Understanding Risks and Safety in Hymen Surgery in Dubai

Health |

2026-06-04 10:11:55

PW Consulting today publishes its authoritative market brief on the Paid Micro Short Drama Production market, timed to support executive decision-making throughout 2026. After analyzing five years of historical performance (2020–2025) and running scenario forecasts across 2026–2032, our study identifies the structural drivers, competitive moves, and operational levers that will determine winners in the next phase of scale and monetization.

Paid Micro Short Drama Production Market

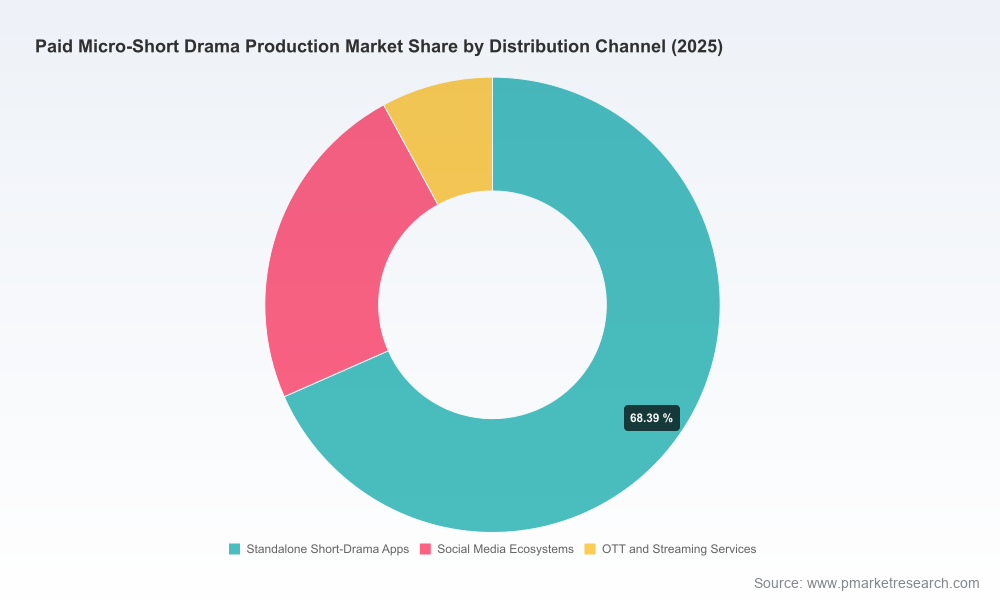

At a macro level, the market reached roughly USD 1.25 billion in 2025 and is projected to grow at a compound annual growth rate of approximately 22.45% through our 2026–2032 forecast window, producing multiple strategic inflection points for content producers, platform operators, telcos, brands, and investors. While this press summary highlights core trends and practical recommendations, the report deliberately omits granular segment tables and regional splits to encourage readers to access the full intelligence package for transaction-ready detail.

Paid Micro Short Drama Production Market

Speed-to-market matters more than ever. Short-form, vertical episodic formats compress development and distribution cycles—decision-makers must reconfigure greenlight and production pipelines to capture first-mover economics.

Paid Micro Short Drama Production Market

Monetization is multifaceted. Subscription, coin-based unlocks, in-app purchases and brand-sponsored models coexist; successful players blend monetization across formats rather than relying on a single stream.

AI is a transformative cost lever. AI-assisted production workflows are already creating new unit economics that can reshape margins and content volume strategies.

Regulation and labor frameworks are stabilizing. New labeling and union contract regimes are emerging—enterprises must bake compliance and talent economics into every 2026 plan.

Rapid revenue expansion: The market’s historical trajectory through 2025 demonstrates consistently high growth; our forecast shows sustained expansion that will reward those able to scale distribution while managing acquisition and retention costs.

Unit economics are shifting: Professional vertical microdrama series have established budget bands—most productions operate within a mid-range budget envelope, while premium S-class titles command substantially higher spend. Concurrently, AI-driven production workflows have driven per-minute production costs down materially in certain markets, enabling higher volume experiments and lower break-even thresholds.

Production cadence and infrastructure: Compact crews and 1–2 week shoots have become the norm for many vertical series. At the same time, industrial-scale AI-assisted production hubs are emerging, enabling rapid output and standardization of quality across large slates.

Regulatory and labor landscape: Authorities in several major markets now require AI-origin labeling and have refined review processes for new-media formats. Industry guilds have negotiated new contracts tailored to microdrama budgets—this dual dynamic creates a compliance floor that firms must institutionalize.

Market structure: The market is neither a pure winner-takes-all platform nor completely fragmented. Leading clusters of producers and platforms capture a meaningful share of revenue, leaving room for scale mergers and differentiated niche plays.

Our report profiles the firms shaping the market today and those whose recent moves point to scalable models for 2026. Below are the core competitors we tracked and the strategic takeaways executives should consider.

Crazy Maple Studio (ReelShort) — A California-headquartered studio backed by a major Chinese investor, operating a paid micro-drama app focused on vertical episodic content and hybrid monetization (coin-based unlocks plus subscriptions). Strategic takeaway: owning the consumer monetization layer remains a potent advantage—platform-control enables rapid A/B testing on pricing and episode gating.

