Stem Cell Treatments for Lupus: Exploring Regenerative Medicine for Autoimmune Care

Other |

2026-05-28 16:40:31

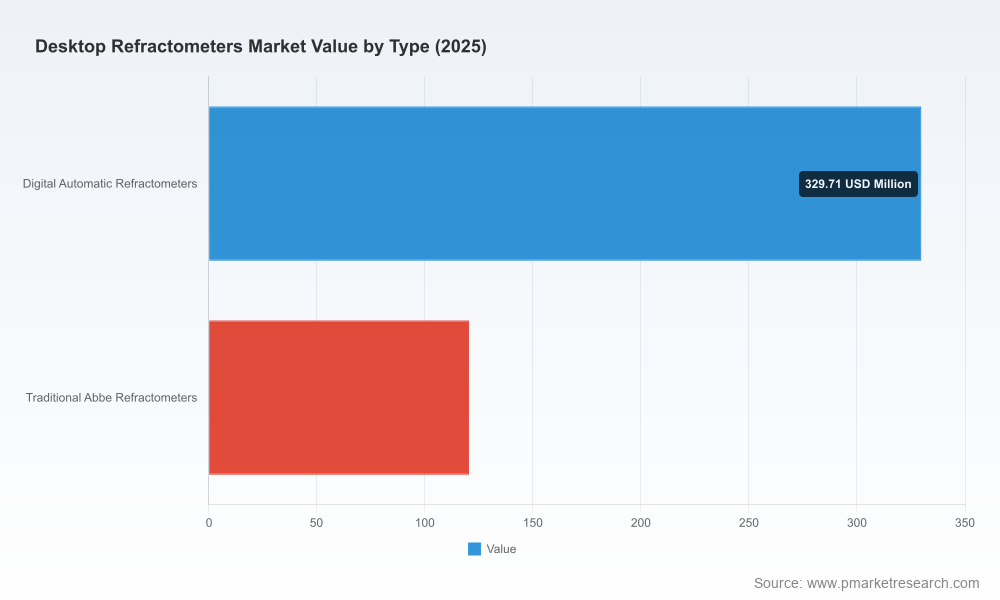

PW Consulting today publishes a forward-looking analysis of the Desktop Refractometers market, designed to equip executive teams with the strategic clarity they need as they set budgets, product roadmaps, and M&A priorities for 2026. Built on a 2025 base-year audit and a 2026–2032 forecast horizon, our study combines rigorous market sizing, competitive intelligence, and decision-grade scenario work to translate instrument-level dynamics into actionable corporate choices. Key headline metrics: the market has expanded from 2020 levels to an audited 2025 market size of USD 450.15 Million and is projected to grow at a compound annual growth rate (CAGR) of 5.18% across the 2026–2032 forecast window, approaching the mid-hundreds of millions by the end of the period.

Desktop Refractometers Market

Between 2020 and 2025 the sector demonstrated steady expansion, reflecting resilient demand across clinical laboratories, food & beverage quality control, and pharma/biotech quality assurance. Our forecast assumes continuation of this healthy baseline demand, tempered by short-cycle volatility driven by purchasing budgets and capital replacement patterns. The 5.18% CAGR we model accounts for two structural influences: a continued shift toward digital/automated desktop instruments and a persistent installed-base replacement tail where legacy Abbe-style devices are gradually refreshed for higher throughput, automation and connectivity.

Desktop Refractometers Market

Importantly, growth is not uniform: equipment sophistication, regulatory posture of buyers, and procurement cycles create pockets of accelerated adoption (multi-wavelength and temperature-controlled units) as well as slower-moving segments (entry-level analog devices). PW Consulting’s report preserves the granularity clients need—pricing ladders, ASP trajectories, and device-level demand curves—while maintaining a high-level narrative suitable for board briefing and cross-functional alignment.

Desktop Refractometers Market

The competitive environment is moderately concentrated. Leading specialist manufacturers and established laboratory-analytics firms continue to drive innovation and set technical performance benchmarks. Market concentration metrics indicate a top-three/top-five grouping that controls a meaningful portion of value, leaving room for regional specialists and well-capitalized challengers to secure niche positions.

Our competitive profiles go beyond standard company summaries: subscribers receive differentiated competitor matrices mapping product roadmaps, regulatory approvals, distribution strength, service footprint and likely near-term moves (pricing and feature upgrades). Recent vendor activity—new product introductions, certifications, and trade show reveals—underscores a market driven by incremental innovation rather than disruptive entrants. That dynamic favors incumbents but creates clear windows for targeted differentiation.

Two practical supply considerations will influence 2026 vendor strategies. First, the optical core—sapphire prisms—remains a high-cost component in medical-grade refractometers; industry inputs put per-prism costs in the range of USD 500–2,000 depending on specification and treatment. Second, test automation and digitalization require electronics and sensor sourcing that are subject to lead-time variability. PW Consulting’s cost-modeling annex quantifies the margin sensitivity to raw material and component price movements and recommends hedging and supplier diversification tactics for OEMs and contract manufacturers.

PW Consulting’s Desktop Refractometers Market report is designed for executives who need both the strategic narrative and the spreadsheets. Deliverables include:

For commercial leaders, the immediate priorities are: (1) finalize 2026 capital spend and inventory buffering strategies informed by the forecasted CAGR and short-cycle variability; (2) lock in supplier agreements for optical components where lead times and price volatility could erode margins; (3) pilot clinical-feature bundles with two or three reference customers to accelerate adoption and create case studies for reimbursement-led procurement.

For product teams and R&D investors, the checklist is: concentrate development resources on connectivity, automated temperature control, and simplified compliance validation; rework pricing models to reflect value over time (service, calibration, consumables); and consider acquisitions that accelerate multi-wavelength or high-precision capabilities without long, organic development cycles.

PW Consulting’s Desktop Refractometers Market report is a practical briefing, not an academic exercise. It is purpose-built to influence 2026 decisions across procurement, product strategy, and corporate development. The public summary above intentionally omits core microsegmentation tables and device-level revenues to preserve the consultative value of the full dataset. Clients and subscribers receive the complete data tables, vendor scorecards, and downloadable financial models needed to implement the strategies described.

Contact PW Consulting for an executive briefing and to learn how the complete report can be tailored to your organization’s questions about product portfolio choices, channel investments, or M&A screening in 2026.

For detailed analysis of this topic, please visit the official page:Desktop Refractometers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com