes and early-stage design-in support are entry tickets for suppliers competing for factory accessories.

Steel Rubber (USA) — EPDM edge trim specialist with peel-and-stick solutions; positions on long-term durability and resistance. Strategic implication: Material-differentiation claims backed by independent test data will increasingly win fleet and OEM specs in 2026.

Putco (USA) — offers premium stainless-steel trims, representing a higher-margin aesthetic segment. Strategic implication: Luxury and premium accessory strategies provide elevated margins but require distinct distribution and brand-building investments.

Trim-Lok’s catalog refreshes and product kit launches across 2025 demonstrate a focused push to make specification and installation easier for OEM and aftermarket channels—an example of product-led commercialization that compresses the buyer’s adoption cycle.

Across the market, adhesive systems and fitment kits are replacing labor-intensive installation approaches, accelerating aftermarket growth and increasing the importance of tape and sealing technology partnerships.

Prioritize adhesive-system partnerships: For manufacturers and brands, securing qualified tape and adhesive suppliers reduces returns and warranty exposure. Consider co-developed fitment kits that bundle trim with validated adhesives to simplify distribution.

Invest in validated compliance documentation: Build an audited compliance package for common flammability and material standards to remove procurement friction for OEMs and larger fleet customers.

Adopt a two-track product roadmap: pursue incremental cost-and-fit improvements in the near term while piloting material innovations (lighter-weight composites, recycled-content formulations) to capture sustainability-led specs expected from fleet and OEM RFPs.

Use M&A tactically: Target roll-forming shops, small-volume molders, or adhesive-technology vendors to plug capability gaps quickly. Integration planning should prioritize quality systems and supply continuity.

Scenario-proof procurement: Implement multi-source contracts for EPDM and key tapes, and model margin sensitivity to 10–20% swings in key raw-material input costs—use this to set hedging or inventory thresholds going into 2026.

Channel segmentation and pricing: Differentiate pricing and packaging between premium accessory channels and mass-market aftermarket, preserving margin on branded premium SKUs while using value bundles to drive volume in the mass aftermarket.

This briefing presents the strategic contours and operational levers that will matter most in 2026. PW Consulting’s full Fender Flare Trim Market report extends these insights with the underlying datasets, supplier scorecards, and the granular segmentation necessary for transaction due diligence and product portfolio optimization. In keeping with our “preview” approach, we have intentionally withheld detailed region- and application-level breakdowns in this release to focus on imperatives; the full intelligence package contains the granular splits, market maps, and downloadable models that procurement, corporate development and product teams require to move from strategy to execution.

For executives and functional leaders seeking the underlying market models, supplier matrices, and our detailed scenario analyses that inform the 2026 playbook, request the full PW Consulting Fender Flare Trim Market report. The comprehensive package includes downloadable spreadsheets, supplier profiles, and the operational checklists referenced in this preview—tools designed to convert insight into measurable action in 2026.

For detailed analysis of this topic, please visit the official page:Fender Flare Trim Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com