Beijing Dianzhong Technology (DramaBox) — A China-based producer and operator with strong overseas traction, notable for translated and localized vertical series monetized via in-app purchases. Strategic takeaway: localization and distribution partnerships are decisive when converting regional virality into sustained paid revenue.

Linmon Media — Expanding into vertical microdramas for Asian markets with high-performing regional launches. Strategic takeaway: regional content excellence plus festival and market presence (slate launches) accelerate licensing and telco partnership traction.

AR Asia Productions — Focused on multi-genre microdrama distribution across Asia with telco and platform partnerships. Strategic takeaway: bundling microdramas into telco propositions and regional OTT offerings can materially reduce CAC and increase ARPU through cross-sell.

Vigloo (SpoonLabs) — A Seoul-based studio producing premium and AI-assisted microdramas, including fully AI-native English-language titles. Strategic takeaway: AI-native productions lower marginal costs and accelerate iteration; however, reputation management and disclosure rules require careful governance.

Holywater (MyDrama/MyMuse) — Producing Hollywood-style microdramas for international paid platforms with strategic investor backing. Strategic takeaway: premiumized micro-form content can command higher price points and reach new audience demographics when paired with sophisticated marketing.

Recent industry events underscore these dynamics: slate launches and market movement from regional producers, fully AI-native program releases executed in compressed timeframes, and the scale-up of AI-assisted production hubs serving thousands of teams. Each development points to a market accelerating both in volume and in technical sophistication.

Rewire production processes for hybrid AI-human workflows. Adopt AI tools for pre-production, VFX, and editing to lower per-minute costs and shorten lead times. Pilot fully AI-assisted titles alongside human-first productions to measure quality delta and audience tolerance.

Modularize IP and monetization. Design stories as modular vertical episodes that can be re-bundled across pay-per-episode, subscription, and brand sponsorship packages—this flexibility smooths revenue volatility and lengthens content lifetime value.

Forge distribution partnerships beyond pure-play apps. Negotiate telco bundling, integrated social ecosystem placements, and windowed OTT licensing to broaden reach while preserving core paid conversion flows.

Institutionalize compliance and talent frameworks. Embed AI labeling, content review processes, and updated guild contract templates into production playbooks to avoid costly retrofits and labor disputes.

Measure unit economics at the episode level. Track acquisition cost, retention cohorts, ARPU by monetization channel, and content-level payback periods. Use these KPIs to allocate slate spend dynamically toward the highest-yielding formats and geographies.

Investors and corporate development teams should prioritize three themes this year:

Production automation and tooling. Platforms and studios that own or tightly integrate with AI tooling stacks will capture improved margins and expand feasible slate volumes.

Distribution control and direct monetization. Companies that combine platform access with proven paid conversion pathways enjoy strategic optionality versus pure content suppliers.

Regional champions and localization capabilities. Firms with demonstrated localization playbooks and local partnerships can export formats at scale and sustain lifetime monetization across markets.

Market concentration metrics indicate meaningful leadership pockets but also room for consolidation—top clusters account for a significant portion of revenue while nearly half of market value remains distributed across a long tail of regional players. This structure favors strategic bolt-ons for scale and capability expansion.

The full report delivers the tactical intelligence executives need to translate insight into action. Highlights include:

Scenario-based revenue forecasts (base, upside, downside) and sensitivity analyses that drive capital allocation decisions.

Episode-level production cost benchmarks and modular budget templates to accelerate greenlight cycles.

Monetization playbooks with tested pricing experiments, churn-reduction tactics, and bundled sponsorship frameworks.

Vendor and tooling scorecards for AI production platforms, post-production vendors, and distribution partners.

Legal and regulatory compendium covering AI disclosure, platform compliance, and new guild provisions for microdrama talent.

Competitive due diligence briefings and go-to-market blueprints for direct-entry and partnership-led expansion.

To preserve strategic advantage for paying clients, the report’s annexes include granular regional and format splits, contract clause templates, and downloadable model spreadsheets—these are intentionally excluded from this press summary to serve as paywalled deliverables.

Rapid diagnostics: 4–6 week market-entry and slate-optimization engagements to rebase production and monetization KPIs.

Operational playbooks: bespoke production and distribution blueprints, vendor negotiation support, and compliance checklists for AI labeling and union contracts.

M&A and partnership advisory: target screening across production tooling, distribution platforms, and regional studios to accelerate consolidation or fill capability gaps.

Conclusion: 2026 will be a defining year for the paid micro short drama market. Growth remains robust at the top line and unit economics are being rewritten by AI and new distribution models. Organizations that proactively redesign production pipelines, diversify monetization, and institutionalize compliance and talent strategies will convert market momentum into durable advantage. PW Consulting’s full report provides the operational blueprints and transaction-ready intelligence to make those shifts quickly and with confidence.

For access to the complete dataset, segmented forecasts, downloadable models, and proprietary annexes, please visit PW Consulting’s report page. Our team is also available to discuss tailored advisory programs to accelerate your 2026 agenda.

For detailed analysis of this topic, please visit the official page:Paid Micro Short Drama Production Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com