L'Excellence du Divertissement Numérique : Une Immersion Sans Frontières

Games |

2026-05-09 12:48:16

PW Consulting today publishes an executive market brief accompanying our full report on the Precision Agriculture GNSS Guidance System Market. As the sector shifts from pilot deployments toward scaled operational adoption, the intelligence contained in our 2026-facing analysis is designed to convert uncertainty into strategy — enabling OEMs, retrofit suppliers, ag-service providers, investors, and public policymakers to make decisions with measurable upside and controlled risk.

Precision Agriculture Gnss Guidance System Market

Timing: 2026 is a hinge year. Technology maturity, policy incentives and supply‑chain stressors converge to make near-term choices decisive for next‑decade positioning. Our report translates those convergences into discrete strategic options.

Precision Agriculture Gnss Guidance System Market

Decision focus: Executives need rigorous, actionable insight — not descriptive summaries. PW Consulting’s analysis supplies business cases, scenario playbooks, and stress-tested roadmaps so teams can prioritize capex, partnerships, product roadmaps, and go‑to‑market tactics for measurable ROI.

Precision Agriculture Gnss Guidance System Market

Competitive clarity: The market is moderately concentrated (CR3 ~52.3%, CR5 ~68.7%). That concentration shapes where scale matters, where niche specialization can thrive, and how channel strategies should be constructed. Our brief highlights implications without disclosing proprietary segment tables reserved for the full report.

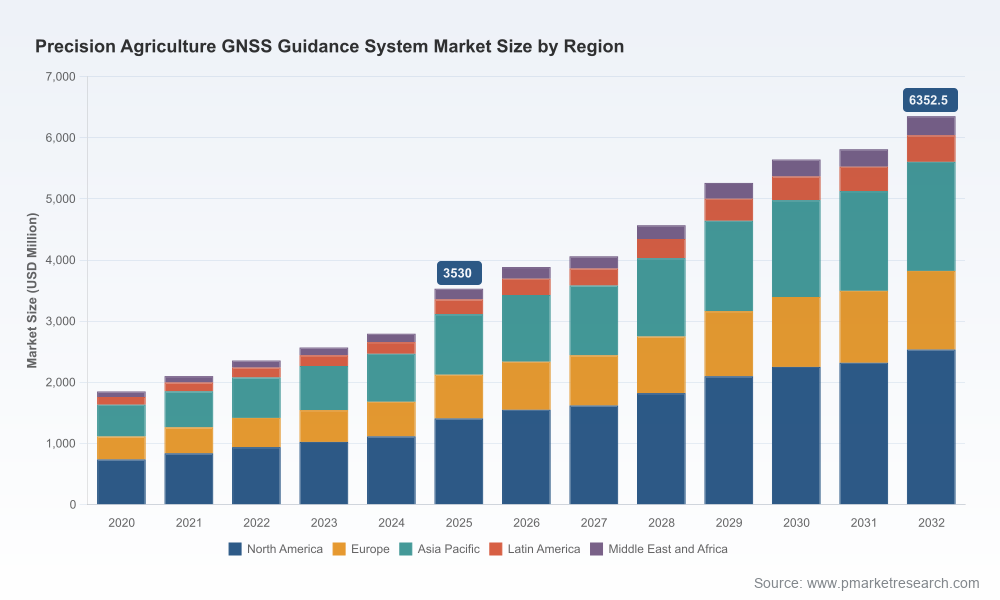

The Precision Agriculture GNSS Guidance System Market has entered a phase of sustained expansion. PW Consulting’s base‑year analysis, covering historical performance (2020–2025) and a forecast window (2026–2032), shows the industry growing from USD 1,850.45 Million in 2020 to USD 3,530.0 Million in 2025. We forecast continued expansion to USD 6,352.5 Million by 2032, representing a compound annual growth rate (CAGR) of 8.75% over the 2026–2032 horizon. For 2026 specifically, we expect the market to continue its positive momentum as early adopters transition into mainstream buyers and as reimbursement and regulatory drivers accelerate adoption.

Policy incentives and reimbursement: New provisions in the 2026 US Farm Bill — including high‑value reimbursement programs for precision technologies — materially lower the adoption cost for farmers, improving payback profiles and expanding the addressable base for guidance systems.

Operational ROI maturity: Advances in integration between GNSS guidance, autonomous implements, and farm management platforms have improved first‑year and lifecycle economics versus prior generations, shortening purchase decision cycles for many mid‑sized farms.

Technical resilience: Innovations that harden GNSS performance against ionospheric and space‑weather disturbances are emerging. These technologies materially reduce perceived operational risk during critical seasons and bolster product value propositions.

Retrofit opportunity: Mixed fleets and aging capital stock create a substantial retrofit market. Vendors that offer high‑compatibility, low‑friction retrofit solutions can access installation and data‑services revenue streams beyond OEM channels.

Regulatory transitions: The 2026 GPS datum modernization and parallel augmentation initiatives (e.g., EGNOS in Europe) require engineering roadmaps for continuity of mapping and guidance accuracy. Systems that are not prepared face remediation costs and customer dissatisfaction.

Supply chain and input costs: Tariff regimes and raw‑material dynamics — including steel tariffs affecting component prices — introduce margin pressure and product lead‑time risk for hardware‑heavy suppliers.

