Recovered Carbon Black (rCB) Market: Strategic Priorities for 2026 — PW Consulting Market Brief

Executive snapshot

The recovered carbon black (rCB) market has moved from an early-stage sustainability niche into a structurally expanding segment of the elastomers and specialty materials complex. Our updated market model shows global rCB market value rising from USD 425.1 Million in 2020 to USD 718.5 Million in 2025, and we forecast it to reach USD 1,539.4 Million by 2032 — an implied compound annual growth rate of approximately 11.5% across the 2026–2032 forecast window. This trajectory is driven by maturing pyrolysis technologies, OEM sustainability commitments, regulatory reclassification of pyrolysis products, and accelerating commercial-scale capacity additions worldwide.

Recovered Carbon Black Rcb Market

Why this brief matters for 2026 decision-making

- Prioritizes the tactical choices procurement and R&D teams must make in 2026 — from qualification timelines to multi-sourcing strategies.

- Identifies how certification, grade differentiation and feedstock economics will influence partner selection and contract structure.

- Maps the timing and scale of capex and M&A opportunities for players seeking to secure differentiated supply or to vertically integrate.

- Translates macro growth and regulatory drivers into actionable risk mitigations for supply continuity and product performance.

Market dynamics shaping strategy in 2026

Three categories of forces will determine winners and laggards next year: feedstock economics, regulatory clarity, and technical fit with end-use performance.

Recovered Carbon Black Rcb Market

- Feedstock and cost volatility: Rising recovery demand has increased the market value of scrap tires in some hubs. Procurement professionals should expect tighter feedstock-to-product margins in 2026 and plan contractual protections and price-indexing mechanisms accordingly.

- Regulatory tailwinds and compliance gates: Policy changes such as the EU Waste Framework Directive that treats tire pyrolysis as a recovery route, and the growing adoption of ISCC PLUS for chain-of-custody verification, materially improve commercial acceptance of rCB. These create near-term uplift for suppliers who already hold recognized certifications and add a certification timing risk for those that do not.

- Technical limits and application fit: rCB typically achieves lower purity compared to most virgin carbon blacks, which constrains direct substitution in the highest-performance tire tread compounds. That said, product-grade improvements and mass-balance certification enable substitution in many reinforcement and non-tire applications, creating differentiated route-to-market strategies for suppliers and converters.

Segmentation and where to focus

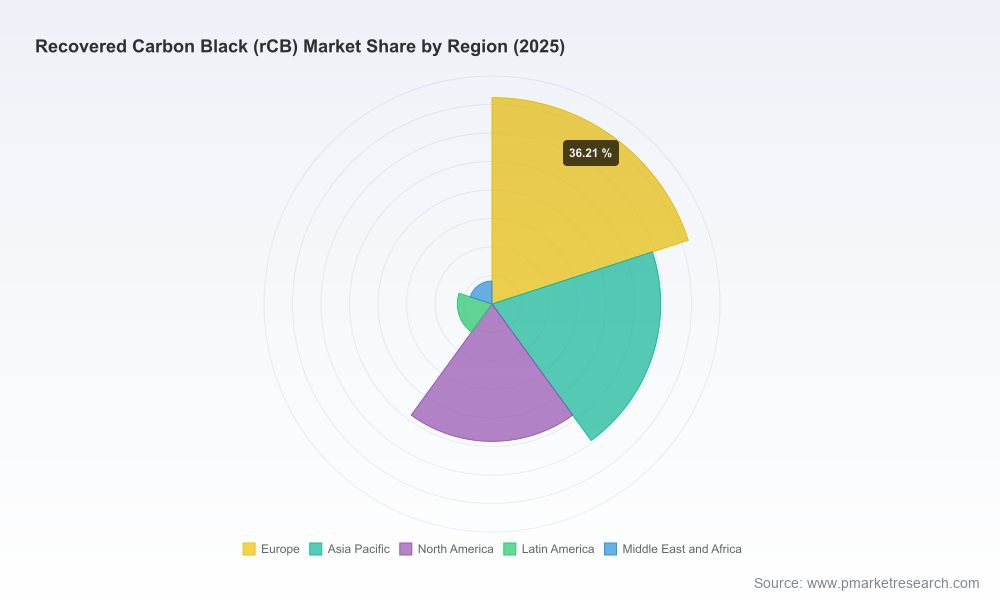

Our report dissects the market across three practical dimensions — geography, application, and product grade — and links each segment to technical requirements, logical supply chains and adoption barriers. While we do not disclose segment-level revenue here, executives should note the following implications:

Recovered Carbon Black Rcb Market

- Application segmentation (e.g., tire vs. non-tire rubber goods, plastics/masterbatches, coatings/inks) determines acceptable purity thresholds and required product certifications.

- Regional dynamics influence logistics cost, feedstock supply, and regulatory acceptance — which in turn shape sourcing and localisation strategies.

- Grade differentiation (standard vs. premium) is the single most important determinant of pricing power and OEM acceptance; premium certified grades earn strategic customer conversations, while standard grades address volume-driven industrial demand.

Competitive landscape — what incumbents and scale-ups are doing

The market is becoming moderately consolidated: the top three suppliers account for a meaningful minority share and the top five control nearly half the market. This structure creates room for both scale-driven incumbents and specialized niche players.

