Mp System on a Chip (SoC) Market: Strategic Imperatives for 2026 — PW Consulting Executive Brief

As organizations set budgets and roadmaps for 2026, the Mp System on a Chip market presents both accelerating opportunities and structural risks that will determine winners across consumer, automotive, telecom, and industrial value chains. PW Consulting’s latest market study — grounded in a robust historical dataset (2020–2025) and a 2026–2032 forecast model — frames those decisions with a data-first narrative: the market grew from roughly USD 128.1 billion in 2020 to USD 195.5 billion in 2025 and is on a trajectory to cross approximately USD 363.2 billion by 2032, implying a compound annual growth rate of 9.25% across the forecast horizon. This brief highlights the report’s strategic value to executives while preserving the granular segmentation and vendor share tables that we reserve for the full report.

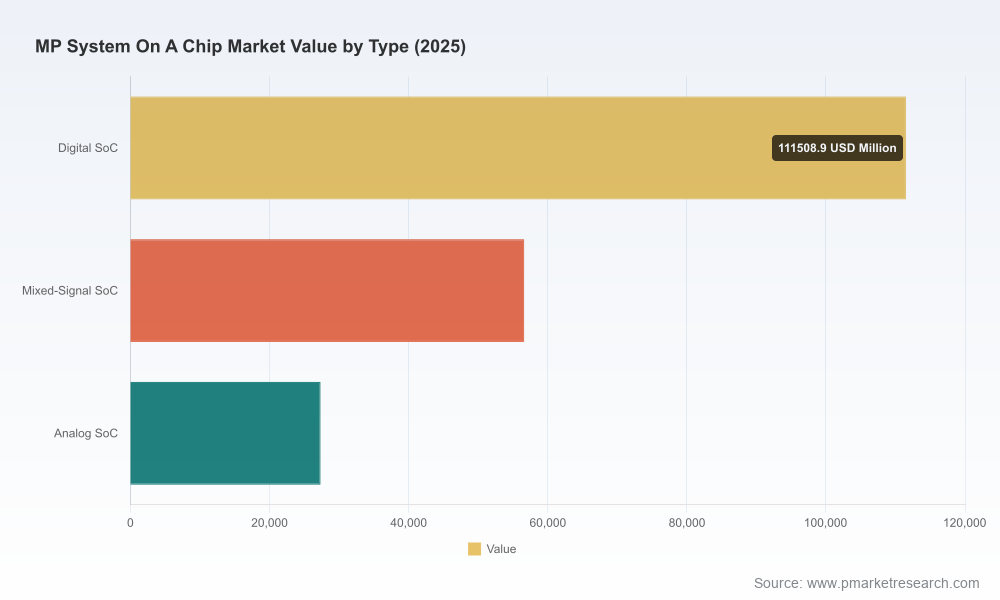

Mp System On A Chip Market

Why this market trajectory matters for 2026 planning

The mid-decade inflection reflects a confluence of trends: accelerated node migration for flagship mobile SoCs, the mainstreaming of heterogeneous integration (chiplets + advanced packaging), the proliferation of embedded AI at the edge, and growing compute intensity across automotive and telecom domains. For a 2026 planning cycle, these dynamics translate into four immediate decision vectors for corporate leaders:

Mp System On A Chip Market

- Technology investment timing — when to commit to advanced node designs, chiplet strategies, or packaging partnerships to avoid obsolescence and cost overruns.

- Supply-chain architecture — how to balance lead foundry relationships with risk-mitigation measures tied to export controls and geopolitical pressures.

- Portfolio prioritization — which end-market adjacencies (e.g., automotive L3/L4, 5G RAN, consumer edge AI) require bespoke SoC features versus off-the-shelf platforms.

- M&A and partner playbooks — where to pursue capability buys (IP, design houses, packaging partners) versus go-to-market alliances with major OEMs and TSMC/other foundries.

Report contents that directly inform boardroom choices

Our full study is designed as an executable tool for 2026 strategy cycles. Key deliverables include:

Mp System On A Chip Market

- Top-down and bottom-up market model with annual historicals and a 2026–2032 forecast — enabling scenario planning under alternative growth, price, and supply assumptions.

- Competitive scorecards and capability matrices for major vendors — covering IP portfolios, node roadmaps, packaging partnerships, and go-to-market strengths.

- Technology adoption timelines — assessing feasibility and commercial readiness for 2nm, chiplet standards (UCIe), and CoWoS-class interposers.

- Supply-chain risk map — mapping critical tool dependencies, country-level exposure to export controls, and mitigation levers (dual-sourcing, buffer inventories, regional fabs).

- Commercial playbooks — tailored GTM and product strategies for consumer, telecom, automotive, and industrial OEMs, including suggested pricing and channel approaches derived from elasticities in our demand model.

- Transaction support materials — valuation benchmarks, synergy templates, and integration checklists for M&A or strategic investments.

To retain the integrity of the market model as an engaged commercial asset, granular regional and application splits, vendor market shares, and certain price-volume tables are exclusively available in the full report.

Competitive landscape — what the leaders’ moves imply for 2026

The SoC landscape is a mix of vertically integrated incumbents, fabless innovators, and IDM/foundry hybrids. Our workbench evaluates each major player across five vectors: node leadership, heterogeneous integration capability, IP breadth (CPU/GPU/AI accelerators), go-to-market reach, and supply-chain control.

- Qualcomm Technologies: A dominant mobile and automotive SoC designer with strong modem and AI acceleration integration. Expect continued leadership in cellular multimode integration and automotive telematics SoCs; their supply plays will hinge on foundry access and packaging partners.

