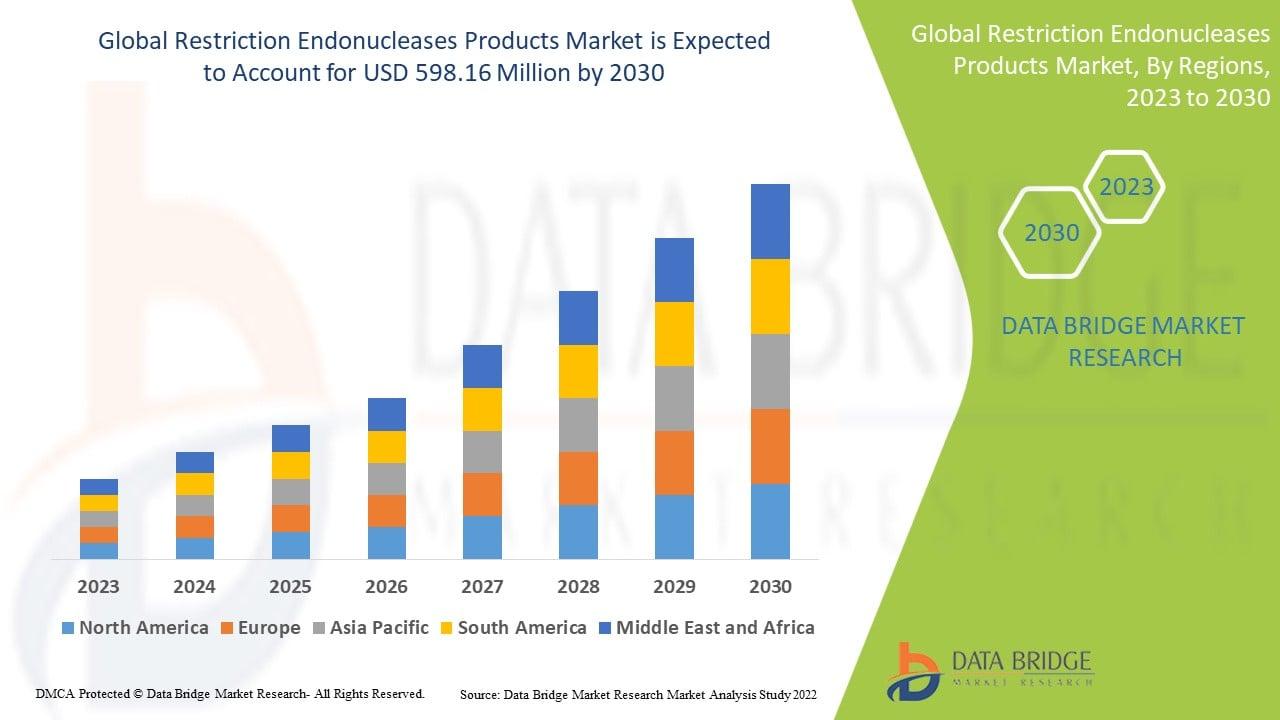

Restriction Endonucleases Products Market Growth and Demand Analysis

Other |

2026-05-05 09:11:16

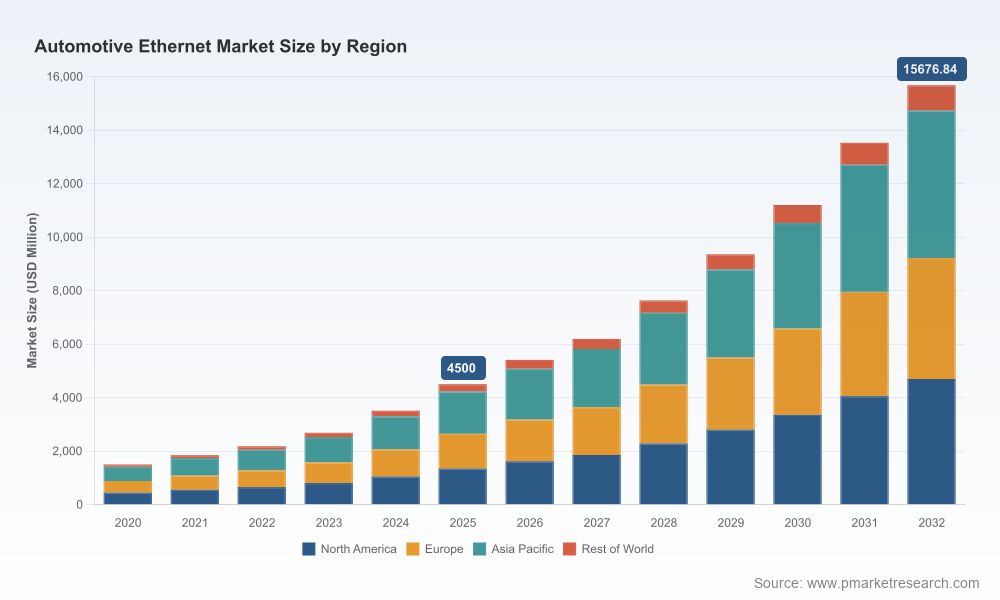

PW Consulting’s latest Automotive Ethernet Market report (base year 2025; forecast 2026–2032) delivers a pragmatic, decision‑ready playbook for OEMs, Tier‑1 suppliers, semiconductor vendors and strategic investors planning capital allocation and product roadmaps in 2026. The market has entered a rapid scaling phase: after accelerating through 2020–2025, the total market reached approximately USD 4.5 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of roughly 19.5% over the 2026–2032 forecast window—surpassing the mid‑teens billion dollar threshold by the end of the period. This report synthesizes market dynamics, regulatory and standards drivers, technology bottlenecks and competitive positioning into actionable strategies while deliberately reserving granular segment and regional tables for report subscribers.

Automotive Ethernet Market

Timing hardware investments: The high CAGR anchors a window in 2026 when investments in PHYs, switches, and domain controller architectures yield disproportionate share gains. Decisions on silicon node selection, PHY family commitment, and assembly alignment will determine whether suppliers capture early zonal and centralized architectures.

Automotive Ethernet Market

Prioritizing product roadmaps: With bandwidth demand driven by ADAS, infotainment and centralized compute architectures, strategic prioritization between low‑cost multi‑drop solutions and high‑speed 10G links is now a make‑or‑break choice for semiconductor firms and module OEMs.

Automotive Ethernet Market

Supply‑chain risk and scale planning: Rapid growth increases supplier consolidation pressure; our market concentration analysis shows a moderately concentrated supplier landscape (top‑3 and top‑5 share metrics indicate leading incumbents retain significant influence), which affects negotiation leverage, lead‑times, and qualification cycles in 2026.

Regulatory and certification calendars: New type‑approval and cybersecurity rules have shifted procurement timelines—UN ECE R155 and evolving OPEN Alliance standards create compliance gating factors that must be reflected in procurement and product‑release milestones.

Market sizing and validated forecasting model (2020–2032) with scenario variants for technology adoption curves and OEM architecture choices—designed for integration into financial planning and capex models.

Go‑to‑market playbooks for semiconductor vendors and Tier‑1 module integrators covering pricing cadence, sample‑to‑production timelines, and qualification checklists aligned with vehicle program cycles.

