IoT in Energy 2026: A Strategic Playbook for Executive Decision-Making

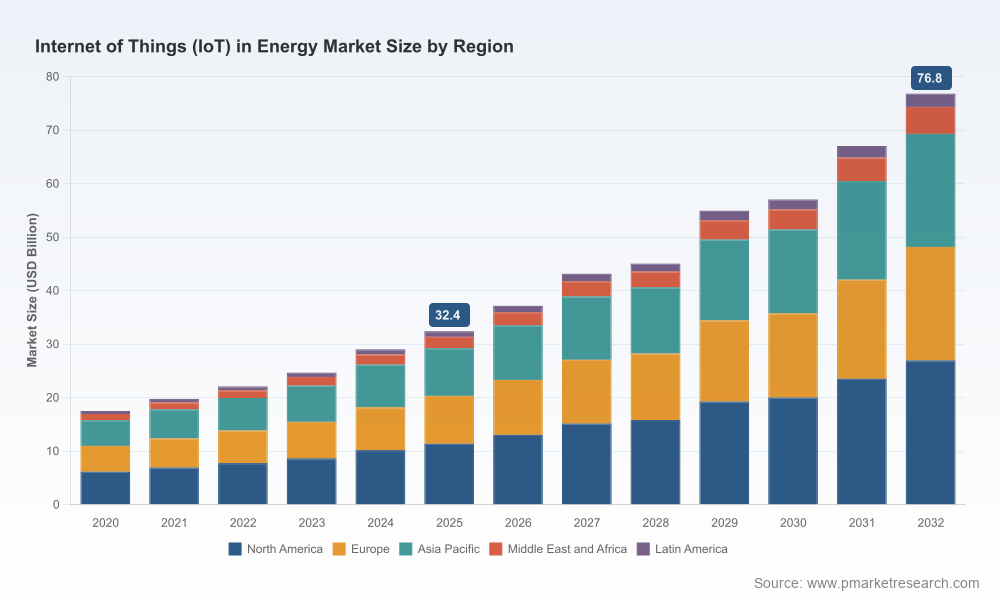

As energy systems accelerate their digital transformation, the Internet of Things (IoT) is no longer an experimental add‑on — it is a structural capability that shapes asset economics, operational resilience, and regulatory compliance. PW Consulting’s latest market study on IoT in Energy (base year 2025) charts this shift with a clear, investible narrative: after expanding from a measured base in 2020, the market scaled meaningfully through 2025 and is forecast to grow at a compound annual growth rate of 13.08% across our 2026–2032 horizon. By 2026 the market size breaks through a new threshold on the way to a multi‑decade transformation, and by 2032 the scale of IoT‑enabled energy revenues implies dramatically deeper integration across grids, generation, storage and the distributed edge.

Internet Of Things Iot In Energy Market

Why this brief matters for 2026 corporate decisions

- Acceleration in deployment and value capture: The market’s sustained double‑digit CAGR underscores an expanding opportunity window for buyers and vendors alike — not just for pilot projects, but for scaled rollouts that alter cost curves for operations and capital allocation.

- Regulatory and investment tailwinds: Global energy investment dynamics — with major flows into renewables, grids and storage — are creating new use cases where IoT becomes a prerequisite for visibility and control. National directives focused on grid reliability and security further compress timelines for modernization.

- Technology maturation converges with commercial models: Connectivity ecosystems (including large‑scale LoRaWAN deployments), edge computing standards, and commercial IoT platforms have matured to the point where the primary barriers are business‑model alignment and organizational change, not capability.

What our report delivers — practical, action‑ready content

This report is built as an executable toolkit for 2026 planning cycles. It combines rigorous market modeling with tactical assets designed for procurement, strategy and M&A teams. Highlights include:

Internet Of Things Iot In Energy Market

- Proprietary market model and scenario engine (2026–2032) that allows organizations to stress‑test investments against alternative adoption and technology paths without exposing our underlying segmentation datapoints.

- A vendor evaluation framework and a comparator matrix examining platform capabilities, edge‑to‑cloud architecture, data governance, and integration effort — designed for RFP shortlisting and vendor negotiation.

- Deployment playbooks and KPIs for pilots and scale‑up: device lifecycle management, telemetry quality metrics, OTA update strategies, and operational handover procedures to minimize ramp risks.

- IP‑grade blueprints for IT/OT convergence, secure edge architectures, and data ops pipelines that align with common utility procurement cycles and regulatory reporting windows.

- ROI and TCO models tuned to energy use cases (grid automation, asset performance, distributed resource management) with sensitivity analysis for latency, device churn, and market price volatility.

- Regulatory tracker and compliance checklist focused on emerging reliability mandates, data sovereignty regimes and standardization efforts that materially affect deployment timelines.

- Case studies and vendor negotiation templates that translate technology choices into contract terms and performance SLAs.

Market dynamics and context — what’s changing in 2026

- Massive connectivity scale: LPWAN ecosystems have reached production scale, with publicly reported deployment counts in the low‑hundreds of millions globally; utilities are among the largest adopters for smart applications. This changes the economics of metering, grid edge intelligence and distributed monitoring.

- Capital flows into system infrastructure: Global energy investment is running at multi‑trillion dollar levels, with a substantial share dedicated to renewables, grids, storage and the enabling infrastructure that IoT augments. That capital creates projects and partnerships where IoT is an embedded deliverable rather than an optional feature.

