Water Utility Monitoring System Market: Strategic Imperatives for 2026 — PW Consulting Report Preview

PW Consulting today releases a strategic preview of our forthcoming Water Utility Monitoring System Market report — an essential briefing for utility executives, technology investors, and infrastructure planners preparing decisions in 2026. Grounded in a robust historical base (2020–2025) and a clear, data-driven forecast (2026–2032), this preview summarizes why the monitoring systems segment is a priority investment area, what practical tools the full report provides, and how leading vendors are positioning to capture value as the market accelerates.

Water Utility Monitoring System Market

Market Trajectory and What It Means for 2026 Decisions

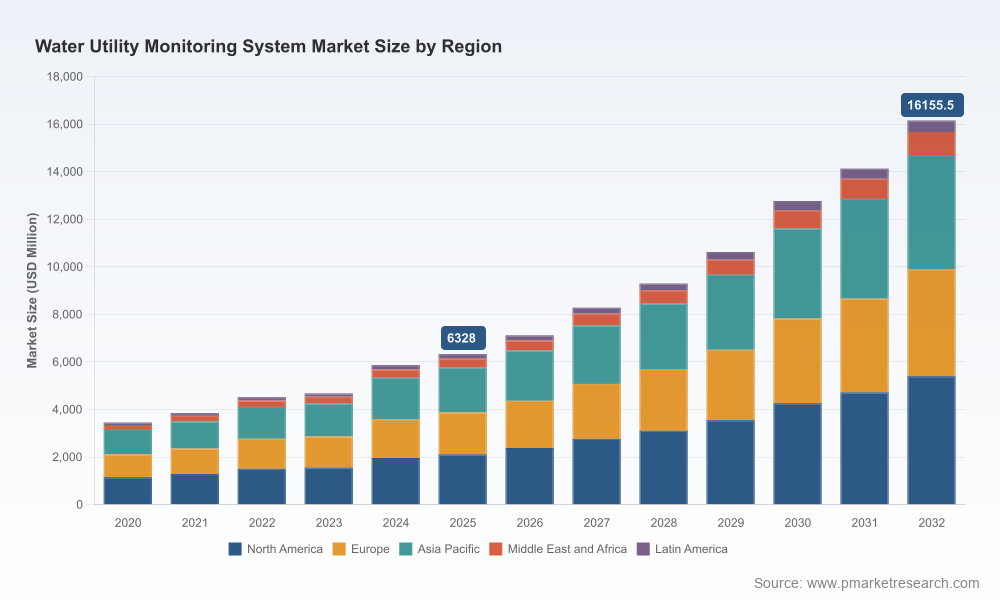

The water utility monitoring market has moved from a niche digital program to a core element of network resilience and commercial performance. Our base-year assessment places global market revenue at USD 6,328.0 Million in 2025, following sustained expansion from 2020. With a compound annual growth rate (CAGR) of 14.33% forecast over 2026–2032, the market is set to cross significant scale thresholds within the investment horizon most utility planning cycles now target. By 2032 the market is projected to be multiple times larger than the 2025 base, reflecting faster-than-average adoption of smart metering, telemetry, analytics and enterprise-level monitoring capabilities.

Water Utility Monitoring System Market

For 2026, that trajectory translates into three practical implications for decision-makers:

Water Utility Monitoring System Market

- Acceleration pressure: Capital and operating dollars will be redirected toward digital monitoring to meet regulatory, environmental, and commercial imperatives.

- Vendor selection matters: A moderate concentration among leading suppliers creates both opportunities for strategic partnerships and risks of lock-in that must be managed.

- Risk profile shifts: Digital deployments reduce manual labor costs but increase exposure to cybersecurity, data governance and lifecycle software investments.

Sector Dynamics Shaping the Short-Term Playbook

Several persistent forces are shaping the near-term market environment and should factor into any 2026 planning scenario:

- Regulatory classification and cybersecurity: Water utility control systems — including SCADA and smart metering networks — are increasingly treated as critical infrastructure under national guidance. Expect requirements around network segmentation, encrypted communications, and continuous monitoring to be prerequisites for funding and project approval.

- Capital needs and asset deterioration: In mature markets, regulators and industry studies signal multi-hundred-billion-dollar investment backlogs to replace aging drinking water and wastewater assets. This creates a long-term procurement pipeline for monitoring systems integrated with asset replacement programs.

- Operational economics: Utilities are documenting labor savings from automated meter reading and remote diagnostics, but are simultaneously reallocating spend toward cybersecurity operations, cloud services, and analytics subscriptions — shifting total cost of ownership drivers.

- Spectrum and policy constraints: In several emerging markets, telecommunications and spectrum governance materially affect choice of radio technologies and deployment pace for IoT devices.

What the PW Consulting Report Contains — Practical, Ready-to-Use Deliverables

The full PW Consulting market research package is built for operators and investors who must convert market intelligence into procurement and investment action. Key deliverables include:

- Methodology and market sizing: Full documentation of assumptions, base-year calibration, and scenario-driven forecasts across the 2026–2032 horizon to stress-test investment cases.

- Decision support templates: Total cost of ownership (TCO) models, KPI dashboards for pilots, selection scorecards for hardware/software/service mixes, and procurement RFP checklists tuned to cybersecurity and interoperability clauses.