Technology roadmaps and engineering decision matrices: PHY selection frameworks (tradeoffs among 10BASE‑T1S, 100BASE‑T1, 1000BASE‑T1 and 10GBASE‑T1), shielding and cable strategies, and validation templates to shorten time‑to‑system‑integration.

Supply‑chain stress tests and supplier scorecards: critical‑path mapping, alternate‑source playbooks, and inventory/consignment recommendations tailored to supplier concentration and lead‑time risk.

Compliance tracker and certification playbook: mapping of ISO, OPEN Alliance and UNECE requirements to product release gates to reduce rework and late‑stage program slips.

Investor intelligence appendix: market sizing, unit economics, margin benchmarks and a heat‑map of strategic M&A targets by technology and geographic presence (note: detailed transaction multiples and target valuations are available in the full report).

The report provides a calibrated view of incumbent capability and momentum across semiconductors, systems integrators and test & validation vendors. Market concentration metrics indicate that the top three vendors account for a meaningful share of revenue, while the top five broaden the competitive moat—an important consideration for new entrants evaluating scale economics.

Broadcom Inc. (San Jose, CA): A leader in automotive‑grade PHYs and switches, Broadcom’s BroadR‑Reach lineage and push into 10GBASE‑T1 compliance (recent OPEN Alliance TC10 certification) underscore its strategy to own high‑bandwidth backbone interfaces for software‑defined vehicles. Expect continued investments in silicon integration and OEM partnership programs.

Marvell Technology (Santa Clara, CA): Marvell has translated high‑speed PHY capability into vehicle integrations, evidenced by recent platform deployments with OEMs. Their multi‑rate portfolio positions them to capture both next‑gen ADAS transport and high‑bandwidth infotainment lanes; strategic differentiation will hinge on software stacks and PHY‑to‑SoC optimization.

NXP Semiconductors (Eindhoven): NXP’s sustained focus on MAC‑PHY integration and zonal switch products targets the OEM move toward centralized compute and zonal architectures. Recent product launches tailored for zonal domains indicate NXP’s offensive play to influence wiring‑strategies and domain controller content.

Texas Instruments (Dallas, TX): TI continues to compete on cost‑performance for mainstream architectures, with product families that aim to serve high‑volume vehicle programs. Their competitiveness in price‑sensitive segments makes them a strategic partner for Tier‑1s optimizing BOMs.

