Corn Flour Market 2026: Strategic Imperatives from PW Consulting’s Market Outlook

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I present a forward-looking synthesis from our Corn Flour Market report (base year 2025, historical review 2020–2025, forecast 2026–2032). This briefing is written for executive teams planning investments, procurement strategies, product roadmaps, and M&A activity in 2026. It demonstrates the analytical depth of our work while intentionally withholding detailed segment tables and granular splits—to guide you to our full report for the underlying data and model outputs.

Corn Flour Market

Executive snapshot

The global corn flour market registered USD 6.45 Billion in 2025 and is projected to continue a steady expansion through the forecast horizon, reaching approximately USD 8.63 Billion by 2032. Our model points to a compound annual growth rate (CAGR) of about 4.25% for 2026–2032. These headline dynamics reflect a combination of stable demand from established food applications, incremental gains in convenience and snack formats, and premiumization tied to clean-label and functional ingredient trends.

Corn Flour Market

Why 2026 is a decision inflection point

- Macro momentum: Growth is predictable but not runaway—companies can capture value through operational choices (optimizing milling efficiencies, fortification, and SKU rationalization) rather than relying solely on demand expansion.

- Input-price sensitivity: Corn price volatility and futures levels will continue to reshape margins and procurement strategy; firms that refine hedging and sourcing diversification will gain a structural cost advantage.

- Policy and trade shocks: Recent legal and tariff developments have altered trade flows, creating near-term opportunities for importers and exporters that can adapt distribution footprints quickly.

Market trajectory and macro drivers

Our historical analysis (2020–2025) shows a resilient base of demand anchored in bakery and traditional applications, with newer growth pockets in ready-to-eat snack and clean-label mixes. The market baseline in 2025 at USD 6.45 Billion provides the starting point for scenario work. From that base, our central forecast—built from proprietary demand models, price elasticity estimates, and supply-side capacity mapping—anticipates a 4.25% CAGR through 2032. Under alternative scenarios (higher commodity inflation or accelerated premiumization), growth can diverge meaningfully from the base case; our full report contains stress-tested scenario outputs and sensitivities.

Corn Flour Market

Key dynamics shaping supply and demand in 2026

- Raw materials and pricing: USDA projections for the 2025/26 U.S. season-average corn price and observed futures activity (notably the April 2026 futures range) underscore continued price sensitivity across the value chain. Procurement teams must align hedging horizons with product shelf-life and downstream pass-through capabilities.

- Standards and formulation constraints: Regulatory standards such as U.S. FDA Code of Federal Regulations Title 21 continue to govern product identity and labelling for white and yellow corn flour, shaping product development and export compliance obligations.

- Trade policy shifts: Judicial and regulatory developments in 2025–2026—most prominently a U.S. Supreme Court ruling that altered certain import tariff structures—have changed the calculus for cross-border sourcing. The tariff environment that prevailed in 2025 created friction in supply chains; its partial rollback in 2026 opens windows to reconfigure international procurement strategies.

- Sustainability and traceability: Buyers and retailers increasingly demand transparent origin and regenerative practices. Producers that can credibly claim renewable-energy milling, lower lifecycle emissions, or regenerative-sourced corn access premium channels and longer-term contracts.

Competitive landscape — what to watch

The market displays moderate concentration: the top three firms account for approximately 28.5% of market supply, while the top five capture about 38.2%, indicating meaningful competition but also room for regional and product-focused specialists. Below are the strategic postures we see among leading participants:

- Archer Daniels Midland Company (ADM) — a vertically integrated processor with scale across wet and dry milling. Recent sustainability investments (including regenerative sourcing and renewable-energy milling initiatives announced in 2025) signal a dual play: cost resilience through energy transition and a premium product roadmap for sustainability-conscious buyers.

- Cargill, Incorporated — emphasizes supply chain integration and local capacity expansion. The company’s announcement of a new corn ethanol facility in Brazil (2025) reflects a diversification strategy that influences co-product flows and working-capital profiles; such investments can have downstream implications for ingredient availability and feedstock balancing.

- Bunge Limited — leverages broad origination networks across the Americas, which supports quick reaction to regional harvest and logistics shifts. Bunge’s playbook is centered on cross-border arbitration and logistics optimization.

- Ingredion and specialty ingredient players — compete on formulation support, texturizing solutions, and customized blends that help food manufacturers reduce development time and achieve label claims.

- Regional specialists and heritage brands (Gruma, Azteca Milling, Bob’s Red Mill, Grain Millers, etc.) — sustain strength in niche product formats (nixtamalized masa, organic, non-GMO, gluten-free). Their brand equity in traditional and retail channels is a durable advantage vs. commodity suppliers.

- Smaller millers and focused B2B processors — continue to capture opportunities in regional foodservice and industrial contract manufacturing where quick lead times and product customization matter more than scale.

Collectively, these players are reshaping competitive boundaries through sustainability claims, capacity reallocation, and ingredient innovation. Our report’s company dossiers include strategic KPIs, capacity maps, and recent M&A/activity trackers not reproduced here.

Strategic playbook for 2026 — five pragmatic moves

- Revisit procurement architecture: Move from spot-dominated buying to a blended approach—longer-term origin contracts for baseline volumes, complemented by futures and options for flexibility. Align hedging strategies to SKU margins rather than aggregate volume to avoid mis-pricing risk across product families.

