Fructose Market Size, Food Sweeteners Industry Trends and Forecast to 2033

Food |

2026-03-18 12:30:51

PW Consulting today releases a strategic briefing drawn from our forthcoming High Purity L‑Glutamine Market report (base year 2025, forecast period 2026–2032). As life sciences supply chains, specialty ingredient manufacturers, and strategic investors position for a turbulent 2026, this briefing explains how the market’s trajectory should shape near‑term capital allocation, sourcing policy, and partnership decisions.

High Purity L Glutamine Market

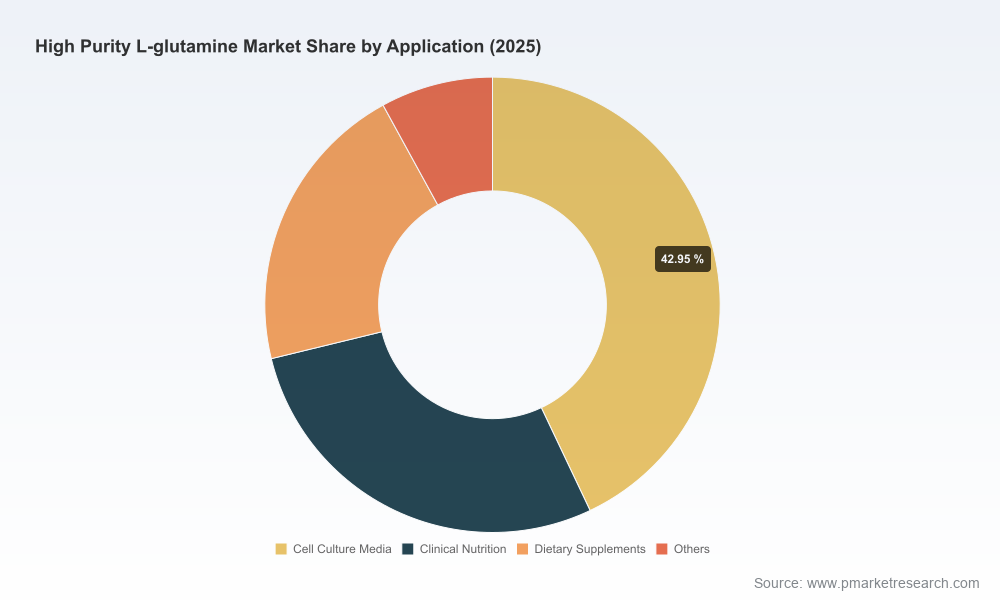

The high purity L‑glutamine market is recovering from multi‑year demand shifts and is on a structurally higher growth path. Our base‑year assessment for 2025 pegs the overall market value at USD 245.5 Million. Under our central scenario, the market is expected to expand driven by biologics manufacturing scale‑up, growth in clinical nutrition and advanced cell culture applications, and continued uptake in high‑end nutraceutical formats — yielding a compounded annual growth rate of approximately 7.91% across the 2026–2032 forecast window, bringing the market to the low‑hundreds of millions by the early 2030s.

High Purity L Glutamine Market

That trajectory converts into concrete strategic choices in 2026: whether to accelerate onshore capacity, secure multi‑year offtakes with certified suppliers, or pursue opportunistic M&A to capture incremental margin as manufacturing moves up the value chain. Our report is designed to make those choices evidence‑based and executable.

High Purity L Glutamine Market

Demand‑supply model calibrated to 2020–2025 historicals and dynamically linked to biologics capacity buildouts, clinical trial starts, and nutraceutical consumption patterns. The model produces custom scenarios for procurement teams (spot vs contract), production planners, and M&A desks.

Regulatory impact matrix mapping potential outcomes from import trade actions, tariff contingencies, and certificate‑of‑analysis (CoA)/USDMF/CEP filing timelines — translated into actionable sourcing mitigations and cost pass‑through simulations.

Supplier scorecards covering quality certifications, low‑endotoxin/low‑metal capabilities, CoA/USDMF status, geographical footprint, and capacity flexibility — built to support dual‑sourcing and contingency contracting.

Procurement playbook with three executable strategies for 2026: “Protect and Lock” (multi‑year, quality‑indexed contracts); “Hedge and Flex” (tiered spot coverage plus capacity options); and “Localize and Certify” (capex timelines for onshore parity and regulatory assurance).

M&A and alliance shortlist identifying priority targets by strategic fit (technology, certification, market access), plus preliminary valuation multipliers and integration risk checklists for rapid due diligence.

Risk heatmaps and operational contingencies addressing feedstock volatility, logistics disruptions, and certification delays — with estimated impact bands to support board‑level prioritization.

The high purity segment shows moderate concentration: the top three players account for a meaningful share of supply, and the top five significantly increase that share. This creates a market with identifiable industry leaders and a deep tail of regional and specialized producers. The competitive set includes multinational chemical and amino‑acid specialists, established pharmaceutical excipient manufacturers, and ambitious large‑scale fermentation players from Asia — each bringing differentiated value propositions.

