Varicose Eczema Treatment Market Overview: Key Drivers and Challenges

Other |

2026-06-23 11:43:02

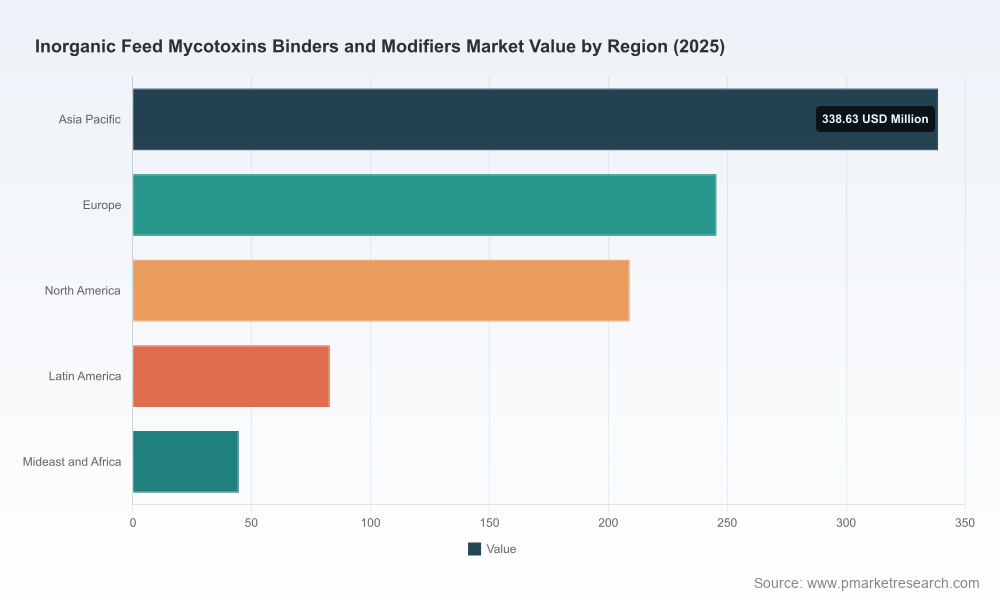

As the livestock and aquaculture industries confront intensifying mycotoxin pressure, inorganic mycotoxin binders and modifiers are transitioning from niche supplements to essential risk-management inputs. PW Consulting’s new market study — anchored on a 2025 base year with a historical window covering 2020–2025 and a forecast through 2026–2032 — quantifies this transition. The global market, measured in USD million, expanded materially over the historical period and our forward-looking modelling projects steady growth at a compound annual growth rate (CAGR) of 5.15% through the forecast horizon. Market concentration metrics point to a fragmented but consolidating landscape (CR3 ≈ 28.5%; CR5 ≈ 39.2%), underlining both competitive intensity and transaction opportunity for scale-seeking players.

Inorganic Feed Mycotoxins Binders And Modifiers Market

Actionable foresight for capex and product roadmaps: manufacturers and ingredient suppliers need repeatable models to size incremental volumes and evaluate ROI on novel binder formulations versus conventional clays.

Inorganic Feed Mycotoxins Binders And Modifiers Market

Regulatory readiness as a revenue lever: evolving approvals and EFSA-style efficacy requirements elevate the importance of dossier investment and post-market field evidence as competitive barriers.

Inorganic Feed Mycotoxins Binders And Modifiers Market

Sourcing and margin protection: with feed-grade clays and activated carbons as primary inputs, supply-chain design becomes as critical as R&D in protecting margins and fulfilment.

M&A and partnership prioritization: fragmented market concentration highlights targets for bolt-on acquisitions and co-development alliances that rapidly expand technical breadth and geographic reach.

Market sizing and high-frequency trend models (USD million basis), with scenario-based forecasts to 2032 that allow users to stress-test assumptions on adoption, price deflation, and regulatory shifts.

Demand-driver decomposition linking mycotoxin prevalence, feed-intensity metrics, and protein-producer economics to binder uptake.

Supply-side diagnostics: raw-material sourcing maps, quality variance scoring for mined clays, cost-to-serve overlays, and procurement levers to stabilise input cost exposure.

Regulatory and efficacy matrix: a concise guide to regional approvals, dossier expectations, and acceptable use-level boundaries — enabling legal and regulatory teams to prioritise jurisdictions and product claims.

Competitive benchmarking and capability heatmaps across product portfolios, technical claims (polar vs non-polar mycotoxins), and commercialization reach.

M&A playbook and valuation frameworks built for realistic multiples in a mid-consolidation market — including an acquisition screening checklist and integration sprint templates.

Go-to-market templates for feed additive suppliers: segmentation strategies, distributor economics, and pilot-to-scale roll-out checklists.

Note: To preserve commercial sensitivity and strategic advantage, the report presents granular segmental tables, regional splits, and proprietary price curves exclusively in the subscriber appendices.

Raw-material fundamentals: inorganic binders are primarily derived from mined aluminosilicates and related minerals — bentonite, montmorillonite, HSCAS, sepiolite, zeolites — plus activated carbons and diatomaceous earth where formulators require broader sorptive profiles. These inputs have inherently variable quality characteristics (cation exchange capacity, particle size distribution, thermal stability) that drive formulation performance and sourcing complexity.

