Global External Solid State Drives Market Growing at 7.2% CAGR Through 2032

Other |

2026-07-01 12:52:13

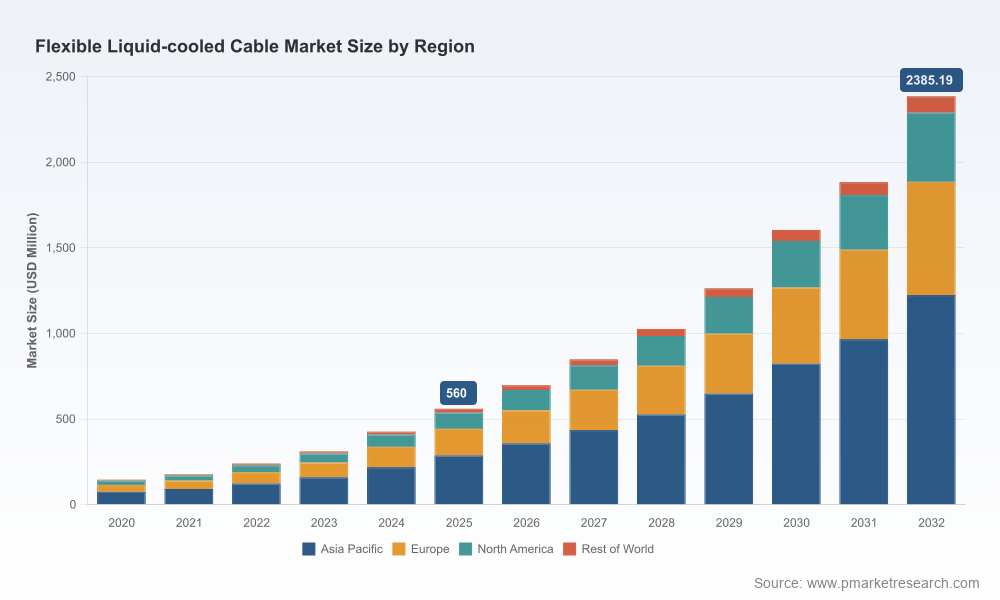

As companies race to deploy ultra-fast electrification and industrial power upgrades, flexible liquid-cooled cables have moved from niche engineering components to strategic infrastructure enablers. PW Consulting’s latest market study shows a market that has expanded rapidly in the first half of the decade — rising from roughly USD 145 million in 2020 to about USD 560 million in 2025 — and that is on track to compound at an estimated 23.01% CAGR through our forecast window. By 2032 the market is modeled to exceed USD 2.3 billion. For executives making capital allocation, product, and partnership decisions in 2026, these macro dynamics create both urgency and opportunity.

Flexible Liquid Cooled Cable Market

Megawatt-class EV charging and high-current industrial applications are becoming commercially material. The technical requirement to sustain high currents (typically in the hundreds to low thousands of amps) while keeping cable weight, flexibility, and handling ergonomics acceptable has put liquid cooling at the center of next-generation cable designs.

Flexible Liquid Cooled Cable Market

Standards and certifications are moving from concept to practice. Compliance dimensions such as connector standards and insulation/temperature limits (IEC and UL families, among others) are now binding constraints on product design and go-to-market timelines. Notably, the market received a milestone certification for 1 MW-capable liquid cooling in 2025, establishing an assurance baseline for high-power deployments.

Flexible Liquid Cooled Cable Market

Component-level engineering choices — copper conductor grades, coolant media and hose materials, and terminal/swivel designs — materially affect both performance and total cost of ownership. High-conductivity electrolytic copper remains the dominant conductor due to its thermal and electrical performance; protective hose and high-temperature tubing choices determine durability and maintenance cadence.

Our market sizing shows a steep growth trajectory that validates strategic investment: five-year historical expansion followed by a high double-digit compound annual growth rate through 2032. We use that top-line trajectory to stress-test three executive questions: where to place manufacturing capacity, what partner ecosystems to build, and which technology bets to prioritize. Deliberately, this public briefing avoids disclosing the detailed split of revenue by region, application or product-type — that granularity is available in the full report and is the exact intelligence needed to operationalize the strategic options we outline below.

The industry exhibits a hybrid structure: established specialists that serve traditional industrial heating, welding and furnace markets and an emerging cohort targeting electric vehicle high-power charging. Market concentration is meaningful but not monopolistic — our CR3 sits in the low forties percent range while CR5 is under 60% — indicating room for both consolidation and niche players focused on superior engineering or integration expertise.

Industrial-specialist segment: A group of firms with deep craftmanship and customization capabilities serves induction heating, arc/electric furnaces, and resistance welding markets. These suppliers compete on turnaround time, terminal and swivel designs, and the ability to fabricate large-section water-cooled conductors. Their strengths are custom engineering and service-led relationships with OEMs and plant operators.