- Prioritize differentiated product development: Invest in formulations that capture clean-label, gluten-free, or fortified positioning. Smaller format and convenience applications present higher margin uplift—allocate R&D resources to rapid-prototype lines and co-development with priority retail customers.

- Operational resilience: Evaluate dry- vs wet-milling footprints and energy pathways. For companies with capital flexibility, targeted investments in renewable electricity and process efficiency can reduce unit cost volatility and support sustainability claims that retailers increasingly reward.

- M&A and partnerships play: Given market concentration metrics and regional fragmentation, bolt-on acquisitions can rapidly secure channel access or niche technology (nixtamalization, organic certification, specialty milling). Joint ventures to manage origin risk and local compliance are also high-value options.

- Regulatory and trade scenario planning: Prepare rapid-response playbooks for tariff reinstatements or new standards; maintain a compliance matrix aligned to major export markets. Use scenario models (provided in our full report) to quantify P&L impacts under alternate trade and price outcomes.

What our full report delivers — practical, implementable content

PW Consulting’s Corn Flour Market report is designed as an operational tool for 2026 decision-making. Highlights (summarized; detailed data withheld in this preview) include:

- Proprietary demand models spanning 2020–2032 with base case and four alternate scenarios (upside/downside commodity and trade shocks).

- Full time-series market sizing (annual) and price-elasticity matrices used in our revenue forecasts.

- Supplier and capacity maps by milling technology and origin, plus a short-list of target assets suitable for acquisition by strategic and private-equity buyers.

- Commercial playbooks: SKU rationalization frameworks, margin ladders by product positioning, and go-to-market templates for launching premium corn-flour formulations.

- Risk matrices: tactical guidance for hedging, quality assurance, and regulatory compliance across major export jurisdictions.

- Company dossiers and benchmarking: strategy scorecards, recent initiatives, and near-term investment signals for the major players listed in this summary.

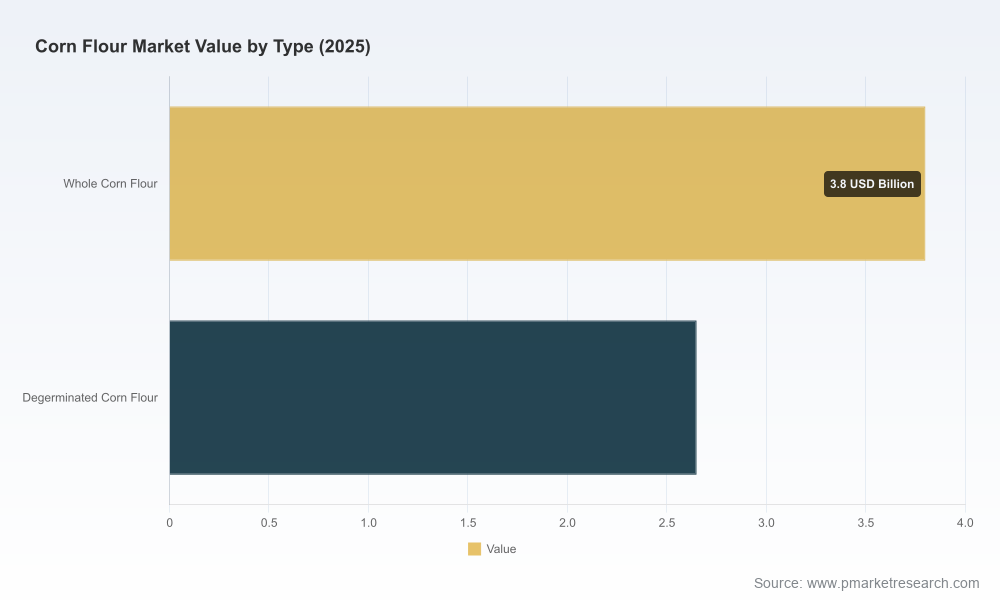

Note: This press briefing intentionally omits our detailed regional, type, and application splits and their underlying tables. These segment-level datapoints, scenario spreadsheets, and primary-source interview transcripts are available in the full PW Consulting report and accompanying data pack.

Implications for executive agendas in 2026

Decision-makers should treat 2026 as a year to convert strategic intent into durable advantage. The market’s steady growth provides room for margin improvement through operational excellence and product premiumization rather than relying solely on volume expansion. Key near-term priorities include: aligning procurement to more sophisticated hedging regimes, accelerating high-value product launches that meet sustainability and clean-label demand, and selectively pursuing capacity or capability M&A to secure regional advantages.

Closing — where PW Consulting adds value

Our firm combines market-level forecasting, granular supplier intelligence, and actionable commercial playbooks tailored for the corn-flour value chain. For teams preparing 2026 budgets, capital plans, or M&A pipelines, the full report converts headline growth and concentration metrics into a prioritized set of moves with quantified financial outcomes.

To access the complete dataset, scenario outputs, and proprietary playbooks, please consult the PW Consulting Corn Flour Market report and data pack. The full study contains the detailed segment tables and models that will enable precise budgeting and operational planning for the year ahead.

For detailed analysis of this topic, please visit the official page:Corn Flour Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com