Handheld Multifunctional Scrubber Market — Strategic Briefing for 2026 Decision-Makers

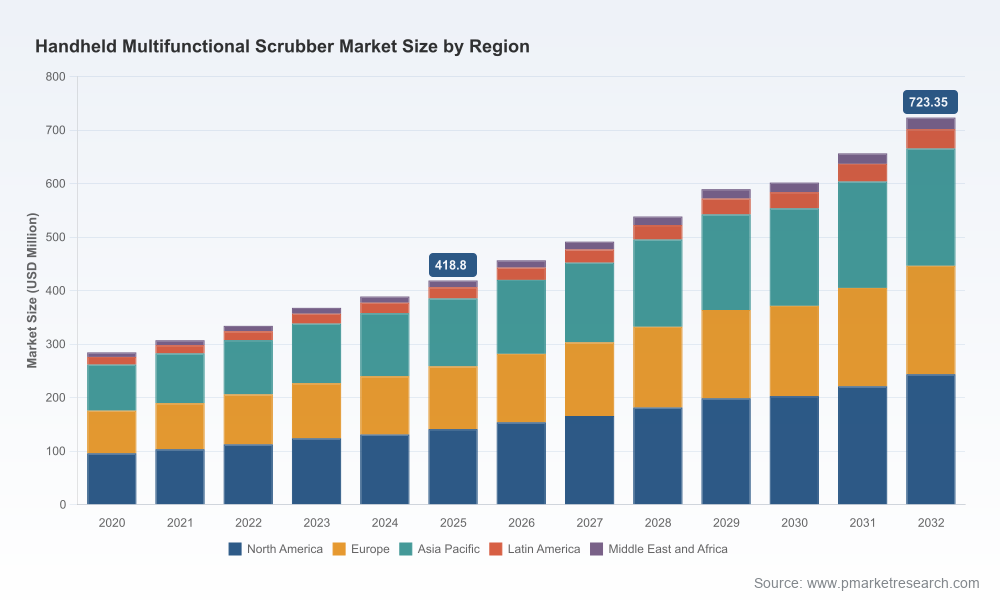

As PW Consulting releases its definitive market study on the Handheld Multifunctional Scrubber market, this briefing summarizes the strategic value our analysis delivers to corporate leadership preparing decisions in 2026. The market has moved beyond a novelty category to a durable segment within small home-cleaning solutions: between 2020 and our base year 2025 the addressable market expanded markedly, and our forecast—anchored on a compound annual growth rate of 8.12%—projects sustained growth through 2032. For leaders evaluating product roadmaps, channel investments, supply-chain hedges, or M&A targets, this report synthesizes the commercial and technical signals that will determine winners in the coming three- to five-year window.

Handheld Multifunctional Scrubber Market

Market snapshot: macro growth and competitive openness

Key macro takeaways: the category more than doubled in relevance over the past half-decade as consumers traded manual effort for compact motorized convenience. Our revenue model shows clear growth momentum into the forecast period (2026–2032) driven by cordless adoption, battery improvements, and broader acceptance of power-assisted cleaning across residential and light-commercial use cases. Importantly, market concentration remains modest: the top three vendors control roughly one-fifth of market spend while the top five account for just over thirty percent—an indication that brand, distribution, and product differentiation remain decisive factors rather than incumbency alone.

Handheld Multifunctional Scrubber Market

Why this matters for decisions in 2026

- Investment timing: An 8.12% CAGR creates a runway where early R&D and channel investments are likely to compound into market share gains by 2028–2030. Companies that commit in 2026 can capitalize on the next wave of cordless, brushless-motor products and attachment ecosystems.

- Portfolio strategy: The category's growth supports both focused single-product plays (high-margin, feature-rich units) and broader platform strategies (battery ecosystems, modular accessories). The choice affects required capex, partner strategy, and margin profile.

- M&A and partnerships: Given the fragmented vendor base and modest concentration, strategic acquisitions or exclusive distribution agreements remain effective routes to increase scale rapidly without multi-year organic brand building.

What the PW report delivers — practical, decision-ready content

The full report is a working toolkit for executives and functional leaders. Highlights include:

Handheld Multifunctional Scrubber Market

- Demand model: granular, SKU-level demand drivers and sensitivity testing for price, battery runtime, and distribution mix (presented as scenario outputs so you can stress-test your business case).

- Go-to-market playbooks: channel economics for direct-to-consumer, specialty retail, and big-box placements; promotional calendars and trade-event sequencing tailored by buyer persona.

- Product specs and roadmap diagnostics: prioritized feature sets (e.g., runtime, RPM bands, waterproofing standards, extension reach, and quick-connect systems) with a commercial viability assessment for each.

- Cost structure and supplier map: bill-of-materials archetypes, strategic single-sourcing risks, and nearshoring vs. offshore tradeoffs, including customs and tariff considerations impacting battery-powered handhelds.

- Competitive scorecards: vendor benchmarking across innovation, channel strength, price positioning, and serviceability—designed to support vendor selection, partnership screening, or M&A target shortlists.

- Implementation playbook: 90- and 180-day action plans for product launches, marketing pilots, and supply-chain resilience measures.

Technology and product dynamics

The category’s technical axis is dominated by three vectors: battery chemistry and pack design; brushless vs. brushed motor choices and resulting RPMs; and modularity of attachments. Lithium-ion advances are enabling runtimes that align with consumer expectations—several best-in-class units now advertise runtimes measured in multiple hours rather than minutes—while sealing and waterproof ratings (e.g., IPX7-class implementations) are becoming table stakes for safe bathroom use.

