PW Consulting Strategic Briefing: Automated Side Load Garbage Trucks Market — What Decision‑Makers Must Know for 2026

As municipal fleets, private waste haulers, and vehicle OEMs move from pilot projects into scaled deployments, automated side load garbage trucks are rapidly evolving from niche assets into strategic fleet components. PW Consulting’s latest market study — anchored on a 2025 base year and projecting through 2032 — quantifies that transition and translates it into actionable guidance for 2026 planning cycles. The market expands at a compound annual growth rate (CAGR) of 6.42% across the forecast period, reflecting steady demand driven by regulatory pressure, labor economics, and technological maturation.

Automated Side Load Garbage Trucks Market

Executive snapshot

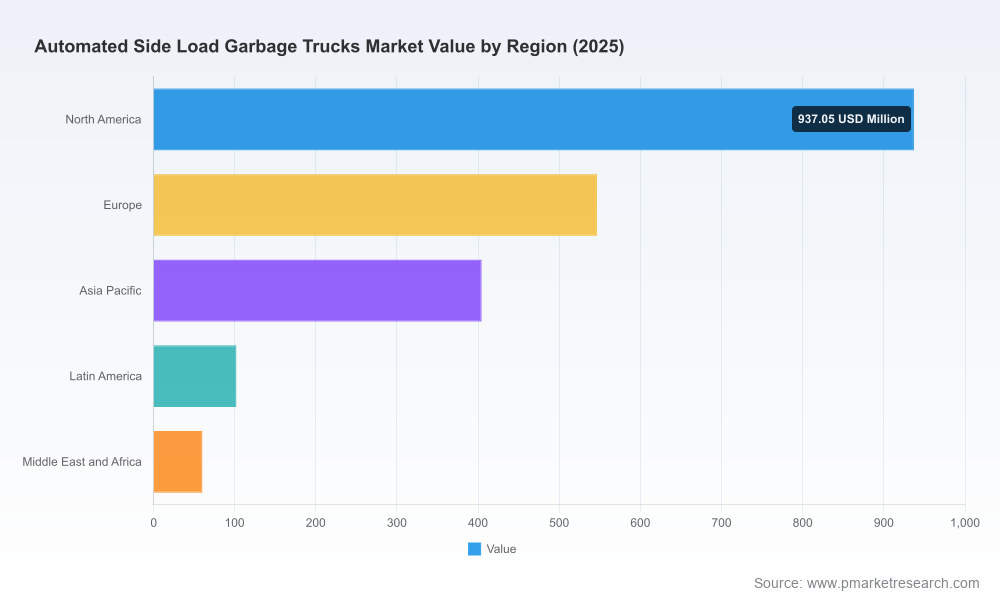

- Market trajectory: The automated side load garbage truck market has grown consistently since 2020 and shows continuous expansion through 2032, reflecting both replacement and new-route adoption dynamics. Our model uses 2025 as the analytical base to align with current procurement timetables.

- Concentration profile: The market is moderately consolidated — the top three players control a meaningful share but there remains room for midsized specialists and new entrants to secure niche positions. PW Consulting’s competitive index reports a CR3 near the mid‑40s and a CR5 approaching 60%, signaling both dominance and competitive opportunity.

- Regulatory + technology drivers: Tightening emissions rules and mandatory equipment safety directives are accelerating demand for low‑emission propulsion variants and more advanced sensor suites on automated side loaders.

Why this report matters for 2026 decision-making

2026 is the inflection point for several stakeholder groups. Municipal procurement budgets, grant cycles, and corporate CapEx planning for 2026–2028 are already being finalized; decisions taken now will determine fleet mixes and total cost of ownership for a decade. Our report provides the strategic inputs required to navigate three simultaneous pressures:

Automated Side Load Garbage Trucks Market

- Decarbonization: Locally mandated emissions targets and incentives are compelling fleet operators to evaluate electric, CNG, and hybrid solutions alongside diesel. The report quantifies technology readiness, integration costs, and the operational tradeoffs inherent in different propulsion strategies.

- Operational resilience: Labor scarcity and safety mandates increase the value proposition of automation. We translate field performance characteristics — including arm reach, container compatibility, and compaction behavior — into route‑level productivity metrics.

- Supply‑chain and aftermarket risk: With moderate market concentration, OEM selection has direct implications for spare parts, warranty terms, and service coverage. The report surfaces supplier dependency risks and mitigation strategies that are essential for procurement teams.

What the report delivers — practical, transaction‑ready intelligence

This is deliberately not a high‑level overview. PW Consulting’s market study was built to be operationally useful for procurement committees, fleet engineers, corporate strategy groups, and private equity teams assessing platform investments. Deliverables include:

Automated Side Load Garbage Trucks Market

- Strategic demand model: Scenario‑based forecasts aligned to procurement cycles, grant timelines, and policy shocks — enabling procurement teams to map acquisition windows and lifecycle costs.

- Total Cost of Ownership (TCO) matrices: Comparative TCO for diesel, electric, and CNG variants incorporating acquisition, fueling/energy, maintenance, and residual value assumptions tailored for municipal vs. private operator profiles.

- Regulatory compliance playbook: A checklist covering emissions requirements, OSHA/EU Machinery Directive safety expectations, and recommended safety sensor stacks including anti‑collision and operator‑presence monitoring.

- Supplier scorecards: Operational strengths, product differentiation, service footprint and innovation roadmaps for principal OEMs to inform RFP design and negotiation strategies.