- Policy and reliability mandates: Several jurisdictions have introduced executive actions and regulatory directives that prioritize grid reliability and resilience, accelerating digitalization and increasing the demand for observability and automated control.

- Edge and standards momentum: Open edge projects and industry consortia are producing interoperable components for carbon accounting, secure telemetry and local analytics — reducing integration friction for new deployments.

Competitive landscape — how to read vendor positioning

The IoT in Energy ecosystem is populated by legacy industrial systems integrators, telecom and semiconductor suppliers, and software platform specialists. Market concentration remains relatively low compared with other industrial segments, reflecting a fragmented competitive field and significant room for vertical specialists and ecosystem integrators. Key vendors we profile in the report include:

Internet Of Things Iot In Energy Market

- Siemens AG (Munich) — Strength in digital twins, grid automation and industrial IoT platforms positions Siemens as a prime integrator for utilities and large industrials looking to couple system modelling with operational controls. Their incumbency in substations and control centers is a strategic lever for cross‑sell.

- Schneider Electric (Rueil‑Malmaison) — Schneider’s EcoStruxure architecture focuses on energy management across buildings and grid edge use cases. Their emphasis on efficiency and renewable integration makes them a logical partner for distributed energy projects and building‑to‑grid orchestration.

- ABB Ltd. (Zurich) — ABB’s ABB Ability portfolio brings deep OT expertise and a strong position in asset performance management and grid stability applications; they are a contender where high‑availability systems and industrial controls are required.

- GE Vernova / GE Digital (Cambridge, MA) — With industrial IoT and ADMS capabilities, GE bridges generation and distribution use cases, especially where utilities seek to integrate asset performance with grid management.

- Honeywell (Charlotte, NC) — Honeywell’s strength is in combined building and industrial energy management, leveraging connected sensors and operations platforms for continuous optimization and fault detection.

- Cisco Systems (San Jose, CA) — Cisco is focused on networking, secure edge compute and integration services; for utilities prioritizing secure, resilient communications, networking incumbents are a strategic consideration.

- Hitachi Energy (Zurich) — With recognition in industrial IoT platforms, Hitachi Energy is increasingly relevant for grid automation and digital substations, especially where utilities aim to modernize protection and control systems.

- Itron and Landis+Gyr — Focused specialists in metering and AMI remain central to mass‑market deployments at the grid edge and are favored partners for utilities executing meter modernization programs.

- Semtech (Sierra Wireless lineage) — Suppliers of connectivity modules and IoT radios anchor the device layer, and their technology choices influence device economics and network design.

For buyers, the competitive choice is increasingly about systems integration capability, data‑ops maturity, and the ability to convert telemetry into operational decisions — less about isolated device price. For vendors, differentiation will hinge on platform openness, go‑to‑market partnerships and outcome‑based commercial models.

Strategic recommendations for 2026 planners

- Move from pilots to portfolio thinking: Align IoT initiatives with asset replacement cycles and regulatory milestones so investments compound across projects rather than exist as stranded pilots.

- Prioritize data‑ops and standards: Secure, standardized telemetry and identity at the device‑edge reduce integration costs and accelerate multi‑vendor deployments. Invest in data quality pipelines and model governance early.

- Adopt modular procurement: Separate connectivity, device hardware, platform services and analytics into discrete contracting elements to retain optionality and accelerate vendor swaps without system rip‑and‑replace.

- Plan for cyber resilience and compliance: Regulatory scrutiny and reliability mandates require demonstrable security posture and incident response plans; budget for lifecycle security beyond initial deployment.

- Look for M&A and partnership signals: Expect consolidation around platform capabilities and cloud/edge orchestration — prioritize partnerships that shorten time‑to‑value and preserve IP flexibilities.

How to use the full PW Consulting report

The public brief you are reading is intentionally a high‑value preview. The full report contains our proprietary market model, a customizable forecast workbook, the complete vendor scoring matrix, detailed implementation playbooks, and confidential interviews with utility CTOs and procurement leads. It also includes scenario outputs that map investment timing to NPV and operational KPIs so boards and investment committees can assess tradeoffs with precision.

Executives preparing 2026 budgets will find the full deliverables particularly valuable for capital allocation, vendor negotiation, and regulatory impact assessment. If your organization is evaluating large‑scale rollouts, grid modernization programs, or distributed energy orchestration, the report provides the empirical underpinnings and tactical instruments to move from intent to execution.

Conclusion — act with urgency, plan with rigor

IoT in energy is entering a phase where scale, not novelty, determines winners. The growth trajectory we observe — driven by expanding deployments, technology maturation, and massive infrastructure investment — favors organizations that combine prudent financial discipline with an aggressive modernization agenda. PW Consulting’s IoT in Energy report is designed to be the playbook for that agenda: selective on detail in this public summary, comprehensive and operational in the full deliverable.

For senior teams needing a condensed executive workshop, vendor negotiation templates, or a tailored forecast for a specific asset class, our advisory team can overlay the PW model on your balance sheet and operational plans to generate a decision‑grade roadmap for 2026.

For detailed analysis of this topic, please visit the official page:Internet Of Things Iot In Energy Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com