Microchip Technology (Chandler, AZ): Microchip’s PHYs and automotive‑grade switches are positioned for gateway and domain controller tiers; combined with a strong portfolio in mixed‑signal and connectivity, they’re a pragmatic choice for integrators focused on robustness and qualification track records.

Analog Devices (Wilmington, MA): With long‑reach and sensor‑optimized PHYs, ADI addresses use‑cases where extended cable lengths and sensor connectivity are paramount—an important niche as vehicles incorporate more distributed sensing.

Renesas Electronics (Tokyo): Renesas’ SoC‑level integration of high‑speed Ethernet shows an intent to consolidate ECU count by embedding Ethernet into central compute platforms. Their collaborations with Tier suppliers signal an aggressive roadmap for ECU consolidation.

TTTech Auto (Vienna): TTTech’s MotionWise deterministic switches target the software‑defined vehicle’s need for time‑sensitive networking. Demonstrations of 10Gb deterministic switching highlight a path for safety‑critical Ethernet fabrics.

Vector Informatik (Stuttgart) and Intrepid Control Systems (Madison Heights): Test, validation and diagnostics vendors are extending toolchains to support 100BASE‑T1 through 10GBASE‑T1 profiles—critical infrastructure as OEMs shorten verification cycles and raise compliance bars.

Product launches and certifications (2025): A flurry of activity—new zonal switches, 10GBASE‑T1 certifications and OEM integrations—signals that the transition from pilot to production scale has accelerated; suppliers who miss 2026 qualification windows risk being left on incremental content opportunities only.

OEM platform moves: Integrations of high‑bandwidth PHYs into flagship vehicle programs indicate that bandwidth demand for ADAS and centralized compute is not hypothetical—it is being specified today. This pushes decision timelines for silicon partners and cable/connector suppliers.

Standards and regulation tightening: ISO standards for PHYs and OPEN Alliance work items for multi‑drop and high‑speed links, together with UNECE cybersecurity mandates, raise the bar for functional safety and secure in‑vehicle communications. Suppliers must embed compliance engineering into product roadmaps rather than treat it as an afterthought.

Signal integrity and EMI for multi‑Gbps PHYs: 1000BASE‑T1 and beyond impose advanced signal‑processing and PHY‑level equalization to mitigate electromagnetic interference in unshielded twisted pair environments. These engineering costs and qualification cycles are a recurring theme in supplier due‑diligence.

Protocol determinism and latency: As vehicles consolidate compute, deterministic Ethernet switches and TSN support become critical for safety‑relevant domains—creating differentiation opportunities for vendors who can certify latency and redundancy performance.

Safety and power trade‑offs: Design constraints such as exclusion of PoDL for certain PHY profiles due to functional safety isolation requirements force system architects to separate power distribution decisions from data link choices, influencing harness architecture and cost.

Align product qualification timelines with OEM program gates: Prioritize resources to meet the 2026–2027 program award and sampling windows—late qualification will mean lost content on multi‑year vehicle programs.

Adopt a two‑track silicon strategy: Maintain a high‑performance line for 10G and 1G backbones while preserving a cost‑optimized family for sensor and multi‑drop links; invest in PHY‑to‑SoC software co‑design to shorten integration cycles.

Lock in strategic supplier agreements now: Given concentration metrics and lead‑time risk, secure long‑lead components and test resources through multi‑year agreements or strategic equity/partnerships to ensure continuity of supply.

Embed compliance and cybersecurity early: Map ISO, OPEN Alliance and UNECE requirements to product release gates and integrate security‑by‑design into firmware and network management stacks to avoid late rework.

Use the report’s scenario models to stress‑test investment options: Leverage our sensitivity analyses to identify the breakpoint where accelerated R&D or capacity expansion delivers positive NPV under different adoption curves.

The downloadable report contains detailed segment forecasts, regional demand models, supplier scorecards, bill‑of‑materials benchmarks and a prioritized list of technical due‑diligence questions for partnership negotiations. To preserve actionable advantage for report subscribers, the press summary intentionally omits the detailed tables and segment percentages; these are available in the full report package alongside the underlying model spreadsheets and workshop‑ready slide decks designed for executive briefings.

For executive teams preparing 2026 budgets and 3‑year strategic plans, PW Consulting recommends commissioning a tailored workshop where we overlay your product and supplier lineup onto our adoption scenarios. This focused engagement converts the macro forecast and strategic recommendations into a prioritized, executable roadmap tied to your procurement and R&D milestones.

Contact PW Consulting to schedule a briefing and obtain access to the full Automotive Ethernet Market report and the interactive forecast model.

For detailed analysis of this topic, please visit the official page:Automotive Ethernet Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com