- Pyrolyx AG (Germany): A technology-first commercial producer, Pyrolyx has advanced credibility with proprietary pyrolysis know-how and product grades engineered to be near-equivalent to common virgin blacks used in tire reinforcement. Notably, Pyrolyx opened its first commercial-scale plant in Germany in September 2023, signalling a move from pilot to industrial throughput that matters for multi-year supply contracts and qualification pipelines.

- Black Bear Carbon B.V. (Netherlands / Michelin-backed): Backing by a major OEM brings strategic customer access and capital for capacity scale-up. Black Bear’s production of high-purity grades, coupled with Michelin’s involvement, demonstrates how OEM-linked partnerships can accelerate qualification and mainstreaming of rCB into tire manufacturing.

- Enviro AB (Sweden): An early mover on certification, Enviro secured ISCC PLUS credentials, reducing counterparty sustainability risk for buyers. Their certification pathway exemplifies a commercially significant premium: buyers increasingly require proof points for closed-loop claims.

- Hi-Green Carbon Limited (India): Emergent volumes from Asia position Hi-Green to serve fast-growing regional demand, but policy and tariff structures (for example, import GST regimes) affect cross-border trade economics and should be integrated into sourcing evaluations.

Recent industry developments that matter

- September 2023: Pyrolyx opened its first commercial-scale rCB plant in Germany — a clear signal that industrial-scale pyrolysis production is maturing.

- June 2023: Michelin announced industrial rCB production ramp at an expanded European facility via Black Bear Carbon — showcasing OEM-led vertical strategies.

- March 2023: Enviro AB achieved ISCC PLUS certification for tire-to-rCB production — highlighting certification as a commercial differentiator.

Practical playbook for executives in 2026

Use the following prioritized actions as a practical checklist when applying the full PW Consulting report to your 2026 planning cycle:

- Fast-track material qualification pilots: Begin controlled qualification with multiple certified suppliers for all compounds where performance tolerance allows. Time-to-qualification, not price, will often be the gating constraint in 2026.

- Lock in diversified feedstock-linked contracts: Structure supply agreements with formulaic indexes to scrap-tire markets and include step-in rights or secondary sourcing clauses to manage feedstock-driven supply risk.

- Mandate certification as a procurement filter: Prioritize suppliers with recognized mass-balance or chain-of-custody certifications to reduce future compliance disruption and to underpin sustainability claims to end customers.

- Evaluate partnership models with OEMs: Consider minority equity, offtake guarantees, or co-investments with rCB producers to secure preferential access to premium grades and to accelerate product co-development.

- Define technical acceptance windows by application: For non-critical elastomer and plastic compounding, accelerate adoption; for critical tread applications, plan staged substitution supported by co-development and field testing.

- Run scenario-based capex screens: Use the report’s investment cases to identify breakpoints where building or buying rCB capacity becomes economically attractive under differing feedstock and product-price assumptions.

What the PW Consulting report contains (practical tools)

Our full Recovered Carbon Black (rCB) Market report is designed as an operational playbook for 2026. It includes:

- A forward-looking market model (2026–2032) with demand curves, sensitivity scenarios and supplier availability overlays.

- Commercial intelligence dossiers and techno-economic profiles for major rCB producers and a watchlist of near-term entrants.

- Regulatory and certification roadmaps, including jurisdictional comparators, timelines and certification cost estimates.

- Supplier scorecards that combine grade specs, certification status, demonstrated supply volumes, and logistical considerations.

- Actionable procurement templates (RFx language, qualification checklists, contract clauses for feedstock volatility).

- Investment cases and M&A frameworks with stress-tested returns under alternate feedstock and pricing regimes.

To preserve commercial integrity and to align with our “preview” approach, the report showcases granular segment-level outputs and company-specific revenue tables that are available only in the full report package.

How to use the intelligence in 2026

- CEOs and strategy teams: Use the scenario outputs to prioritise strategic bets — whether to partner with certified scale-ups, sponsor internal pyrolysis pilots, or acquire upstream feedstock capabilities.

- Procurement leaders: Apply the supplier scorecards and contractual playbook to reduce qualification lead time and to de-risk supply continuity.

- R&D and product development: Leverage grade performance matrices to select target applications for substitution pilots and to define co-development KPIs with rCB suppliers.

- Investors and corporate development: Use the valuation frameworks and capex screens to size opportunities and to gauge timing for entry via minority stakes or greenfield expansion.

Common questions (FAQ) — short answers

- Can rCB replace virgin carbon black across the board? Not yet — purity and performance limits mean high-performance tread compounds still rely on virgin blacks. However, the gap is closing for many reinforcement and non-tire applications.

- Is certification mandatory? Not universally, but ISCC PLUS and equivalent standards materially accelerate commercial acceptance and reduce reputational and compliance risk.

- Are supply risks material? Yes — feedstock availability, regional logistics and nascent production scale can cause short-term constraints. Diversified sourcing and contractual protections are essential.

Closing — what to do next

The rCB market is transitioning from experimental adoption to practical industrialisation. For executives planning 2026 budgets, the central choices are: when to commit to scale, whom to certify with, and how aggressively to integrate upstream. PW Consulting’s full Recovered Carbon Black (rCB) Market report converts these strategic questions into quantified options and executable next steps. Visit the PW Consulting reports page to access the full report, the underlying data model, and a customizable decision toolkit tailored for procurement, R&D and corporate development teams.

For detailed analysis of this topic, please visit the official page:Recovered Carbon Black Rcb Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com