Neem Oil and Concentrates market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-05-12 10:39:07

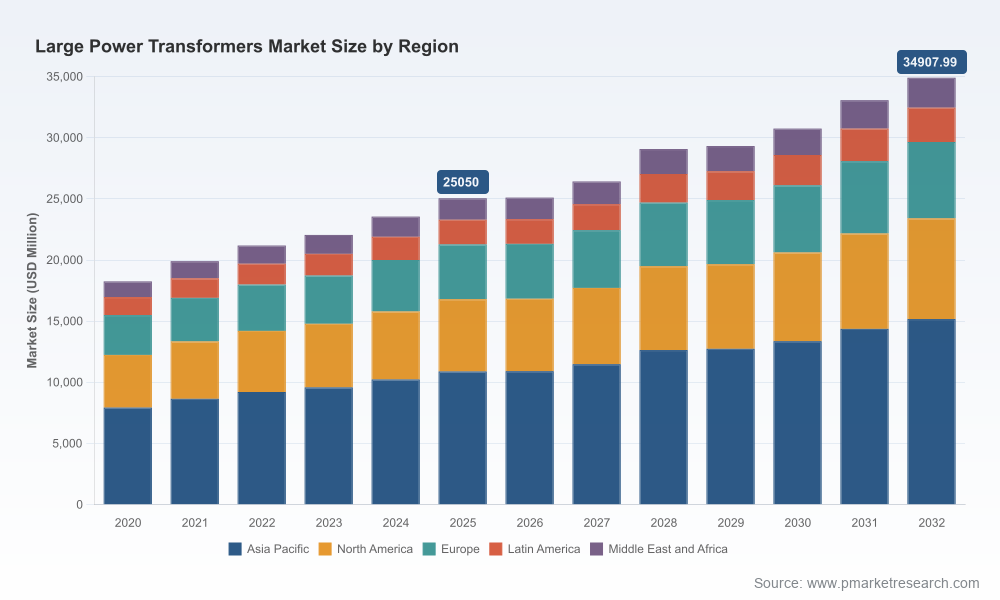

PW Consulting’s latest Large Power Transformers (LPT) market study — covering historical performance (2020–2025) and forward-looking scenarios for 2026–2032 — is designed as an operational playbook for executives making capital, procurement, and industrial policy decisions in 2026. At the macro level, the global LPT market reached approximately USD 25,050 Million in 2025 and is modeled to expand at a 4.85% CAGR across the 2026–2032 forecast window, approaching roughly USD 34,908 Million by 2032. Those topline dynamics are only part of the story: supply-side concentration, raw-material constraints, dramatically extended lead times and active capacity investments are reshaping how buyers and suppliers should act this year.

Large Power Transformers Market

Demand composition is shifting. Accelerating renewables, grid modernization, and hyperscale data-centre buildouts have pushed procurement peaks into a new cadence. This is not a cyclical blip — it is a structural reconfiguration of load and transmission profiles that requires different product specifications, testing regimes and lifecycle services.

Large Power Transformers Market

Supply remains constrained. Critical inputs and capacity bottlenecks are visible: domestic production of grain-oriented electrical steel (GOES) in the U.S. covers only an estimated 12–20% of demand, with a single major domestic producer currently active. At the same time, transformer unit prices have increased sharply since 2019 — our review of market intelligence shows roughly a 77% increase for power transformers and a 45% rise for generator step-up units — driven by steels, copper and broader supply-chain pressure.

Large Power Transformers Market

Lead times have lengthened to operationally significant levels. Industry surveys and logistics studies report average LPT lead times near 128 weeks, with many orders stretching beyond 210 weeks amid surging clean-energy and data-centre requirements. For procurement planners, what used to be a two- to four-quarter sourcing cycle is now a multi-year scheduling problem.

Market structure is moderately concentrated. Our concentration analysis indicates top-tier suppliers collectively command a meaningful share of global LPT supply — a dynamic that increases supplier leverage on pricing, delivery and technical customization.

Actionable market sizing and scenario models calibrated to 2025 base-year realities and multiple 2026–2032 demand paths. These models are built for sensitivity testing (lead-time shocks, raw-material price trajectories, accelerated domestic content rules).

Procurement playbook for utilities, IPPs and industrial buyers: decision trees for make-vs-buy, recommended contracting structures (including indexation, capacity reservation and modular delivery), and trigger points for strategic inventory investments.

Supplier risk matrix and qualification templates that operational teams can deploy immediately to stress-test existing vendor lists against technical capability, delivery reliability and raw-material exposure.

CapEx and localization playbooks for OEMs and new entrants: site-selection criteria, lead-time reduction levers, and a staged ramp plan that balances demand capture with capital discipline.

Aftermarket and lifecycle monetization roadmap: strategies to convert extended-service windows, retrofits and life-extension offerings into annuity revenues as an offset to order-book volatility.

Primary research-based company dossiers, competitive benchmarking and scenario-specific supplier profiles to support negotiation teams and M&A diligence.

Note: This press summary intentionally omits granular regional, type and application splits that appear in the full report. Those segmented data and unit-level forecasts are preserved to support commercial insights accessible from our full report package.

