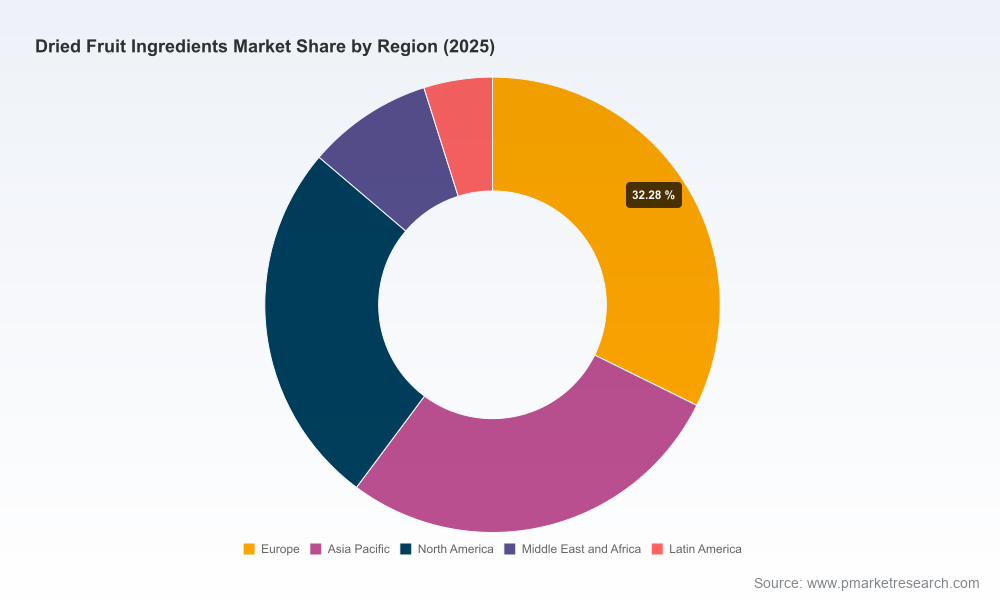

Dried Fruit Ingredients Market: Strategic Roadmap for 2026 Decision‑Makers

Executive snapshot

As global food manufacturers and ingredient buyers set budgets and strategic priorities for 2026, the dried fruit ingredients market presents a compelling, steady-growth opportunity underpinned by shifting consumer preferences and persistent supply‑side pressure. Our 2025‑base analysis shows the global market at approximately USD 9,547.4 Million in 2025, with a projected compound annual growth rate (CAGR) of 5.45% across the 2026–2032 forecast horizon. By 2032 the market is forecast to approach USD 13,842.4 Million, reflecting resilient demand for natural, value‑adding inclusions in bakery, snacks, cereals, dairy and functional food formulations.

Dried Fruit Ingredients Market

Why this matters for 2026 strategy

- Capital allocation and portfolio prioritization: A mid-single‑digit CAGR indicates steady expansion rather than explosive disruption; firms must therefore align investment pacing (capacity, R&D, M&A) to capture volume growth while protecting margin through higher value‑added SKUs.

- Sourcing and procurement resilience: Volatility in agricultural yields and grower economics means procurement teams should move beyond spot buying toward integrated contracts, origin diversification, and indexed pricing mechanisms.

- Product innovation and premiumization: Consumers continue to reward clean‑label, minimal‑processing, and functional claims; ingredient suppliers and formulators that convert basic dried fruit into convenience‑friendly, nutrition‑forward formats will capture outsized value.

- Regulatory and reputational risk management: Labeling rules and food safety incidents have real commercial impact; active compliance roadmaps and traceability investments are now table stakes for market access and brand protection.

Report overview — what PW Consulting delivers to your team

This market study combines market sizing, trend analytics, supplier benchmarking and executable playbooks designed to be used directly by commercial, procurement and R&D teams. Highlights include:

Dried Fruit Ingredients Market

- Top‑line market trajectory and scenario modeling (base case plus upside/downside stress scenarios through 2032) to support capital planning and sensitivity analysis.

- Demand driver diagnostics segmented by channel and formulation need, with implications for pricing, SKU design and co‑marketing strategies.

- Supplier scorecards and competitive positioning frameworks that translate observable moves (capacity, innovation, certifications) into risk/opportunity maps for sourcing managers.

- Procurement playbook: contract templates, hedging and indexation approaches, lead‑time optimization and supplier diversification pathways tailored to perishable‑derived ingredient markets.

- R&D and formulation toolkit: process guidance for ingredient conversion (dicing, pureeing, infusion), clean‑label alternatives, shelf‑stability trade‑offs, and cost‑in‑use calculators.

- M&A screening and inorganic growth playbook, including target archetypes, due diligence checklists and integration pitfalls specific to dried‑fruit upstreams and co‑packing arrangements.

- Regulatory compliance checklist and recall readiness guide, covering labeling, added sugar disclosure, traceability and crisis communications templates.

- Interactive, downloadable models that let teams run custom scenarios without exposing the granular proprietary splits in this public release.

