Indoor Air Quality Monitoring System Market Report: Regional Analysis, Segmentation & Forecast

Art |

2026-06-24 05:40:53

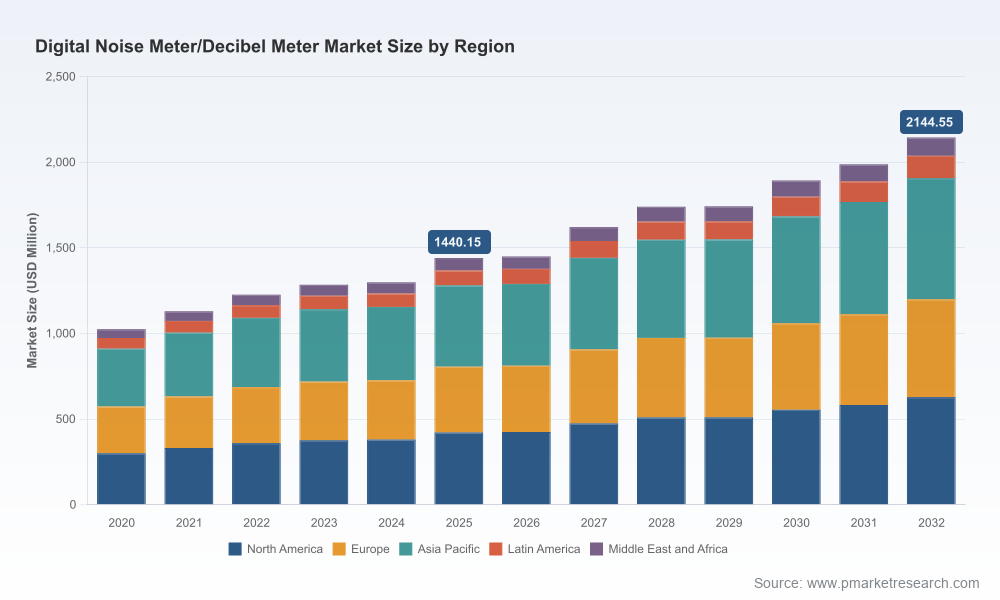

As enterprises reassess operational resilience, regulatory compliance, and workplace well‑being ahead of 2026, measurement and monitoring of acoustic environments has moved from a niche technical concern to a strategic capability. PW Consulting’s latest Digital Noise Meter Decibel Meter Market report (base year 2025, forecast 2026–2032) synthesizes seven years of market evolution and forward projections to inform procurement, product, and M&A decisions. The global market — measured in USD Million — expanded from roughly 1.02 billion in 2020 to about 1.44 billion in 2025, and is forecast to grow at a compound annual growth rate (CAGR) of 5.85% through 2032, reaching an estimated 2.14 billion by the end of the forecast period.

Digital Noise Meter Decibel Meter Market

Regulatory pressure is tightening. Updated international standards and occupational guidelines (including the 2025 iterations of ISO and IEC standards and continued OSHA enforcement) raise the bar on measurement accuracy, traceability, and worker‑exposure protocols. Organizations that delay investment in high‑fidelity monitoring risk compliance gaps and higher remediation costs.

Digital Noise Meter Decibel Meter Market

Data is now a strategic asset. Modern decibel meters are increasingly integrated into IoT stacks, enabling continuous environmental analytics rather than episodic measurement. Enterprises that pair hardware procurement with data platform strategies capture new value streams (predictive maintenance, community relations, health & safety KPIs).

Digital Noise Meter Decibel Meter Market

Market maturity presents selective opportunities. The market’s steady CAGR and historical growth establish a predictable expansion window for product upgrades, services, and software monetization — but value accrues to players that align product accuracy (Class 1 vs Class 2), connectivity, and services with customer budgets and compliance needs.

Executive synthesis and investment thesis tailored for corporate strategists, procurement leads, and private equity: concise signals on demand drivers, pricing pressure, and margin pools.

Market sizing and trend analytics: a reproducible model that traces the market from 2020 through 2025 and projects 2026–2032 under multiple demand scenarios. High‑level macro numbers are presented to support budgeting and portfolio planning.

Regulatory and standards impact assessment: focused guidance on IEC 61672 performance tiers, ISO methods for occupational exposure, and OSHA thresholds — including practical checklists for certifying measurement programs and establishing audit trails.

Technology and product map: classification of device types (precision Class 1 instruments, general Class 2 units, and integrating analyzers), connectivity layers, calibration and service models, and software‑enabled features that command pricing premiums.

Buyer’s playbook: procurement frameworks for capex vs. as‑a‑service choices, lifecycle cost calculators (including calibration frequency and data management costs), and vendor selection matrices keyed to use case and regulatory risk tolerance.

Competitive benchmarking and vendor dossiers: qualitative and quantitative scoring of incumbent vendors, go‑to‑market strategies, distribution channels, and product roadmaps — enabling shortlist creation for RFPs without exposing sensitive market share line items in this brief.

Scenario planning and deal pipeline guidance: three strategic scenarios (Consolidation, Platformization, and Fragmentation) with implications for M&A targets, integration KPIs, and partner ecosystems.

