Autonomous Robot Market Accelerates as Industries Pursue Greater Efficiency and Automation

Networking |

2026-06-18 13:24:00

PW Consulting’s new market intelligence pack on the Rubber Milk Tubing and Hose market delivers a decision-grade perspective for executives planning resource allocation, product roadmaps, and M&A through 2026 and beyond. Built on a five-year historical base (2020–2025) and a forward-looking 2026–2032 forecast, the analysis demonstrates a steady recovery and expansion: the market rose from under USD 400 Million in 2020 to USD 485.6 Million in the report base year (2025), and is modeled to grow at a compound annual growth rate of 4.81% through the forecast window, reaching approximately USD 674.2 Million by 2032. This briefing summarizes why that trajectory matters, what operational levers it reveals, and how senior leaders should convert insight into action — while preserving the deeper, transaction-ready analytics in the full report.

Rubber Milk Tubing And Hose Market

Market momentum is moderate but durable. The mid-single-digit CAGR masks important pockets of volatility driven by raw material swings, sanitary regulation tightening, and evolving milking system architectures. 2026 will be the year many OEMs and major dairy processors either consolidate specifications or pursue differentiated materials and services to lock in margins.

Rubber Milk Tubing And Hose Market

Cost and compliance intersect. Recent movements in rubber and polymer prices and a higher-profile regulatory focus on food-contact materials mean procurement, product development, and compliance must coordinate more closely than they have historically.

Rubber Milk Tubing And Hose Market

Fragmentation leaves optionality. Market concentration metrics show industry leadership without dominance — the top-three players account for approximately one-third of market revenue, and the top five sit below 50% share. That structure creates strategic windows for challengers, niche specialists, and acquisitive players.

The report is designed as a playbook, not an academic exercise. Highlights of operational relevance include:

Quantitative market-sizing and validated demand archetypes across the forecast horizon, with sensitivity scenarios for cost shocks and regulatory tightening.

Supply‑chain mapping from raw rubber and EPDM through compounding and extrusion to finished tubing and hoses — identifying single‑point risks, lead‑time drivers, and margin sinks.

Regulatory and hygiene checklist tied to procurement specifications (FDA 21 CFR 177.2600, 3‑A sanitary guidance, NSF‑51 and BfR expectations), with pass/fail implications for product variants and manufacturing practices.

Competitive scorecards and capability heat maps (manufacturing footprint, material competencies, certifications, OEM relationships), enabling rapid shortlists for partnership, supplier consolidation, or acquisition.

Commercial playbooks — pricing levers, contract structures, and aftermarket service models that protect margin while addressing farmer and processor demand elasticity.

Investment cases and near‑term M&A screening: focused target profiles, valuation heuristics, and integration risk checklists for 2026 deal activity.