- Implementation playbooks: Stepwise deployment templates for smart metering, telemetry, and digital twins, including pilot-to-scale transition criteria and vendor engagement timelines.

- Investment and M&A framework: Prioritization matrix for inorganic growth, partnership models, and valuation sensitivities for strategic investors evaluating utility-tech assets.

- Vendor benchmarking and deal tracker: Comparative analysis of competitive positioning, product strengths, go-to-market models, and a chronology of major commercial moves to inform negotiation strategies.

To preserve commercial value for report subscribers, the preview intentionally omits granular regional and application split figures and detailed price-model tables. These segment-level breakouts — including breakouts by component, technology and geography — are available in the full report on our site.

Strategic Takeaways: Five Actions to Prioritize in 2026

- Adopt a cybersecurity-first procurement standard: Embed encrypted communications, device identity management and continuous monitoring clauses into all new AMI/SCADA procurements. Regulatory guidance increasingly links these controls to grant eligibility.

- Structure pilots to validate operating-model transitions: Pilot projects should measure not only leak-reduction or meter-read accuracy, but also the incremental costs of cloud ingestion, analytics subscriptions, and permanent SOC functions.

- Favor modular architectures that de-risk vendor lock-in: Specify open APIs, standards-aligned data models, and staged integration to allow best-of-breed selection across hardware, communications and analytics layers.

- Plan capital and O&M as a blended financial case: Recast budgets to compare capex for hardware and installation against multi-year opex for connectivity, analytics and cybersecurity — this is where many utilities realize unplanned lifecycle costs.

- Use competitive dynamics to negotiate value beyond price: With the market showing moderate concentration among leading providers, leverage defined pilots, shared-savings models and multi-utility consortium procurements to extract favorable licensing and service terms.

Competitive Landscape — Who to Watch and Why

The market’s leading manufacturers and systems integrators remain the first movers in product innovation, partnerships and strategic acquisitions. Our analysis highlights companies that combine meter hardware, communications platforms, analytics capabilities and field service footprints — elements that create stickiness in utility relationships. Representative vendors include global metering and instrumentation leaders, systems integrators with SCADA and automation expertise, and specialist analytics firms focused on leak detection and digital twins.

- Badger Meter, Inc. — Known for smart metering and flow measurement, with recent moves broadening sensing into wastewater monitoring through targeted acquisitions to extend solution sets for utilities.

- Itron, Inc. — A platform and communications incumbent deploying AMI modernization projects and expanding communications modules and telemetry platforms into new geographies to capture growth in smart metering conversions.

- Sensus (Xylem) and Xylem Inc. — Offering combined metering, sensors and digital platform capabilities that target utility network optimization and water quality monitoring across the asset lifecycle.

- Neptune Technology Group and Kamstrup — Companies focused on advanced meter hardware and AMI suites that appeal to utilities prioritizing metrology accuracy and low-maintenance field devices.

- ABB, Siemens, Schneider Electric — Industrial automation leaders providing SCADA, process instrumentation and cybersecurity-hardened architectures for treatment and distribution networks.

- Hach (Danaher) and other specialty sensor suppliers — Supplying water quality instrumentation that integrates into monitoring platforms where compliance and process control are central.

Recent commercial activity reinforces the fast-evolving vendor strategies: strategic partnerships to deploy regional AMI projects, geographic expansion of communications modules, targeted acquisitions to broaden sensing portfolios, and new product launches that emphasize cybersecurity and AI-driven prediction. These moves foreshadow an environment where product breadth, platform maturity, and service delivery will determine market winners.

Market concentration metrics indicate a moderate degree of supplier consolidation among the top vendors. Buyers should interpret this as an impetus to insist on interoperable contracts and robust exit/transition clauses should future competitive dynamics shift.

How Utilities, Vendors and Investors Should Use This Preview

This preview is designed to inform immediate 2026 planning cycles. Recommended next steps:

- Utilities: Use the report’s procurement templates and TCO models to re-baseline 2026 capital programs and to build defensible multi-year budgets that incorporate cybersecurity and SaaS costs.

- Vendors: Map product roadmaps against the report’s technology adoption scenarios to prioritize interoperability and compliance features that are likely to become procurement must-haves.

- Investors and financiers: Leverage our growth scenarios and M&A framework to size platform plays, service provider roll-ups, and strategically positioned hardware manufacturers.

Conclusion — Why PW Consulting’s Intelligence Matters for 2026

As the water utility monitoring market shifts from pilot-driven experimentation to enterprise-grade deployments, the decisions made in 2026 will set long-term cost and resilience trajectories for utilities and the commercial fortunes of suppliers. PW Consulting’s report combines quantified market sizing, a verified growth path, tactical tools, and competitive intelligence to support executable strategies. For executives who must align capital discipline with digital ambition, the full report delivers the depth required to move beyond vendor claims and toward measurable outcomes.

To access the complete dataset, segmented analyses and proprietary templates referenced in this preview, please visit our report landing page. PW Consulting’s full Water Utility Monitoring System Market report contains the granular regional, technology and application splits that underpin the scenarios summarized here.

For detailed analysis of this topic, please visit the official page:Water Utility Monitoring System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com