Modular Storage Area Network (SAN) Solutions Market Size, Share & Growth Forecast 2026–2034

Technology |

2026-06-26 10:53:59

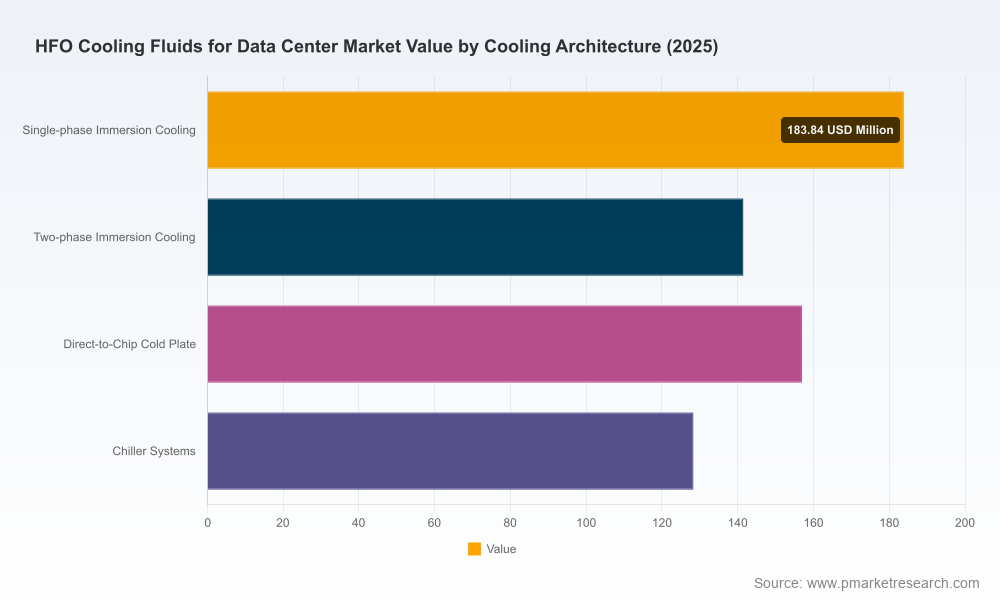

PW Consulting is pleased to announce the release of our new market intelligence brief, "Hfo Cooling Fluids For Data Center Market." Built on a rigorous analysis of historical trends (2020–2025) and forward-looking scenario work for 2026–2032, this research equips corporate leaders, procurement teams, data center operators, and investors with the strategic context they need to make high-conviction decisions in 2026. The market is undergoing rapid transformation: after accelerating from a mid‑hundreds million USD base in 2020 to an estimated USD 610.5 Million in 2025, our model projects a compound annual growth rate (CAGR) of 18.02% across the 2026–2032 forecast window — driving the market toward roughly USD 1.95 Billion by 2032.

Hfo Cooling Fluids For Data Center Market

Decision timetables in 2026 will be materially shaped by three simultaneous forces: regulatory tightening, supplier consolidation, and rapid technology maturation. New regulatory thresholds (notably a U.S. EPA Technology Transitions rule that institutes a GWP ceiling for certain cooling equipment beginning in 2027, alongside ongoing international drivers such as Kigali and EU F‑Gas frameworks) are compressing the window for technology selection and qualification. At the same time, the supply base has become highly concentrated — our market concentration analysis shows the top three suppliers account for roughly 72% of market revenues, and the top five nearly 88% — creating both risk and opportunity for buyers and entrants. Finally, product maturity in two‑phase immersion, single‑phase immersion, and refrigerant‑based chillers is enabling deployment in higher-density architectures, accelerating adoption curves across hyperscale and edge deployments.

Hfo Cooling Fluids For Data Center Market

This is not a headline deck. The report synthesizes market sizing, supplier economics, and practical playbooks into a single deliverable designed for executives executing in 2026:

Hfo Cooling Fluids For Data Center Market

The HFO cooling fluids ecosystem is increasingly dominated by a handful of global incumbents and specialized players. Our competitive diligence profiles suppliers across commercial readiness, manufacturing footprint, product compatibility, and go‑to‑market partnerships. Highlights include:

Recent developments reinforce the pace of market consolidation and qualification activity. During 2025, we observed product qualifications with major SSD and server OEMs, strategic manufacturing alliances to secure scale, and capacity ramp‑ups aimed at meeting accelerating demand. These moves shorten lead times for qualified fluids but also increase the bargaining power of suppliers that can guarantee availability and product compatibility.

Regulatory policy is the external shock that most meaningfully changes capital and procurement outcomes in 2026. The U.S. EPA’s Technology Transitions rule sets a de facto deadline for equipment selection by establishing GWP limits for new systems beginning in 2027. Parallel international regimes — the Kigali Amendment, the EU F‑Gas regime, and regionally emerging quota systems — accelerate the phasedown of legacy HFCs and favor ultra‑low‑GWP HFOs. For corporate decision‑makers, this means compliance risk is now an input to technology selection rather than an afterthought; late adoption risks both replaced inventory and limited installation windows.

On the supply side, HFO production is exposed to price volatility in fluorinated intermediates and olefins. Producers have already reacted: we tracked supplier price adjustments in 2025 tied to feedstock cost inflation, and our scenario work models the effect of sustained raw material price shocks on TCO and supplier viability. Procurement strategies that ignore input‑price volatility — or rely solely on spot purchases — will be disadvantaged.

Based on our quantitative models and supplier due diligence, PW Consulting recommends the following course of action for companies planning deployments, procurement, or investments in 2026:

Executives tell us they need intelligence that closes the gap between insight and execution. This report provides that bridge: it combines a granular market forecast (anchored to a 2025 base and a detailed 2026–2032 projection), actionable procurement and engineering checklists, and an M&A/partnership scoring rubric mapped to real supplier capabilities. The goal is to enable decisions that are defensible under regulatory pressure, resilient to supply shocks, and optimized for data‑center operational metrics such as PUE, water use, and server thermal reliability.

To maintain the utility of this brief as a “trailer,” we have deliberately withheld detailed subsegment revenue tables and granular regional breakdowns from this release. The full report includes those line‑by‑line decompositions, sensitivity runs, supplier scorecards, and downloadable templates that you will need to operationalize strategy in 2026.

PW Consulting’s Hfo Cooling Fluids For Data Center Market report is targeted at leaders who must make binding procurement, engineering, or investment decisions in 2026. If your organization is evaluating cooling technology selection, negotiating supplier terms, planning manufacturing investments, or preparing for regulatory compliance, this report is designed to reduce uncertainty and accelerate execution.

For access to the complete dataset, subsegment forecasts, and client‑only advisory services—including bespoke supplier diligence, contract negotiation support, and regulatory scenario workshops—please consult the PW Consulting distribution channels to obtain the full report and schedule a briefing with our industry practice.

For detailed analysis of this topic, please visit the official page:Hfo Cooling Fluids For Data Center Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com