Carpal Tunnel Syndrome Treatment Market: Strategic Imperatives for 2026 — PW Consulting Market Brief

PW Consulting’s latest market study on Carpal Tunnel Syndrome (CTS) Treatment synthesizes five years of historical performance and a seven-year forward view to deliver a concise, decision‑grade playbook for executives, investors, and clinical leaders planning for 2026 and beyond. Built on a quantitative foundation and validated against recent regulatory, reimbursement, and clinical milestones, the brief explains why CTS is transitioning from a predominantly procedure‑driven market to an ecosystem shaped by image‑guided therapy, percutaneous solutions, AI‑enabled diagnostics, and shifting reimbursement frameworks.

Carpal Tunnel Syndrome Treatment Market

Quick market snapshot (high level)

Our analysis shows the global CTS treatment market at an inflection point. The market reached roughly USD 748.6 Million in 2025 and is projected to advance to around USD 784.2 Million in 2026. Over the 2026–2032 forecast horizon, PW Consulting models a compound annual growth rate (CAGR) of approximately 6.12%, resulting in a market size north of USD 1.1 Billion by 2032. Market concentration remains moderate: the top three vendors account for roughly one‑third of market revenues, while the top five control just over half — a structure that supports both consolidation plays and continued innovation by specialist entrants.

Carpal Tunnel Syndrome Treatment Market

Why 2026 is a strategic hinge year

- Reimbursement codification unlocks new pathways. The introduction of a Category I CPT code for percutaneous carpal tunnel decompression effective January 1, 2026, and its associated payment conventions (notably a 0‑day global period and separate reporting of post‑procedure visits) materially alters the economics of ambulatory/day‑of‑service procedures. Organizations that align clinical pathways and billing practices with the new code will capture outsized share in ambulatory and outpatient settings.

- Clinical evidence and regulatory clarity accelerate adoption of image‑guided procedures. Recent regulatory clearances and peer‑review publications in 2025–2026 for ultrasound‑guided and endoscopic systems increase physician confidence and payer receptivity. These approvals create a runway for device makers and health systems to reallocate cases from traditional open surgery to minimally invasive alternatives, subject to local reimbursement policies and credentialing.

- Diagnostic automation reshapes the front-end patient pathway. AI tools that automate median nerve ultrasound metrics lower diagnostic friction, reduce time‑to‑treatment, and enable more efficient triage — critical in markets where access to electrodiagnostic testing is constrained.

What’s in the PW Consulting CTS Treatment Report (practical contents)

- Detailed market sizing and seven‑year forecast with scenario analysis under alternative adoption curves and reimbursement uptake rates.

- Clinical evidence mapping: systematic review of randomized trials, registries, and published case series tied to treatment modalities (open, endoscopic, percutaneous, ultrasound‑guided) and their real‑world outcomes.

- Regulatory and reimbursement playbook: jurisdictional trackers, CPT/Coding implications, Medicare/insurer valuations, and payer negotiation strategies to protect margin while driving volume.

- Competitive and product benchmarking: feature, pricing, and evidence comparison across established OEMs and disruptive entrants, with go‑to‑market sequences for 12‑ to 24‑month launch windows.

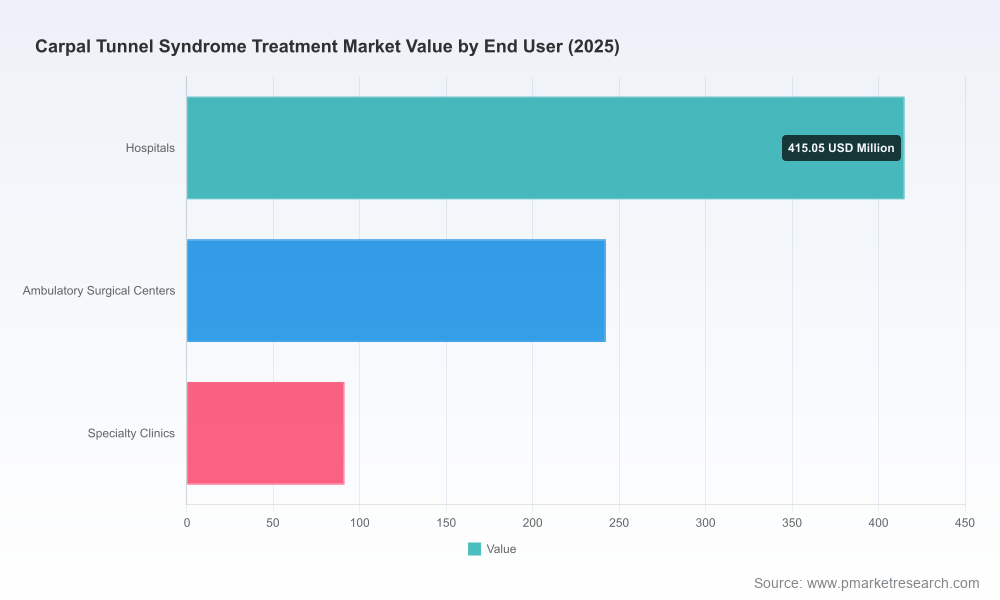

- Commercial opportunity heatmaps and service model recommendations for hospitals, ambulatory surgical centers, and specialty clinics, including referral pathway redesign and bundled payment readiness.

- M&A and partnership screening: a shortlist of capability gaps, strategic bolt‑ons, and licensing opportunities with valuation sensitivity to regulatory and reimbursement milestones.

- Operational playbooks for scale: from sterile supply optimization and reusable/disposable mix decisions to training curricula and clinician credentialing roadmaps designed to limit downtime and accelerate case throughput.

