Global Sugar Lactone Market Set to Hit USD 39.5 Million by 2032 at 5.0% CAGR

Other |

2026-06-09 13:21:30

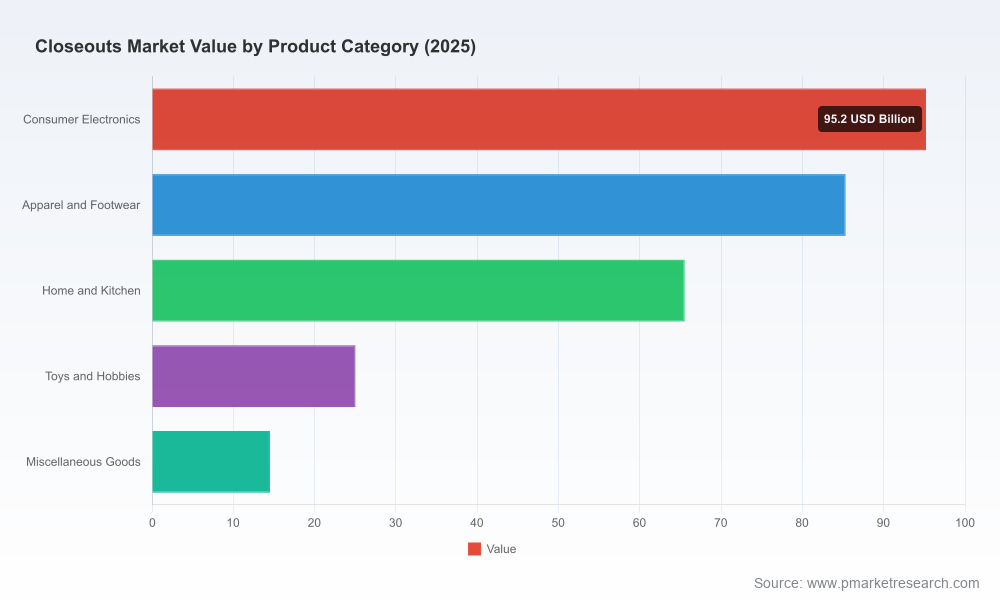

PW Consulting’s latest Closeouts Market research—anchored on a 2025 base year with historical analysis from 2020–2025 and forward-looking projections through 2032—translates deep, data-driven market intelligence into an operational playbook for executives preparing strategy in 2026. Our modeling shows the global closeouts market growing at a mid-single-digit compound annual growth rate (CAGR) of 6.85% over the forecast period, with overall size expanding from the mid‑hundreds of USD billions today to a materially larger market by 2032. This briefing highlights the strategic choices that matter next year while leaving detailed segment-level values and proprietary models for the full report and interactive portal.

Closeouts Market

Momentum and scale: The market experienced steady expansion through 2020–2025 and, based on our scenario-weighted forecasts, continues to grow sustainably into the next decade. That growth is fuelled by a combination of structural and cyclical forces—rising overstock generation, evolving secondary channels, and continued investor and operator interest in asset monetization.

Closeouts Market

Fragmented competitive structure: Market concentration remains low relative to many traditional retail industries—top-three and top-five operators account for under one quarter of the market—creating opportunities for differentiated operators, regional specialists, and digital-native entrants to capture value.

Closeouts Market

Supply-side dislocations: Retail insolvencies, cautious consumer spending patterns, and inventory management shifts have increased the flow of closeout and surplus merchandise into secondary markets. These supply dynamics have expanded available inventory while compressing time-to-liquidation for many product categories.

Policy and trade noise: Trade policy and tariff regimes—particularly U.S. tariffs on imported consumer goods—continue to affect pricing dynamics and cross‑border flows. Our review of macro studies and central-bank analyses indicates notable passthrough of tariff costs to downstream prices in several categories, creating both margin pressure and arbitrage opportunities for specialist liquidators and secondary retailers.

This report is designed as more than a market-size briefing; it is a hands‑on toolkit for commercial, operational, and M&A decision‑makers. Key deliverables include:

Proprietary forecasting models (2026–2032) with scenario and sensitivity toggles—allowing executives to stress-test outcomes under different consumer-demand, tariff, and bankruptcy rate assumptions.

Decision frameworks for monetizing surplus inventory across distribution channels (including auction platforms, pallet sales, and direct secondary retail)—with playbooks on channel mix optimization and margin improvement tactics.

A practical commercial playbook: pricing heuristics, condition grading standards, consignment vs. buy-sell contract templates, and SLA language tailored for retailers, manufacturers, and liquidation partners.

Operational diagnostics: logistics and reverse‑supply‑chain design patterns, returns triage workflows, grading and refurbishment economics, and warehouse capacity utilization strategies for high-turnover closeout assortments.

Analytics and technology adoption roadmap: data models for lot-level pricing, buyer-scoring algorithms, and recommended tech stack components for marketplaces, including real-time bidding engines and image-based condition assessment pilots.

M&A and partnership playbooks: valuation templates, integration checklists, and synergy capture estimates tailored to acquisitions of online platforms, pallet suppliers, and last-mile secondary retailers.

Regulatory risk mapping and mitigation measures covering tariffs, waste and disposal regulations, and evolving ESG expectations for downstream channels.