- Apple: Exemplifies vertical integration with proprietary CPU/GPU/Neural Engine stacks and tight software-hardware co-optimization. Apple’s approach continues to raise the bar on SoC power-efficiency and system-level performance, pressuring competitors to invest in differentiated acceleration and memory architectures.

- MediaTek: Demonstrated rapid process adoption and cost-competitive value propositions. Recent tape-out activity targeting 2nm indicates aggressive product cadence and continued pressure on pricing for mainstream mobile segments.

- Samsung: Offers both SoC designs and foundry capacity, providing unique options for customers that value an integrated supply chain; their packaging and memory ecosystem (HBM, advanced interposers) are strategic advantages for high-bandwidth applications.

- AMD & NVIDIA: Both bring high-performance compute and accelerator IP into SoC architectures, advancing edge and data-center constrained SoC designs. NVIDIA’s Orin/Tegra lineage is notable for automotive and robotic applications, while AMD’s integration of CPU/GPU in EPYC/Ryzen platforms informs SoC-level consolidation for servers and edge compute.

- Intel: Leveraging IDM assets, Intel’s SoC offerings will be judged on process competitiveness and its capacity to win embedded/server SoC designs that require x86 compatibility or robust I/O integration.

- Broadcom, NXP, STMicro, TI: Focused plays across networking, automotive, and industrial segments. Their strengths in connectivity, mixed-signal integration, and automotive-grade qualification provide defensible niches as compute decentralizes.

- OmniVision & Socionext: Represent specialist SoC/system integrators for imaging and embedded verticals, illustrating opportunities for bespoke solutions in automotive vision and industrial imaging.

Market concentration metrics also signal strategic posture: a moderate-to-high concentration among the top-tier vendors (CR3 ≈ 48.7%; CR5 ≈ 62.1%) underscores a market where scale, IP breadth, and foundry relationships confer material advantage — yet sufficient room exists for focused challengers to capture niche growth through specialization and fast time-to-market.

Recent industry developments with near-term implications

- Process node adoption: Industry movements toward 2nm in 2026 (including leading smartphone SoC roadmaps and supplier tape-outs) will compress design windows, raise NRE for leading-edge products, and shift bargaining power toward foundries and advanced packaging houses.

- Advanced packaging & CoWoS: High-yield advanced packaging enabling multi-chip HBM stacks reduces system latency and increases achievable compute per watt. Design teams must decide whether to optimize around monolithic die or heterogeneous assemblies.

- Standards & chiplet ecosystems: Active standardization efforts (e.g., UCIe) lower the integration barrier for heterogeneous SoC stacks, but they also require investment in ecosystem-compatible IP and interposer strategies.

- Regulatory & incentive landscape: Export control regimes and national incentive programs such as the CHIPS Act materially reshape capital allocation decisions — favoring local fabs, strategic inventory planning, and partner selection that aligns with geopolitical risk tolerance.

Practical strategic playbooks for 2026

Based on the report’s findings, PW Consulting recommends three prioritized playbooks for 2026 initiatives. Each playbook includes concrete first-step actions that leadership teams can deploy within 90–180 days.

- Design Leadership Playbook

- Run a node-cost vs. benefit analysis for flagship products using our scenario models to determine which SKUs justify advanced-node NRE.

- Invest in modular IP and chiplet-friendly interfaces to shorten time-to-market while preserving performance scaling.

- Form cross-functional partnerships with packaging vendors to lock in assembly slots and co-optimize thermal and power envelopes.

- Manufacturing & Resilience Playbook

- Implement a three-tier foundry strategy: primary advanced-node partner, backup mature-node foundry, and a regional fab for strategic products sensitive to export constraints.

- Prioritize dual-sourcing for long-lead tooling and critical test houses; negotiate yield- and volume-based pricing to reduce margin volatility.

- Leverage government incentive programs to offset incremental capital for regionalizing production where sensible.

- Commercial & Market Acceleration Playbook

- Segment product roadmaps into “platform” and “specialty” builds to balance volume-driven margins with higher-margin bespoke solutions for automotive and industrial clients.

- Align sales compensation and channel strategies to prioritize early design wins in high-growth verticals (embedded AI, ADAS, 5G infrastructure).

- Prepare go-to-market partnerships with cloud and software ecosystem players to accelerate adoption of SoC-enabled services and firmware monetization.

How PW Consulting’s report supports executable 2026 decisions

Executives require both high-level conviction and granular inputs to make capital, R&D, and commercial choices. The full Mp SoC Market report provides:

- Stress-tested financial models and sensitivity tables to quantify expected returns under alternative node, yield, and price scenarios.

- Vendor-specific risk assessments and negotiation playbooks calibrated to current concentration dynamics and recent supplier events.

- Detailed technology timelines and readiness assessments for 2nm, UCIe-enabled chiplets, and CoWoS-level packaging with practical checklists for integration.

- Customizable dashboards for board-level reporting and procurement negotiation templates to accelerate supplier engagements.

Next steps

PW Consulting’s Mp SoC Market report is purpose-built to move conversations from strategic intent to operational execution in 2026. For executives preparing capex proposals, product roadmaps, or M&A funnels, the report offers the combination of market-level clarity and actionable, vendor-specific counsel required to de-risk decisions. Detailed regional and application splits, vendor market share tables, and downloadable model workbooks are published in the full report and accessible via our report page.

Contact PW Consulting to schedule a briefing or to request the full dataset and tailored scenario workups for your product portfolio. Our analysts are available for board-level presentations and hands-on implementation support to translate these market dynamics into measurable business outcomes.

For detailed analysis of this topic, please visit the official page:Mp System On A Chip Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com