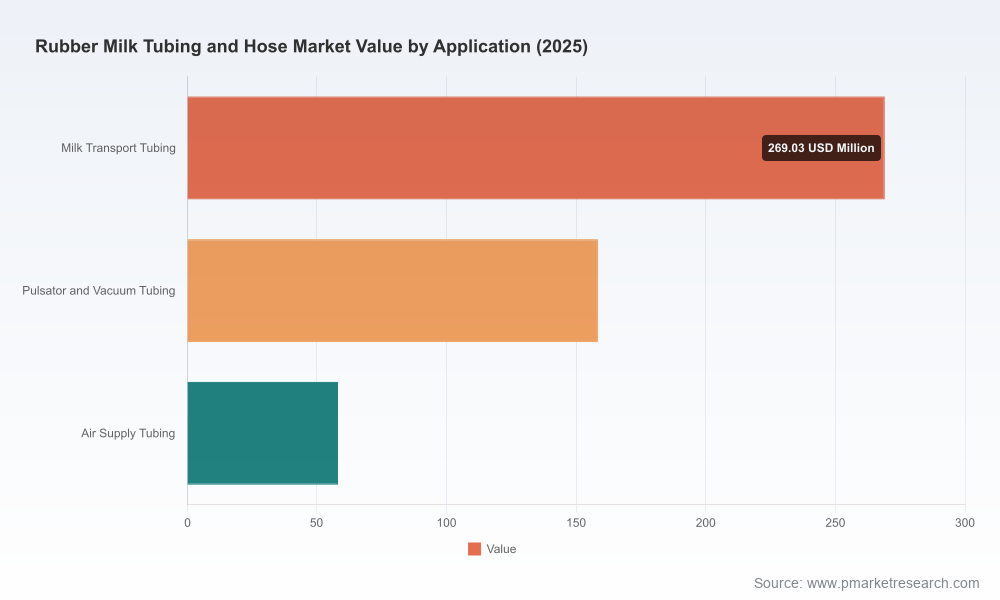

Because this briefing follows a “trailer” principle, segment-level allocations and granular regional/application revenue splits are intentionally withheld here; the full dataset, appended models, and supplier scorecards are available through the PW Consulting report page.

Raw material volatility has resumed as a defining margin factor. Natural rubber benchmarks softened in early 2026 relative to prior peaks, and EPDM prices exhibit geographic dispersion that impacts sourcing strategy for global manufacturers. These price movements materially change the economics of natural rubber vs. synthetic replacements and influence compound selection for milk-contact products.

Industrial price indices corroborate sector-level cost pressure. Producer indices for rubber and plastics hose show upward momentum compared with prior cycles, underscoring that pass-through to customers and contract design will be critical to preserve profitability.

Standards and sanitary expectations remain non-negotiable. Food‑contact compliance (FDA, 3‑A, NSF, BfR) is both a market access gate and a differentiation axis — products that demonstrably reduce biofilm formation and ease cleanability command lower switching friction and premium positioning.

The market is populated by specialized rubber firms, global elastomer platforms, and niche OEM suppliers. The PW Consulting report profiles leading players and evaluates their strategic posture across manufacturing, certification, and go-to-market execution:

U.S.-based silicone specialists bring strong food‑grade credentials and quick customization cycles. These manufacturers emphasize 100% FDA‑compliant silicones, ISO quality systems, and product lines tailored to dairy parlors and milking systems. Their key strengths are rapid prototyping, tight sanitary compliance, and proximity to North American dairy markets.

Established European hose makers couple compound engineering with full-system hose assemblies for processing plants and tanker transfer — blending hygienic design, smooth non‑porous finishes, and certifications that ease export to regulated dairy markets. Their advantage is integrated product portfolios and scale in processing-plant applications.

Specialty manufacturers focus on twin or pulsation hoses, niche sizes, and OEM partnerships. These firms succeed through configurable SKUs, color-coding and traceability programs, and service‑oriented stocking agreements with distributors and integrators.

Across the competitive set, certification and traceability are differentiators: firms that carry multiple food‑contact certifications and can demonstrate hygienic extrusion practices command greater trust with large dairy processors and integrators.

Collectively, the industry structure offers both a defensive playbook for incumbents (protect install base via certification and aftermarket service) and an offensive route for challengers (target underserved product niches, offer better TCO, or pursue bolt‑on acquisitions in regional markets).

Based on scenario runs and supplier diagnostics, PW Consulting recommends a prioritized set of moves for manufacturers, purchasers, and investors operating in or adjacent to the rubber milk tubing and hose market.

Board level: Use the forecast scenarios and concentration analysis to test strategic choices — defend, divest, or expand — under different market and raw-material paths.

Commercial leadership: Adopt the pricing and service playbooks to rebalance revenue toward higher-margin aftermarket offerings and away from commoditized volume competition.

Procurement and operations: Implement the supplier scorecard and risk maps to restructure supplier portfolios and reduce single-supplier exposure for critical compounds.

Corporate development: Leverage the M&A shortlist and valuation heuristics when screening targets who can close capability gaps or accelerate market access.

This briefing highlights the strategic value of the Rubber Milk Tubing and Hose market study for 2026 planning: clear growth, acute material and regulatory levers, and tactical options for differentiation and consolidation. For transaction-ready detail — full segment and regional breakouts, supplier scorecards, downloadable financial models, and an actionable M&A shortlist — access the PW Consulting report and model package. The full deliverable contains the granular data and operational templates you will use to convert this strategic briefing into executable plans and measurable KPIs.

Contact your PW Consulting representative or visit our report page to request the complete dataset, model workbook, and an executive briefing with our senior analysts.

For detailed analysis of this topic, please visit the official page:Rubber Milk Tubing And Hose Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com