The market is populated by a broad spectrum of players—pure-play online marketplaces, auction houses, pallet suppliers, direct B2B wholesalers, and vertically integrated liquidators. Our competitive analysis balances company-level profiling with strategic evaluation of business models and vulnerabilities.

Direct Liquidation (directliquidation.com): A high-profile partner to national retailers, Direct Liquidation leverages auction mechanisms and wholesale channels to convert large retailer returns and overstock into rapid liquidity. Strengths: scale relationships with national brands and auction expertise. Watch for continued expansion of data-driven lot segmentation and greater emphasis on buyer experience to raise recovery rates.

B‑Stock (bstock.com): As an online marketplace connecting large retailers to wholesale buyers, B‑Stock’s digital marketplace model offers transparency and wide buyer reach. Their platform approach makes them a logical partner for omnichannel retailers seeking to retain pricing control while offloading excess inventory.

Liquidation.com (liquidation.com): A traditional auction-centric platform with an emphasis on surplus from major retail chains. Their continued relevance underscores the role of auction dynamics in price discovery for heterogeneous lots.

Overstock Trader (overstocktrader.com) and BULQ (bulq.com): These firms illustrate two different operational archetypes—facilitating downstream retail channels through curated lots and standardized pallet offerings respectively. BULQ’s approach reflects the productization of liquidation inventory, while Overstock Trader highlights networked relationships with discount channels.

UpLiquidation (upliquidation.com), Kole Imports (koleimports.com), Global Distributors (globalcloseouts.net), Countryside Closeouts, Total Surplus Solutions: These operators demonstrate the breadth of players active in direct wholesale and redistributed channels, with business models that vary by assortment curation, grading rigor, and value-added services such as refurbishment or repackaging.

Together, these firms reflect a market where digital marketplaces and traditional auction houses co-exist with specialized wholesale suppliers. Strategic differentiation today hinges on data quality, grading standards, logistics integration, and buyer network depth.

Optimize channel mix to protect margin: With increased inventory flows, organizations must balance speed-to-cash with revenue recovery. Our frameworks show when to route lots to auction, pallet sale, direct secondary retail, or targeted outlet channels to maximize realized value.

Invest in grading and disclosure: Standardized, verifiable condition grading directly raises buyer confidence and price realizations. Investing in automated vision systems and standardized disclosures is a high‑ROI operational improvement.

Build tariff-aware sourcing and pricing engines: Given the ongoing tariff uncertainty and significant passthrough effects on consumer pricing, firms should include tariff scenarios in pricing algorithms and contract language to protect margins and preserve buyer relationships.

Leverage marketplace liquidity while protecting brand equity: For brand owners, controlled channels that preserve price architecture and prevent gray-market spillover are critical. Structuring partnerships with platform providers to include geographic and channel fences can be a pragmatic compromise.

Pursue bolt-on M&A and partnerships: Low consolidation leaves room for roll-up strategies—especially acquiring regional pallet suppliers, last-mile refurbishers, or data-rich marketplaces. Our M&A playbook quantifies revenue synergies and integration risks for common transaction archetypes.

Adopt sustainability and compliance by design: Regulatory and reputational risks around disposal and waste are rising. Programs that prioritize reuse, repair, and transparent end-of-life pathways reduce regulatory exposure and resonate with partners and institutional buyers.

Our report includes scenario analyses that show how outcomes change under key sensitivities: tariff shifts, bankruptcy rates among brick-and-mortar retailers, consumer spending shocks, and major technology adoption events (e.g., rapid rollout of automated condition assessment). Executives should use these scenarios to set contingency thresholds—trigger points for re-routing inventory, tightening credit to buyers, or accelerating channel diversification.

Closeouts and liquidation channels are becoming a strategic lever for inventory management, margin recovery, and customer experience control. For retail CFOs, logistics directors, private-equity investors, and marketplace operators, the decisions made in 2026 will determine whether surplus inventory becomes a recurring drag on earnings or a source of predictable recovery and even strategic advantage.

PW Consulting’s closeouts study is structured to support these decisions with actionable modules—forecasting tools, commercial playbooks, operational diagnostics, and M&A templates—backed by a granular, proprietary dataset. The public summary above signals the types of insights we offer; the full report and our interactive dashboards contain the complete segmentation, channel economics, and downloadable models that operational teams use to set budgets, negotiate contracts, and prioritize investments.

Trade shows and supplier ecosystems: Events such as ASD Market Week continue to concentrate supplier and buyer activity, surfacing new business models and partnerships among over 250 wholesale closeout suppliers. These venues remain a useful live market signal for pricing and buyer demand shifts.

Policy and supply shocks: Continued tariff volatility and retail balance-sheet stress have materially increased available closeout inventory. Organizations that move quickly to codify contingency pricing and logistics plans will capture disproportionate value.

This release is a strategic preview designed to orient leaders and provoke the right questions for 2026 planning. To access the full datasets, segmentation breakouts, interactive forecast models, and tactical playbooks, please visit the PW Consulting report page where the complete Closeouts Market report and supporting downloads are available. The full subscription includes scenario runners, buyer-seller scoring matrices, and contract templates ready for adaptation.

For senior executives and investment teams seeking an executive briefing or custom sensitivity runs against your portfolio, PW Consulting offers tailored workshops and model‑calibration sessions that map our findings directly to your P&L and operational levers.

For detailed analysis of this topic, please visit the official page:Closeouts Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com