Implementation templates: pilot design, validation protocols, calibration governance, and a template SLA for third‑party monitoring providers ready for deployment in 90–180 days.

Standards and enforcement: The IEC 61672 family continues to be the benchmark for instrument performance, while ISO 9612:2025 and OSHA guidance tighten expectations for workplace exposure assessment. Buyers should prioritize instruments with clear traceability and vendor commitments to accredited calibration.

Hardware differentiation is narrowing while software becomes a margin driver: Premium Class 1 instruments retain value for compliance‑heavy customers and research applications; at the same time, IoT connectivity, automated reporting, and cloud analytics are where service providers extract recurring revenue.

Integration into industrial systems: Partnerships between metrology equipment providers and smart factory integrators are accelerating. Embedding acoustic sensors into process control and condition monitoring platforms reduces operational blind spots and creates new cross‑sell bundles.

Workplace health and corporate ESG: Employers are increasingly framing noise management as part of occupational health and broader ESG commitments. This shifts purchasing from ad hoc instruments to sustained monitoring programs with reporting capabilities aligned to sustainability disclosures.

The market brings together long‑standing precision manufacturers, cost‑focused instrument makers, and regional specialists. Each group follows distinct value propositions that inform partnership and procurement choices:

Precision legacy players (e.g., Brüel & Kjær — Nærum, Denmark; Larson Davis — Provo, Utah) emphasize Class 1 performance, metrological heritage, and analytical ecosystems for research, environmental monitoring, and advanced occupational use cases. These vendors command premium positioning where traceable accuracy and advanced feature sets matter.

Cost and accessibility leaders (e.g., Extech Instruments — Nashua, NH; REED Instruments — Wilmington, NC) serve field technicians and general occupational safety programs with affordable, rugged devices and straightforward data logging. Their strength is in broad distribution and ease of use.

Regional and systems specialists (e.g., PCE Instruments — Meschede, Germany; RION — Tokyo, Japan; Casella — Bedford, UK; Svantek — Warsaw, Poland; Pulsar Instruments — Filey, UK) combine local standards knowledge, retrofit solutions for industrial customers, and integration with hearing conservation programs.

Market movements to watch: product launches and partnerships. For example, new occupational‑focused models with built‑in dose metrics (announced in 2025) and compact pocket meters for ambient checks expand addressable use cases. Collaborations to integrate sound sensors into smart factory architectures underscore the escalating role of acoustic data in industrial IoT.

For corporate purchasers and HSE leaders (Immediate — 0–12 months): Conduct a compliance gap analysis mapped to the updated ISO/IEC/OSHA guidance; prioritize instrument purchases where regulatory risk is highest. Pilot integrated monitoring on one high‑risk site to validate data flows and calibration regimes before scaling.

For product and engineering leaders (Near term — 6–18 months): If you are a device vendor, accelerate investments in secure connectivity, over‑the‑air firmware management, and cloud analytics that yield recurring revenue. If you are a systems integrator, formalize partnerships with metrology vendors and build certified calibration workflows.

For investors and M&A teams (Medium term — 12–36 months): Target acquisitions that expand software capabilities, calibration networks, or last‑mile distribution in underserved geographies. Focus on targets with defensible service revenue or strong channel relationships rather than pure hardware plays.

For service providers (Ongoing): Differentiate on accredited calibration, rapid instrument exchange programs, and analytics‑driven advisory services that convert measurement data into operational recommendations.

Technology substitution risk is asymmetric: low‑cost MEMS sensors promise ubiquity but currently lack the repeatable traceability of Class 1 instruments. Enterprises must balance scale with metrological integrity.

Regulatory shifts and localized enforcement can create pockets of accelerated demand or sudden capital expenditure needs; global organizations should maintain a flexible procurement reserve to respond to jurisdictional changes.

Supply chain volatility for sensors and semiconductors remains a consideration for 2026 planning — contracts with clear lead times and spare‑unit strategies reduce program risk.

Our market model supplies the macroeconomic and segment‑level trajectories necessary to build capital plans and prioritize projects, while our vendor assessments offer a pragmatic shortlist for procurements and partnership diligence. The operational toolkits — including pilot templates, calibration schedules, and SLA language — are designed for rapid deployment.

Importantly, this brief intentionally omits detailed segmented shares and granular regional breakdowns: the full report contains the precise splits, competitor revenue buckets, and scenario‑based financials that senior leaders and deal teams require for final approvals. Those datasets are provided with reproducible models and confidence intervals to support board‑level decisions.

Download the full Digital Noise Meter Decibel Meter Market report for the 2026‑2032 forecast, complete vendor scorecards, and the reproducible financial model.

Engage PW Consulting for a tailored executive workshop: align your HSE, procurement, and technology roadmaps to the market outlook and build a prioritized implementation plan for 2026.

For organizations that view acoustic measurement as a compliance checkbox, the coming years will feel incremental. For those that treat sound monitoring as a data source that informs safety, operational efficiency, and community engagement, 2026 presents a window to convert measurement into strategic advantage.

For detailed analysis of this topic, please visit the official page:Digital Noise Meter Decibel Meter Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com