Technology and compliance leaders (e.g., established global bioscience companies) compete on USP/EP/JP grades, USDMF/CEP filings, and demonstrated low‑endotoxin manufacturing for injectable and cell‑culture applications.

Large fermentation players with scale advantages focus on cost and global distribution, using capacity and logistics to serve nutraceutical and lower‑barrier pharmaceutical channels.

Regional specialists and cGMP excipient producers emphasize certification, customer intimacy, and rapid response for parenteral and clinical‑grade supply needs.

For decision‑makers, the implication is clear: supply strategies must be segmented by application risk (parenteral vs research vs nutraceutical), regulatory exposure, and price elasticity. Our supplier scorecards and sourcing simulations in the report give procurement leaders the ability to translate these qualitative distinctions into contractual language and KPIs.

Established global bioscience manufacturers bring deep regulatory assets (USDMF/JDMF/CEP) and proven low‑endotoxin lines suited for biologics supply chains. Their premium positioning supports higher margins in injectable and cell culture segments.

European specialty chemical players emphasize certified supply chains and high‑purity process controls; they are natural partners for pharma firms needing shorter validation windows and stable certification status.

Large Chinese fermentation groups deliver scale and cost competitiveness. Their accelerated overseas capacity programs increase supply options but also introduce trade and regulatory complexity for North American and European buyers seeking tariff‑safe sourcing.

Regional Indian and Chinese producers often provide attractive cost‑performance for generic clinical‑grade demand, while smaller GMP firms in the U.S. and Europe differentiate through rapid certification and low‑risk logistic footprints.

Feedstock and fermentation economics: Fermentation accounts for the vast majority of global L‑glutamine production, relying on agricultural feedstocks such as glucose and corn starch. A modest price decline in upstream glutamic acid observed early in 2026 is easing some short‑term input pressure, but structural demand from biologics may re‑pressure feedstock markets if downstream production ramps faster than expected.

Capacity moves: Several large producers accelerated capacity expansion during 2024–2025; these investments start to influence global balances in 2026. Buyers should expect transitional periods where spot availability increases while certified supply suitable for parenteral use remains rationed until validation cycles complete.

Regulatory and trade policy: Ongoing trade measures and a high‑profile review of pharmaceutical imports are elevating the premium for tariff‑compliant suppliers and onshore or allied‑country production. Governments are signalling differentiated treatment for some vitamins and amino acids, but the policy path remains a supply‑chain risk requiring proactive sourcing re‑engineering.

Product innovation and certification releases: New product introductions and catalogue updates from regional manufacturers continue to broaden available grades, creating opportunities for formulators but also raising buyer diligence requirements to ensure equivalence on critical purity and endotoxin metrics.

Segment sourcing by use case: Lock premium, certified suppliers for parenteral and cell culture needs; deploy flexible contracts and cost‑pass mechanisms for nutraceutical and research grades.

Build a regulatory‑aware dual‑sourcing roster: Combine established certified manufacturers with high‑quality regional producers that can scale, while maintaining rapid qualification pathways to switch supply in months not years.

Consider targeted capacity or equity plays: For mid‑sized players, selective minority investments in fermentation assets or toll‑manufacturing partnerships can secure preferential allocation without the full risk of greenfield expansion.

Operationalize feedstock hedges and logistics flexibility: Translate the report’s feedstock‑price scenarios into hedging rules and logistics alternatives to preserve margin and availability under volatility.

Boards and executive teams need not only forecasts, but executable roadmaps. Our report provides: (a) quantified scenario outcomes tied to procurement levers; (b) a regulatory response matrix that converts trade actions into procurement deadlines; (c) an M&A readiness checklist that shortens diligence time by pre‑mapping critical certification and integration risk; and (d) a supplier negotiation toolkit with contract language templates keyed to quality, supply continuity, and price pass‑through mechanisms.

PW Consulting’s full High Purity L‑Glutamine Market report contains the granular segmentation, region‑by‑region supply/demand tables, supplier benchmarking scores, and transaction‑level valuations that underpin the strategic playbook summarized here. This briefing intentionally omits detailed segment breakdowns to preserve the value of the full dataset; practitioners requiring the precise splits, forecast tables, and downloadable models should consult the full report.

For procurement directors, strategic investors, and corporate development teams preparing for 2026, the report is calibrated for immediate use: plug‑and‑play scenario models, supplier RFP templates, and an actionable M&A shortlist are included to shorten decision cycles and reduce execution risk.

To access the full report, detailed models, and supplier scorecards, please visit the PW Consulting report page or contact our industry advisory team for a tailored executive briefing. PW Consulting stands ready to workshop these findings with your procurement, regulatory, and commercial leadership to convert market intelligence into defensible, 2026‑ready plans.

For detailed analysis of this topic, please visit the official page:High Purity L Glutamine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com