Market dynamics shaping 2026 decisions

Three broad dynamics will dominate decision‑making next year:

Dried Fruit Ingredients Market

- Demand sophistication: Consumers continue to demand snacks and meal components with natural ingredients, recognizable origins, and functional benefits. This is pushing product developers to favor dehydrated inclusions that deliver texture, natural sweetness and perceived health equity over artificial ingredients.

- Supply fragility and cost pressure: Agricultural realities are increasingly reflected in ingredient availability and pricing. Reported grower returns and crop‑level fluctuations—driven by weather variability, labor dynamics and regional yields—underscore the need for procurement strategies that blend long‑term contracting with tactical sourcing flexibility.

- Regulation and food safety scrutiny: Labeling changes requiring clearer disclosure of added sugars and serving sizes have been in effect for several years and continue to influence formulation and marketing claims. Meanwhile, recent high‑profile recalls in the category reinforce the importance of upstream traceability and rapid response protocols.

Competitive landscape — how leading suppliers are positioning

The dried fruit ingredients market exhibits moderate concentration; the top three suppliers account for a material but not dominant share of the market, and the top five incrementally increase that concentration. This competitive structure creates space for both scale players and specialized premium producers.

Across the industry, we observe distinct strategic archetypes:

- Scale, commodity leadership: Established raisin and dried grape specialists remain focused on efficient processing and wide distribution, leveraging scale to serve large industrial bakers and cereal manufacturers.

- Value‑added innovation: Several mid‑sized processors emphasize productization—diced forms, infused/seasoned formats, and purée concentrates—targeting convenience manufacturers and premium snack brands.

- Niche, provenance and premium play: Firms with differentiated fruit varieties or origin stories position toward yogurt, artisan bakery and craft confectionery segments where premiumization and traceability command higher margins.

Illustrative vendor moves from the last 18 months reveal how these archetypes translate into action:

- A processor showcased low‑moisture diced blends at a leading industry expo to signal readiness for high‑throughput bakery lines requiring extended shelf‑stability and dough compatibility.

- A prune specialist launched a branded bits product aimed squarely at large‑scale bakers and nutrition bar manufacturers—an example of converting raw fruit into a category‑friendly, co‑branded ingredient.

- Another producer emphasized third‑party certifications early in the year, reflecting how credentialing continues to be a differentiator for export markets and premium domestic buyers.

For buyers and investors, the key takeaway is tactical: match your supplier archetype to your go‑to‑market strategy. Large CPG firms typically prefer scale and supply assurance, while premium entrants and private labels will trade volume for provenance, innovation and co‑development capabilities.

Risks & tail events that must be stress‑tested

- Agronomic shocks: Droughts, heat stress and pest pressures can compress yields and force origin shifts; scenario models in the report quantify the P&L impact of production losses and replacement sourcing.

- Trade and tariff exposure: Trade measures have previously altered flows in the category and can rapidly shift landed costs; an earlier round of tariffs demonstrates the asymmetric effects of trade policy on import‑reliant formulations.

- Food safety incidents: Recalls, even when limited in scope, create outsized reputational and logistical burdens. The report includes a recall‑readiness module and communications playbook to minimize downstream disruption.

How procurement, R&D and strategy teams should use this research in 2026

The practical value of this study lies in its immediate operational applicability. Recommended first‑quarter actions for cross‑functional teams include:

- Run the report’s scenario models with your product mix to quantify margin sensitivity to commodity price swings and origin substitution.

- Use supplier scorecards to re‑rank current vendors against resilience criteria (traceability, certification, capacity, lead time) and initiate targeted dual‑sourcing where exposure is high.

- Apply the R&D toolkit to reformulate one high‑volume SKU to a lower‑sugar or functional variant using fruit inclusions, and track cost‑in‑use versus consumer willingness‑to‑pay.

- Prioritize a small M&A shortlist using our target archetypes—look for dehydrators with co‑packing capabilities or branded synergies that accelerate route‑to‑market.

What we intentionally withhold in this public summary

In keeping with a “preview” approach, this release highlights strategic directions and illustrative findings without releasing the full, granular segmentation and proprietary supplier metrics that support transactional decisions. The comprehensive report includes detailed regional splits, fruit‑type and application level breakdowns, company scorecards with comparative KPIs, and downloadable financial models—data we reserve for subscribers and licensed purchasers to preserve commercial value and integrity.

Next steps — making the research operational for your team

For executive teams planning 2026 initiatives, the path is clear: convert strategic intent into quantifiable actions by integrating the report’s scenario models into budgeting cycles, reengineering sourcing strategies to reduce single‑origin exposure, and accelerating product development toward the highest‑value inclusion formats.

To access the full dataset, company scorecards, and the interactive scenario tools that support rapid, board‑level decisionmaking, please visit our report landing page and request the full Dried Fruit Ingredients Market research package. PW Consulting also offers bespoke workshops to tailor the study’s insights into procurement playbooks, product roadmaps and M&A pipelines—services designed to translate market visibility into measurable commercial advantage in 2026.

For detailed analysis of this topic, please visit the official page:Dried Fruit Ingredients Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com