Hitachi Energy (Zurich, Switzerland) — A global technology leader offering LPTs up to 1,100 kV and 1,300 MVA with strong capabilities in HVDC and grid integration. Recent announcements include a multi-hundred-million USD investment to establish a major U.S. LPT facility (South Boston, Virginia) and capacity expansion in Quebec. These moves materially increase North American onshore capacity by the late 2020s and signal an aggressive play for long-lead projects requiring domestic content.

Siemens Energy (Munich, Germany) — Global engineering scale with LPT offerings to utility standards and plans for a first U.S. LPT plant in Charlotte, NC; recruitment and commissioning are being accelerated toward a 2027 production target. Siemens’ approach combines local production with established aftermarket networks — a model that shortens supply chains for U.S. buyers while preserving proprietary engineering advantages.

GE Vernova (Cambridge, MA, USA) — Leveraging its Prolec GE JV and U.S. footprint, GE targets utility-scale modernization and grid projects. Their strategic advantage is program-scale experience and integrated project delivery for large grid interconnections.

Hyundai Electric (Seoul, South Korea) — Supplier with EHV offerings and U.S. manufacturing presence; candidates for customers prioritizing both performance and competitive pricing from Asian-built platforms with localized assembly.

Virginia Transformer Corporation (Roanoke, VA, USA) — The largest U.S.–owned custom LPT manufacturer with deep utility and industrial relationships; a go-to for projects where U.S. origin and customization are procurement priorities.

WEG (Jaraguá do Sul, Brazil) — Expanding U.S. capacity with a reliability-focused, vertically integrated model aimed at generation and transmission segments.

Delta Star (Lynchburg, VA, USA) — Specialist in mobile substations and large units for North America; appealing for contingency and rapid-deployment programs.

Pennsylvania Transformer Technology (Canonsburg, PA, USA) — High-voltage focus and service-based business model; useful for owners prioritizing field service and fast turnarounds.

SPX Transformer Solutions (Waukesha, WI, USA) — Mix of medium and large units with life-extension services; an option for asset-heavy owners seeking long-term O&M performance improvements.

Eaton (Dublin, Ireland) — Broad industrial scale and recent investments into U.S. facilities targeting large three-phase units; integrates control and protection systems into broader solutions packages.

Strategic implication: OEM greenfield investments and expansions announced in 2025–2026 materially improve onshore capacity over the next 24–36 months, but they do not eliminate systemic supply-chain constraints in the near term. Buyers should recalibrate expectations for delivery certainty and pricing leverage accordingly.

Embed multi-year planning into capital programs. Treat LPT procurement as a multi-year supply commitment rather than single-project sourcing: align project pipelines into consolidated program contracts where possible.

Prioritize dual-track sourcing. Maintain a blend of domestic and trusted international suppliers, with formal contingency triggers for capacity substitution and pre-approved technical equivalencies.

Negotiate capacity reservation clauses. For critical projects, secure forward-capacity rights with contractual milestones and exit options rather than relying on spot procurement when lead times are at historic highs.

De-risk raw-material exposure. Include price-pass-through frameworks and strategic metal hedging where appropriate, and evaluate partnerships or joint investments in GOES and copper-processing supply to address upstream shortages.

Accelerate standardization and modularity. Reduce customization-driven lead-time penalties by converging on fewer engineering variants, and exploit modular tank and bushing designs to shorten delivery and testing cycles.

Monetize aftermarket. Invest in predictive-maintenance programs and long-term service agreements to convert extended life-cycle support into recurring revenue and higher asset reliability.

Use scenario stress tests in capital approvals. Every high-value LPT procurement should be stress-tested for: supplier failure, raw-material spike, legislative domestic-content requirements, and accelerated decarbonization timelines.

Upstream material shocks: GOES and copper availability/pricing remain the earliest indicators of cost and delivery pressure.

Factory ramp milestones: physical commissioning dates, labor hiring rates and vendor qualification progress at announced greenfield plants are real-time signals for when onshore capacity will materially loosen.

Lead-time tails: watch order-book aging metrics and unfilled backlog across Tier-1 suppliers; a growing share of >210-week orders is a clear signal to move to contingency plans.

Policy shifts: new domestic-content incentives, tariffs or procurement mandates can rapidly re-shape supply chains; scenario run rates in our models show material P&L sensitivity to such policy changes.

For decision-makers planning capital allocations and procurement strategies in 2026, the PW Consulting LPT report functions as both a diagnostic and a playbook. It reconciles the macro growth path (a mid-single-digit CAGR across 2026–2032) with the granular operational levers that determine whether a program will be delivered on time and on budget. Our competitive intelligence highlights where capacity is expanding and where single-source dependencies remain. Our procurement and capex modules provide the contractual, technical and commercial templates to convert insight into defensible action.

This press summary is intentionally strategic rather than encyclopedic: detailed regional, type and application splits, unit counts, and project-level vendor allocations are available only in the full report and models. For commercial teams requiring contract-ready language, risk matrices mapped to supplier profiles, or scenario-model access for board-level review, please consult the full PW Consulting Large Power Transformers Market report and modelling toolkit.

For detailed analysis of this topic, please visit the official page:Large Power Transformers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com