- Retrofit vs. replacement decision trees: Criteria and financial models for deciding whether to retrofit existing chassis with automated bodies or procure new, integrated vehicles — including battery‑system and chassis compatibility assessments.

- Pilot and scale‑up templates: KPI definitions, pilot duration and scale guidance, and sample contract clauses to accelerate deployment while avoiding common procurement pitfalls.

Competitive landscape — who matters and why

The automated side loader landscape combines legacy equipment manufacturers, specialized body builders, and niche innovators. Our analysis synthesizes company positioning across product breadth, technology integration, and route‑level performance.

- Heil Environmental — Known for a broad portfolio of continuous‑pack and rapid‑pack bodies, Heil combines proven mechanical architectures with an increasingly visible electric strategy (for example, independent battery systems dedicated to collection work). Heil’s scale and product depth make it a default choice for large fleets seeking a predictable supply chain and rapid dealer support.

- McNeilus Truck and Manufacturing — McNeilus emphasizes versatility on residential routes through designs optimized for tight environments. Its model set that spans Zero Radius to AutoReach demonstrates a focus on maneuverability and ergonomic arm designs, making it attractive to operators with dense urban routing constraints.

- Labrie Enviroquip Group — Labrie’s portfolio centers on adaptable bodies that can operate across manual, semi‑automated, and fully automated configurations. For municipalities prioritizing gradual automation, Labrie’s flexibility reduces transition risk.

- New Way Trucks — With options emphasizing lift capacity and under‑CDL configurations, New Way targets operators looking for a balance between capacity and regulatory driving‑license thresholds, an important consideration for staffing models.

- Amrep — Durability is Amrep’s signature, leveraging wear‑resistant steels and robust hoist designs suited to heavy commercial operations. Amrep is frequently selected where fleet uptime under heavy duty cycles is the top priority.

- Curbtender Inc. — As the originator of the automated side loader in commercial production, Curbtender retains a reputation for focused specialization. Its narrower product set is offset by deep operational experience and niche customer loyalty.

- KANN Manufacturing — KANN’s compact and high‑compaction bodies target operators looking to maximize payload and compaction efficiency, with flexible tip and eject configurations enabling different service models.

For buyers, the choice among these suppliers is not binary. Tradeoffs between durability, arm reach and control systems, electric integration, and aftermarket responsiveness must be balanced against local route profiles, workforce availability, and financial constraints. Our vendor scorecards convert these subjective tradeoffs into procurement‑ready comparison metrics.

Regulatory and technical dynamics shaping 2026 deployments

Two intersecting regulatory vectors are shaping procurement decisions.

- Emissions and incentive regimes in key markets are accelerating interest in low‑ and zero‑emission powertrains. The market’s commercial response includes both chassis‑level electrification and body‑level battery systems that perform collection duties independently of the chassis powertrain.

- Safety and machine‑directives push OEMs to integrate anti‑collision sensors, operator presence detection, and reliable emergency override mechanisms. Compliance is non‑negotiable and must be validated during acceptance testing.

From a technical standpoint, common field design parameters — such as hydraulic actuation, container compatibility (30–300 gallon range), reach envelopes, and compaction performance — remain the levers that determine operational productivity. Electric body architectures that isolate battery systems for collection tasks are emerging as a pragmatic bridge technology for operators who want electric collection capability without a full electric chassis fleet today.

Scenario planning: how to act in 2026

We recommend structuring 2026 decisions around three plausible scenarios:

- Conservative transition — Prioritize diesel replacements with readiness for later conversion; focus on supplier terms that facilitate retrofits and ensure spare‑parts availability.

- Baseline adoption — Adopt mixed powertrain fleets, pairing new electric‑capable bodies with selective electric chassis where route density and depot charging economics support it.

- Accelerated decarbonization — Commit to rapid electrification for high‑utilization routes, couple procurement with charging infrastructure investment, and lock in service contracts that prioritize uptime and battery lifecycle management.

Across scenarios, PW Consulting emphasizes four near‑term actions for 2026 planners: implement route‑level TCO logic to inform unit selection; modularize RFPs to preserve retrofit options; require phased acceptance and performance KPIs; and stress‑test supplier warranties against real route cycles.

Priority strategic recommendations

- For fleet operators: build a three‑year rolling acquisition plan that matches vehicle type to route density and regulatory timelines; prioritize vehicles that allow phased electrification.

- For OEMs and body builders: accelerate integration testing of battery‑assisted collection systems and expand service footprints to reduce operator switching costs.

- For investors and private equity: target acquisitions that plug service and regional coverage gaps among mid‑tier players — the market still rewards scale in parts and service.

- For municipalities and regulators: design incentive programs that account for lifecycle costs and total municipal benefits (safety, noise reduction, emissions), not just purchase price.

Next steps and how to access the full intelligence

This briefing is a strategic preview designed to orient 2026 planning. PW Consulting’s full market report contains the proprietary segmentation models, detailed regional and chassis‑capacity scenarios, supplier scorecards with quantified performance metrics, and downloadable procurement templates that support immediate RFP execution.

To unlock the complete dataset — including the granular regional and application‑level splits, downloadable financial models, and the supplier benchmarking matrix — please visit our report page. The full intelligence package is structured to be operational on day one of your 2026 procurement and technology roadmap planning.

For detailed analysis of this topic, please visit the official page:Automated Side Load Garbage Trucks Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com