Competitive landscape: leaders, fast movers, and niche specialists

The CTS treatment market features a mix of large orthopedics and surgical capital equipment companies alongside agile innovators focused on visualization, percutaneous access, and point‑of‑care diagnostics. The competitive environment is defined less by monopolistic dominance and more by capability clusters: endoscopic expertise, ultrasound guidance and visualization, small‑form percutaneous devices, and diagnostic AI. Key observations:

Carpal Tunnel Syndrome Treatment Market

- Traditional device leaders (e.g., Stryker, Smith & Nephew, CONMED, Integra, MicroAire): These players leverage broad surgical portfolios, distribution scale, and physician relationships to defend share in endoscopic and instrument‑driven workflows. Their advantages include established hospital contracting channels and integrated service agreements — useful where hospital systems prefer single‑vendor rationalization.

- Endoscopy and soft‑tissue specialists (Arthrex, MicroAire): Firms with dedicated endoscopic hand‑surgery platforms are positioned to convert open‑procedure volumes where clinical evidence and reimbursement favor minimally invasive options. Arthrex’s established coding/reimbursement guidance for endoscopy underscores the value of early payer engagement.

- Image‑guided and percutaneous disruptors (Sonex Health, PAVmed, Trice Medical): Recent regulatory wins and peer‑review publications validate ultrasound‑guided carpal tunnel release as a credible pathway, improving the commercial case for outpatient percutaneous care. Sonex’s FDA 510(k) clearance and subsequent independent publications materially change the competitive calculus for ambulatory settings and office‑based procedures.

- Diagnostic AI and handheld imaging providers (Clarius): AI tools that standardize ultrasound assessment reduce diagnostic variability and create a pull effect for ultrasound‑based therapeutic workflows. Early regulatory clearance of AI tools has simplified adoption conversations with hospital imaging departments and outpatient clinics.

- Niche instrument manufacturers and service providers: A cadre of smaller firms supplies specialized blades, retractors, and single‑use kits. These suppliers are attractive targets for established OEMs seeking to round out procedure bundles or accelerate time‑to‑market for percutaneous and office‑based offerings.

Regulatory and reimbursement dynamics — the tactical checklist for 2026

- Operationalize CPT 64728: update coding manuals, clinical documentation templates, and revenue cycle workflows now to ensure accurate day‑of‑service capture and separate reporting of post‑procedure follow‑ups.

- Leverage evidence to influence payer policy: prioritize prospective registries and real‑world evidence generation for ultrasound‑guided and percutaneous systems to shorten reimbursement lead times.

- Mitigate regulatory risk: maintain disciplined claim language and marketing communications — the FDA’s warning letters in adjacent therapy spaces underscore the consequences of unsubstantiated claims.

- Engage surgical societies and guideline authors: contribute to AAOS and specialty society dialogs to help refine perioperative recommendations (e.g., antibiotic stewardship) and credentialing expectations for new techniques.

Opportunities and risks — executive summary for 2026 resource allocation

Opportunities

- Shift to outpatient/percutaneous care offers margin and throughput upside for ambulatory surgical centers and device makers that can demonstrate shorter recovery and comparable outcomes.

- AI‑enabled diagnostics and handheld ultrasound expand the addressable patient funnel by simplifying triage and minimizing dependence on EMG/NCS in some pathways, particularly in primary care and musculoskeletal clinics.

- Partnerships between OEMs and ultrasound/AI vendors can create bundled offerings attractive to payers and health systems seeking integrated value propositions.

Risks

- Inconsistent payer adoption of new CPT valuations and local coverage determinations could fragment adoption geographically and across care settings.

- Failure to generate comparative clinical evidence may limit adoption of minimally invasive alternatives despite favorable coding; conversely, early adopters face reputational risk if outcomes monitoring is weak.

- Regulatory scrutiny of claims and marketing continues to be a material compliance risk for entrants claiming unproven therapeutic benefits.

Actionable next steps for leadership teams

- Immediate (0–6 months): implement coding and billing updates for CPT 64728; launch pilot registries that capture clinically meaningful endpoints and health economics metrics; align hospital contracting to support ambulatory percutaneous workflows.

- Near term (6–18 months): execute physician education programs tied to credentialing standards; strike partnerships with diagnostic AI vendors to embed point‑of‑care ultrasound in CTS patient pathways; validate service models (office‑based vs. ASC vs. hospital) via AB testing.

- Strategic (18–36 months): pursue targeted M&A to acquire visualization or AI capabilities if evidence confirms superior economics; negotiate value‑based contracts with larger health systems once real‑world evidence demonstrates sustained benefit.

Why PW Consulting’s report matters for 2026

Our study is built for decision velocity. It connects high‑resolution market forecasts (with scenario levers for adoption and reimbursement) to operational playbooks and deal pipelines. For executives deciding where to allocate R&D dollars, how to price and position new products, or whether to pursue M&A, the report translates macro trends into concrete 12–36 month actions — while preserving proprietary subsegment tables and datasets that underpin our conclusions. Those detailed datasets (including granular regional and treatment‑type splits, provider‑level flows, and price elasticities) are intentionally gated to the full report to protect commercial value and to enable bespoke client engagements.

Final note and call to action

2026 represents a rare alignment of reimbursement change, regulatory approvals, and technological maturation for the CTS treatment market. Organizations that combine disciplined evidence generation, coder and clinician readiness, and smart partnerships will capture disproportionate value as the market expands at an estimated 6.12% CAGR over the coming planning cycle. For boards, strategy teams, clinical operations, and investor groups seeking the full toolkit — including the proprietary subsegment analyses, scenario worksheets, and vendor scorecards referenced here — PW Consulting’s comprehensive report is available now.

Contact PW Consulting to request the full report and tailored advisory options that translate this market insight into executable 2026 plans.

For detailed analysis of this topic, please visit the official page:Carpal Tunnel Syndrome Treatment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com