Product differentiation is increasingly feature-driven. Buyers value ease-of-use attributes—magnetic quick-connect heads, telescoping handles, integrated lights, and ergonomics—almost as much as raw power. Manufacturers investing in durable, serviceable attachments and a low-friction battery ecosystem are finding higher repurchase and accessory attach rates.

Competitive landscape: profiles and strategic implications

The landscape blends global household brands, digitally native challengers, and specialized Chinese OEM-led brands. Our analysis of leading players identifies distinct strategic archetypes:

- Design and brand champions: Established household brands that leverage their retail footprint and brand trust to sell premium, feature-rich units and secure end-caps in mass retail corridors.

- Rapid product-innovation challengers: Agile brands frequently launching differentiated motor and accessory combinations, winning awards and editorial recognition that translate into improved conversion in online channels.

- OEM/platform specialists: Cost-efficient manufacturers that compete on build-quality, price-performance, and breadth of interchangeable heads; these players often form the backbone of private-label and value-tier channels.

Selected company highlights (representative, not exhaustive):

- HOTO: positions itself on runtime and IP-rated durability, reinforced by recent editorial recognition that bolsters channel trust in premium cordless offerings.

- Casabella: leverages extendable-handle designs and household brand equity to target mainstream retail buyers seeking multifunctionality and ergonomics.

- Ruby Horsepower (Telebrands/BulbHead): focuses on high-RPM, mass-market appeal with a concise accessory set, aiming for broad online distribution.

- IEZFIX and LABIGO: representative of nimble China-based brands optimizing motor specifications and accessory ecosystems for global resale—strong in cost-performance tradeoffs.

- Large appliance/cleaning brands (Dirt Devil, Hoover, BLACK+DECKER): utilize platform synergies (battery systems, tool ecosystems) and full-line distribution to extend reach into adjacent cleaning categories.

The practical implication for incumbents and entrants: pursue either platform depth (battery and OEM partnerships) or niche feature leadership (e.g., highest RPM for grout cleaning or longest runtime for large homes) rather than attempting parity across every axis.

Regulation, supply chain, and sourcing risks

Battery classification and cross-border trade rulings have real operational impact. Recent customs classifications for battery-powered handheld scrubbers underline the need for rigorous HS code management and tariff planning. At the same time, reliance on specific battery-cell suppliers or single-source motor vendors concentrates operational risk. Our vendor heat maps identify the most-common single points of failure and propose practical mitigations, including qualified second-source strategies and local buffer stocking.

Channel and consumer behavior signals

Editorial tests and consumer reporting consistently show a preference for cordless units with long runtimes and multiple interchangeable heads. E-commerce reviews amplify installation and post-purchase experience—warranties, spare-head availability, and battery replacement options materially affect repurchase intent. Retail buyers favor units that demonstrate clear point-of-sale differentiation (packaging that highlights runtime, waterproofing, and quick-change heads) and have strong return-on-shelf metrics.

Recent developements that matter in 2026

- Product recognition and launches are shifting perception and raising the bar for new entrants (examples include award recognition for high-runtime models and major launches featuring brushless motors and expanded accessory kits).

- Platform announcements from established tool brands expand the category’s perimeter—battery-platform synergies now create cross-selling opportunities that can materially raise customer lifetime value.

- Regulatory precedents on import classification and battery transport have tightened operational requirements and increased the importance of compliance teams during sourcing and logistics planning.

Actionable recommendations — a 2026 playbook

- Prioritize a battery and service ecosystem: design for replaceable battery packs or cross-compatibility with existing tool ecosystems to increase attachment sales and reduce churn.

- Define a clear differentiation thesis: choose a primary axis—runtime, torque/RPM, or modularity/extension reach—and optimize product and marketing investments against that thesis.

- Invest in accessory economics: accessories drive margin and brand lock-in. Create a tiered accessory roadmap with predictable price points and simple distribution SKUs.

- Harden supply chains: qualify secondary battery and motor suppliers, and build tariff-compliant documentation to avoid customs-led disruptions during the peak seasonal cycle.

- Deploy a hybrid channel approach: combine DTC launches for innovation evangelism with targeted retail placements for scale; use editorial recognition and third-party testing to accelerate retail acceptance.

- Use M&A selectively: target bolt-on capabilities that accelerate time-to-market (battery tech, quick-connect systems, or accessory manufacturing capabilities) rather than broad, unrelated acquisitions.

Why PW Consulting’s report is different

Our study connects near-term tactical moves to long-term strategic outcomes. It provides executable templates—financial model inputs, SKU rationalization tools, and go-to-market checklists—that let leadership act with confidence in 90–180 day horizons, while our scenario-based forecasts illuminate options for 2028–2032 strategic positioning. To preserve the commercial sensitivity of buyers and suppliers, detailed segmentation outcomes, price ladders, and supplier-level revenue estimates are reserved for the full report and interactive database.

Next steps

For executives preparing capital allocation, product roadmaps, or M&A screening in 2026, the PW Consulting Handheld Multifunctional Scrubber report is designed to be the operational playbook you bring into cross-functional planning sessions. The full research package includes downloadable models, vendor scorecards, and a subscription to our quarterly tracker—visit the release page to access the complete dataset, detailed segmentation, and actionable annexes.

For detailed analysis of this topic, please visit the official page:Handheld Multifunctional Scrubber Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com