Growing Need for Reliable Network Connectivity Drives Market Growth at 6.69% CAGR

Other |

2026-06-11 07:49:48

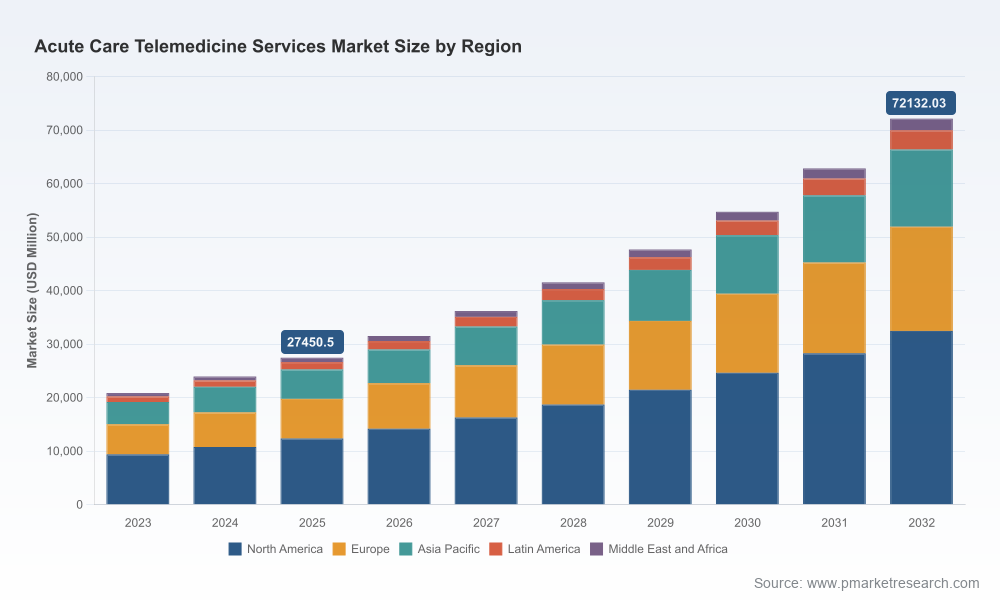

As health systems, payers, and technology vendors plan investments for 2026, PW Consulting’s latest Acute Care Telemedicine Services Market study delivers the actionable intelligence required to convert momentum into durable advantage. Built on a 2025 base year and a historical lens covering 2020–2025, the report quantifies a market on a steep growth trajectory — expanding from the low‑tens of billions in 2023 to a projected global market measured in the tens of billions by the end of our 2026–2032 forecast — and growing at a compound annual growth rate (CAGR) of 14.82% through 2032. That trajectory, combined with a moderately concentrated supplier landscape (top‑3 firms control roughly 38% of market revenue while the top‑5 capture just over 52%), creates both opportunity and strategic urgency for executives making 2026 allocation decisions.

Acute Care Telemedicine Services Market

Strategic timing: 2026 is a pivot year. With the market expected to accelerate materially year‑over‑year from the 2025 base, decisions made now about platform architecture, partner selection, and go‑to‑market (GTM) models will determine which organizations capture the next wave of scale economics.

Acute Care Telemedicine Services Market

Risk management: Rapid growth is accompanied by regulatory, reimbursement, and workforce volatility. Our study synthesizes these dynamics into scenario maps that enable risk‑adjusted investment planning rather than binary “build vs. buy” choices.

Acute Care Telemedicine Services Market

Value capture: The report provides operational playbooks — from clinical workflow integration to hybrid staffing strategies — that translate top‑line market expansion into measurable margin improvement and clinical throughput gains.

The acute care telemedicine market demonstrated strong expansion through 2023–2025 and is expected to continue expanding in 2026 and beyond, reflecting persistent demand for remote specialty coverage, ICU and emergency augmentation, and hospitalist support. The 14.82% CAGR underpinning our forecast reflects system‑level drivers — bed‑level optimization, rural access imperatives, and increasing acceptance of virtual acute care pathways — that will sustain growth across geographies and delivery architectures.

Importantly, market concentration metrics indicate that scale matters: the top three vendors account for roughly 38% of revenue while the top five exceed a 50% share. For buyers and entrants alike, this implies a market where national incumbents and well‑capitalized regional networks capture meaningful share, but where differentiated service models and integration capabilities can still create pockets of outsized return.

Reimbursement levers and uncertainty: Historically supportive policies — including parity reimbursement for certain acute telemedicine modalities under Medicare Part B — have materially de‑risked adoption. However, many of these provisions are time‑bound or subject to policy review, making conservative financial models and policy‑contingent scenarios essential inputs for 2026 capital plans.

Licensure and cross‑state practice: Interstate delivery of acute telemedicine remains administratively complex. Organizations that adopt streamlined licensure strategies — whether via the Interstate Medical Licensure Compact or centralized credentialing hubs — will gain a meaningful speed advantage when scaling multi‑state services.

Clinical standards and technology thresholds: Adherence to documented standards for video quality, bandwidth, and clinical workflows (as per professional associations) is now table stakes. Our report provides a technical checklist that maps clinical use cases to minimum infrastructure and monitoring requirements to ensure diagnostic fidelity and medicolegal protection.