Market leadership combines ecosystem control, sensor fusion capability, and channel breadth. The companies we profile in the full report illustrate three enduring strategic archetypes that buyers and investors must weigh:

Integrated OEM ecosystems: Firms that embed guidance within their machinery platform offer a seamless experience, higher switching costs, and strong aftermarket capture. These players leverage proprietary receivers and platform‑level telematics to sell lifecycle services.

Platform and network specialists: Vendors focusing on universal compatibility and robust correction services enable mixed‑fleet customers to standardize on guidance performance across heterogeneous equipment. Their differentiator is cross‑brand operability and service reliability under disturbed GNSS conditions.

Retrofit and specialist vendors: Companies that optimize for simplicity of installation, low capex and modular upgrades target the retrofit segment and value‑conscious growers. Their potential lies in scaling installation channels and recurring subscription services.

Representative company insights (selective):

John Deere: Continues to deepen integration between machine control, StarFire receivers, and software-defined workflows. The value proposition is high reliability within an owned machinery and service ecosystem.

PTx Trimble: Emphasizes universal compatibility, correction robustness (including newly introduced ionospheric resilience technology), and retrofit solutions showcased against industry audiences. These moves strengthen their cross‑fleet appeal.

CHC Navigation: Positions high‑accuracy tractor guidance for retrofit markets and challenging geographies, using PPP services to deliver cm‑level performance where conventional RTK infrastructure is limited.

Hexagon (NovAtel/HxGN AgrOn): Targets OEM partnerships with premium receiver hardware and correction services, appealing to manufacturers seeking tight integration and differentiation at vehicle level.

Topcon: Pursues mixed strategies — hardware, corrections, and recent strategic partnerships that integrate vision and autonomy — signaling a hybrid path between guidance and higher autonomy layers.

These vendor strategies map directly to opportunity windows in 2026: integrated OEMs should prioritize service monetization; platform specialists should secure correction and data‑service contracts; retrofit players must scale installation networks and subscription models.

Technology resilience: The roll‑out of ionospheric disturbance mitigation solutions (announced by a major platform vendor in early 2025) reduces seasonally driven downtime risk and makes RTK/PPP solutions more reliable for commercial operations.

Autonomy and sensor fusion: Industry demos and partnerships combining vision‑based autonomy with GNSS (notably a recent alliance between a positioning vendor and a robotics specialist) indicate the next wave of farm automation will be multi‑sensor rather than GNSS‑only.

Market positioning: Leading retrofit providers continue to emphasize PPP and low‑infrastructure correction options to capture growth in regions with sparse RTK networks.

PW Consulting’s full report is constructed to be immediately operational for strategy teams. Highlights include:

Commercial playbooks: Route‑to‑market tactics for OEMs, retrofit specialists, and ISOs with prioritized channel investments and partner archetypes.

ROI and TCO calculators: Configurable models that translate guidance performance, reimbursement levels, and labour savings into payback timelines for defined farm archetypes.

Vendor scorecards: Comparative analysis of capabilities, integration complexity, service economics, and strategic fit for partnership or M&A consideration.

Regulatory impact matrix: Actionable checklists for GPS datum migration, augmentation dependencies, and regional compliance — designed to minimize product disruptions in 2026.

Supply‑chain stress tests: Scenario-based assessments of tariff and component‑price shocks with recommended mitigation levers (localized sourcing, modular design choices, hedging windows).

Customer segmentation playbook: Behavioral and economic segmentation that identifies high-value farm segments for focused go‑to‑market campaigns.

Note: In keeping with our “trailer” approach, the brief above highlights the structure and use of these deliverables — detailed datasets, regional/application split tables, and proprietary vendor scoring matrices are available exclusively in the full report.

For OEMs: Fast‑track integration of multi‑correction capabilities and telemetry monetization; protect installed base via upgrade pathways and subscription services.

For retrofit vendors: Scale certified installer networks, bundle sensor fusion upgrades (vision + GNSS), and pilot high‑touch subscription models with finance partners taking advantage of reimbursement programs.

For investors: Prioritize companies with network‑agnostic correction services, software revenue potential, and clear pathways to recurring revenue — those assets de‑risk longer sales cycles and benefit from policy tailwinds.

For policymakers and extension services: Focus on predictable reimbursement frameworks and technology‑neutral standards that catalyze adoption while avoiding vendor lock‑in.

Our findings are grounded in a blend of primary interviews with senior executives, installers, and farm operators; proprietary shipment and telemetry data; and supply‑chain mapping validated against public filings and industry sources. The base year is 2025, historical coverage spans 2020–2025, and our formal forecast period is 2026–2032. Revenue figures are expressed in USD (Million). While our headline projections are published here, the full methodology, sensitivity analyses, and proprietary scenario outputs are reserved for report purchasers.

PW Consulting’s Precision Agriculture GNSS Guidance System Market report is purpose-built for 2026 strategy cycles. It is the only package in the market that couples macro growth projections (including our 8.75% CAGR guidance) with executable playbooks, ROI tools, and vendor scorecards tailored to the dynamics described above. To access the full datasets, regional and application breakdowns, and the complete set of operational deliverables, please visit our report landing page (link in the distribution release) or contact PW Consulting’s industry desk for a briefing.

In 2026, a narrow set of decisions will determine who captures the majority of the growth in precision guidance — from product architecture and channel construction to policy engagement and after‑sales monetization. Our guidance turns uncertainty into options; the full report supplies the maps and the instruments to act.

— PW Consulting, Senior Strategy & Industry Analysis Team

For detailed analysis of this topic, please visit the official page:Precision Agriculture Gnss Guidance System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com