EV and HPC-focused segment: A second cluster is oriented toward standardized connector platforms, ergonomics, and system integration for public and fleet charging. These players emphasize direct liquid-cooling innovations, high-voltage architectures, and partnerships with charger OEMs to deliver certified, user-friendly solutions suitable for high-throughput commercial deployments.

Representative company capabilities we examined include custom fabrication and retrofit services, rope-lay and stranded conductor constructions, ergonomic strain-relief designs, and integrated connector-platform offerings. Recent market activity underscores these bifurcated value propositions: product integrations by charging-system OEMs, product introductions targeting ultrafast EV charging, and field deployments of megawatt-capable chargers.

Commercial integrations continue to accelerate: a leading charging OEM integrated a 1,000 A liquid-cooled CCS2 cable into a high-power charger platform, signaling OEMs’ willingness to adopt third-party liquid-cooled cable systems when compliance and ergonomics meet expectations.

Product innovation remains steady among industrial suppliers, with updated catalogs emphasizing customizable lead times and optional safety enhancements (e.g., fire-retardant sleeves) — evidence that service and aftermarket support are competitive differentiators.

Field validation is advancing: a North American deployment demonstrated successful charging at >1 MW with liquid-cooled cable technology, moving the conversation from lab to live operation and reducing perceived deployment risk.

Regulatory progress has continued: world-first certifications for 1 MW-class liquid-cooling platforms have been announced, which we expect to accelerate procurement decisions by asset owners who require demonstrable safety pedigrees.

Below are the high-conviction actions we recommend for corporate leaders who need to translate the market’s top-line growth into competitive advantage in 2026. These are prioritized to manage risk, accelerate market entry, and protect margin.

Secure raw-material and manufacturing continuity: Lock long-term copper and critical-material supply terms or hedges while sizing flexible fabrication capacity that can handle both small-batch custom orders and scale windows for EV charging volumes.

Pursue standards and certification early: Achieve or partner to obtain the relevant IEC/UL/ISO certifications before large tenders are issued — certification timelines are a gating factor for many buyers and can be a durable moat.

Form charger-OEM alliances and pilot programs: Integrate cable design and ergonomics into charger system development cycles. Co-engineering arrangements shorten qualification cycles and position suppliers as preferred vendors for network rollouts.

Differentiate via service and modularity: Offer swap- or field-serviceable terminations, robust swivel designs, and field diagnostics. For many industrial buyers, lifecycle cost and uptime are as decisive as price.

Build a dual-track product roadmap: Maintain bespoke industrial lines while developing modular, certified platforms for EV HPC. This hedges demand variability and leverages overlapping manufacturing capabilities.

Evaluate M&A or JV options to capture scale quickly: Given the current fragmentation, strategic acquisitions can accelerate entry into high-growth subsegments where time-to-contract matters more than organic development speed.

PW Consulting’s full market study is engineered as a decision-support toolkit for 2026. Key deliverables include:

A transparent market-sizing and forecast model (base year 2025, historical 2020–2025, forecast 2026–2032) with sensitivity scenarios to stress-test price, volume, and certification-adoption assumptions.

A regulatory and standards matrix mapping certification pathways across EV charging and industrial heating applications, with estimated timelines and testing requirements.

Supplier and buyer landscapes with capability maps and go-to-market playbooks tailored for OEMs, Tier-1 suppliers, charging network operators, and industrial end-users.

Supply-chain and margin models that simulate copper-price shocks, manufacturing scale-up economics, and aftermarket-service revenue streams.

Detailed competitive profiles and benchmarking of leading suppliers (product architectures, IP posture, channel strategies), plus a menu of strategic options — partnerships, licensing, M&A, and greenfield investments — prioritized by expected payback under our forecast scenarios.

The market’s strong trajectory is clear: expanding commercial demand, converging standards, and landmark field deployments collectively lower the barriers to scale. For 2026, the strategic question is not whether to participate, but how to enter and win sustainably. PW Consulting’s research equips leaders with the scenario-tested levers needed to move from intent to execution: from supply-chain resilience and certification-first product design to alliance-based go-to-market strategies and selective inorganic plays.

For companies that need the underlying segment-level detail, supplier scorecards, and executable financial models to operationalize these recommendations, the full report contains the necessary data and templates — intentionally withheld from this briefing to preserve the value of that proprietary intelligence. Contact PW Consulting to access the complete study and the model files that will translate macro trends into capital and product decisions for 2026.

For detailed analysis of this topic, please visit the official page:Flexible Liquid Cooled Cable Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com