Labor market pressures: Specialist shortages — especially for intensivists, neurologists, and geriatric psychiatrists — have driven staffing costs materially higher. Our analysis shows selective wage inflation in the 15–20% range in constrained rural markets, and we model staffing scenarios that reveal where telemedicine shifts FTE demand versus cost per encounter.

Quality and accreditation: Accreditation requirements for acute telehealth programs (e.g., The Joint Commission standards) impose compliance thresholds that affect time‑to‑value. Programs that bake in accreditation planning see faster payer engagement and lower denials.

The competitive field combines legacy telehealth platforms, healthcare system‑owned networks, and focused acute care specialists. Our report profiles incumbents and challengers, assessing capabilities across clinical breadth, scale of network operations, platform interoperability, and partnership ecosystems.

Access TeleCare (Dallas, TX): Now positioned after rebranding to emphasize multi‑specialty acute capabilities, the provider operates 24/7 services across neurology, psychiatry, critical care, hospital medicine, and ED support. Their strength is clinical depth and around‑the‑clock operational maturity which appeals to mid‑sized systems seeking turnkey coverage.

Eagle Telemedicine (Leawood, KS): Focused on hospitalist and intensivist services for rural and critical access hospitals, Eagle’s recent geographic expansion underscores the persistent demand among smaller hospitals for outsourced acute physician coverage. Their GTM advantage is a tight operational fit for resource‑constrained hospitals.

Avera eCare (Sioux Falls, SD): A large-scale network operator that blends ICU command center oversight with emergency department support and inpatient coordination. Recent strategic partnerships to enhance rural ED coverage illustrate a hybrid model that pairs regional system governance with local delivery — a playbook increasingly emulated by integrated delivery networks.

Teladoc Health (Purchase, NY): With the InTouch Health platform, Teladoc brings enterprise‑grade integrations for tele‑stroke, tele‑ICU, and ED physician support, leveraging platform scale and cross‑product synergies. Their position favors broad enterprise contracts and platform license models.

Amwell (Boston, MA): The Converge platform targets hospital‑centric virtual care, enabling urgent consults and hybrid care models. Amwell’s focus is on interoperability and fast deployment for hospital partners pursuing integrated virtual/in‑person care pathways.

Sound Physicians (Tacoma, WA): Combines tele‑hospitalist and tele‑ICU capabilities within comprehensive acute care management offerings, often integrated into sponsor health systems’ clinical operations. Their model emphasizes clinical governance and white‑glove provider management.

Recent vendor activity underscores market dynamics: rebranding and capability expansions among specialized firms, strategic partnerships between network operators and regional systems, and continuous geographic scaling by niche players. These moves collectively raise buyer expectations around integration, SLA transparency, and outcome‑based contracting.

Decision frameworks to evaluate build vs. buy vs. partner pathways, incorporating capital expense, time‑to‑service, and clinical control tradeoffs.

Templates and scorecards for vendor selection — technology, clinical quality, operations, and contracting — that let procurement teams move from vendor presentations to shortlists in weeks, not months.

ROI and sensitivity models calibrated to the 2025 base year and scalable across hospital sizes; financial scenarios include conservative policy reversals, licensure friction, and staffing inflation assumptions.

Operational playbooks: center design (hub vs. distributed models), staffing rosters, escalation pathways, and accreditation checklists mapped to common acute use cases.

Risk and compliance compendium covering reimbursement contingencies, licensure pathways, minimum technical standards, and data governance templates for multi‑state operations.

Competitive benchmarking and profiles with go‑to‑market tactics and partner maps to identify white space and consolidation targets.

Adopt a phased scaling approach: pilot a highest‑value acute use case, validate integration with existing EHRs and transfer workflows, then scale horizontally. Lock in clinical KPIs early to avoid scope creep.

Negotiate contract mechanisms that tie a portion of fees to clinical and throughput outcomes rather than encounter counts — this aligns incentives and mitigates reimbursement risk.

Invest in licensure and credentialing automation now. The small up‑front cost delivers outsized acceleration when expanding across state lines in 2026 and beyond.

Prioritize vendors with robust accreditation support and clear clinical governance models; accreditation readiness correlates with faster payer conversations and reduced audit risk.

Prepare for workforce‑cost volatility by modeling mixed staffing strategies (local hires, locum networks, remote specialists) and by investing in retention programs for virtual clinicians.

Boards and investment committees need concise evidence that telemedicine investments will protect margin and improve access without creating operational liabilities. PW Consulting’s study provides executive slide packs, board‑ready summaries, and scenario appendices that align financial projections to operational milestones. Use these deliverables to set three‑year KPIs, define go/no‑go decision gates, and establish contract clauses that preserve upside while sharing downside risk.

This release outlines the macroscopic market trajectory, supplier dynamics, and the practical levers executives must pull to win in 2026. In keeping with the “trailer” principle, we have intentionally presented high‑confidence strategic signals and withheld granular segmentation tables and proprietary revenue splits so readers must consult the full report for play‑by‑play market maps, regional and service‑line breakdowns, and vendor scorecards with weighted scoring matrices.

For executives preparing 2026 investment plans, the full PW Consulting Acute Care Telemedicine Services Market report provides the detailed models, contract templates, and operational checklists to move from strategy to execution with confidence. Contact PW Consulting to access the complete study, the dataset behind our forecasts, and bespoke advisory engagements that tailor these insights to your organization’s risk tolerance and growth ambitions.

For detailed analysis of this topic, please visit the official page:Acute Care Telemedicine Services Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com