Regulatory environment: jurisdictions with stringent feed-safety regimes demand not only demonstration of mycotoxin reduction (e.g., aflatoxin mitigation) but also confirmation that nutrient bioavailability and animal safety are uncompromised. In several major markets, specific mineral binders have pathway precedents (authorisations for defined uses), but these precedents do not remove the need for robust, product-specific dossiers.

Supply-chain and ESG exposure: mining footprints, energy intensity of thermal processing, and trace element content are rising considerations among feed formulators and end-customers. Players with traceability, lower-carbon processing, and community engagement practices will command premium access in sensitive channels.

Substitution and technology risk: while clay-based binders remain the dominant technical approach, ongoing research into engineered materials, surface-modified sorbents, and combined adsorbent–biotransformation systems creates a two-track competitive landscape — incumbent mineral binders versus higher-cost, differentiated modifiers.

The competitive set comprises mineral specialists, integrated feed-ingredient groups, and smaller clay-focused merchants. A few illustrative profiles point to commercial and technical playbooks worth noting:

Amlan International (Oil-Dri Corporation of America) — product differentiation via proprietary mineral processing. Amlan’s Calibrin-A and Calibrin-Z lines demonstrate a dual focus: rapid binding of polar toxins and expanded broad-spectrum sequestration through thermally processed montmorillonite. Recent market activity (product introductions and regional partnerships) underscores their strategy to couple formulation science with local commercial partners to accelerate adoption.

Kemin Industries — breadth and scale in feed additives. Kemin’s TOXFIN range illustrates a strategy of leveraging activated adsorbents and argillaceous minerals to deliver broad-spectrum efficacy claims while drawing on large-scale commercial channels to drive penetration in feed rations.

Tolsa — mineral-centric, differentiated blends. Tolsa’s formulations that combine bentonite/sepiolite and activated carbon show the industry’s trend toward blended adsorbents that improve performance across toxin polarities and operational feed applications.

Bentoli Inc. — focused clay-based solutions aimed at livestock and poultry with an emphasis on practical on-farm results. Smaller, specialist suppliers like Bentoli are important acquisition targets for larger players seeking technical portfolios and regional customer access.

Strategically, suppliers are taking two routes: (1) scale and distribution to make conventional binders a commoditised, low-friction input; or (2) technical differentiation to command premium prices in feed rations where efficacy and safety documentation are critical. Both routes are viable — but they require different capital, regulatory, and commercial investments.

Prioritise product dossiers in target jurisdictions: allocate near-term R&D and field-trial budgets to build efficacy and safety evidence aligned with EFSA-style expectations; early dossier readiness reduces time-to-market and creates a de facto barrier to late entrants.

Secure diversified raw-material streams: implement dual-sourcing for critical clays and establish indexed contracts or hedging approaches to protect against commodity shocks and quality variability.

Adopt a layered go-to-market strategy: combine direct technical service teams for strategic accounts with distributor networks for broader feed-mill penetration — this balances margin and reach.

Pursue bolt-on acquisitions that fill capability gaps: the optimal targets are those offering either novel adsorbent chemistry, local regulatory dossiers, or distribution in fast-growing protein-production corridors.

Invest in end-to-end proof points: complement laboratory adsorption metrics with farm-level performance, nutrient-impact studies, and independent field validations — these reduce buyer reluctance and support premium positioning.

Build ESG narratives around sourcing and processing: traceability, lower-temperature processing, and community programmes convert environmental risk into commercial advantage with sensitive feed buyers.

Base case (most likely): steady, mid-single-digit market growth driven by incremental adoption in higher-risk feed chains, continued reliance on clays, and gradual regulatory tightening for evidence of efficacy.

Acceleration case: favourable regulatory harmonisation and a series of high-impact mycotoxin events drive rapid binder adoption and premium pricing for validated products — beneficiaries are branded suppliers with robust dossiers and distribution scale.

Disruption case: a technology leap (engineered sorbents or enzymatic modifiers) captures share from traditional clays; incumbents either adapt via licence/acquisition or cede premium segments.

Our report provides quantitative triggers and playbooks for each scenario to help executives pre-position investments, manufacturing capacity, and M&A war chests.

PW Consulting’s Inorganic Feed Mycotoxins Binders and Modifiers Market report combines proprietary market models (USD million basis), regulatory matrices, supplier capability maps, and M&A screening tools specifically designed to inform board-level strategy and commercial execution in 2026. For executives preparing budgets, evaluating acquisition targets, or building regulatory submission priorities, the report functions as both an evidence base and a tactical playbook.

To access the full dataset — including segmented forecasts, regional deployment scenarios, unit-price modelling, and the proprietary analyst console — please visit the PW Consulting report page where subscribers can download the executive report, schedule a briefing with our industry team, or commission a tailored workshop aligned to your strategic priorities.

For detailed analysis of this topic, please visit the official page:Inorganic Feed Mycotoxins Binders And Modifiers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com