Siti non AAMS: I Segreti dei Migliori Siti di Scommesse

Networking |

2026-05-21 20:08:43

PW Consulting today publishes a forward-looking industry brief drawn from our comprehensive Cryoablation For Cancer Market research (base year 2025, forecast 2026–2032). As healthcare systems, device manufacturers, and investors prepare plans for the coming year, our analysis shows the market continuing a strong trajectory — growing from an established mid‑hundred‑million USD level in 2025 toward near‑billion dollar scale by the end of the forecast horizon, at an expected compound annual growth rate of approximately 9.42%. This brief summarizes the high‑impact trends and strategic levers that will matter for decisions made in 2026, while preserving the report’s proprietary segmentation and model outputs for subscribers and clients.

Cryoablation For Cancer Market

Between 2020 and 2025 the cryoablation market demonstrated resilient expansion underpinned by steady clinical adoption and improving commercial access. Our 2026–2032 forecast encapsulates a continuation of that momentum: the market is projected to more than double in scale over the coming six years under a mid‑single‑digit to high‑single‑digit CAGR profile (9.42% point estimate). For strategy teams, that growth translates into an environment of accelerating commercial opportunity alongside intensifying competition — a classic window for both incumbents to defend and challengers to scale rapidly.

Cryoablation For Cancer Market

Key strategic takeaways for 2026 budget and resource planning:

Cryoablation For Cancer Market

Our analysis identifies three converging catalysts that will meaningfully influence adoption in 2026:

PW Consulting’s full report models the timing and sensitivity of each catalyst against adoption curves across care settings. The headline implication: firms that can synchronize evidence generation, reimbursement engagement, and capital‑efficient commercial models will secure the early majority of the addressable market growth over the next 24‑36 months.

The cryoablation market displays a concentrated structure at the top, with the largest players accounting for the majority of market value. This concentration creates a dual strategic reality: established players benefit from strong channel reach and installed bases, while the competitive moat is porous for innovators who bring differentiated clinical data, lower‑cost consumables, or superior imaging integration.

Key industry participants profiled in our research include:

Recent company developments captured in our brief illustrate the speed at which regulatory and clinical milestones translate into market opportunity. For example, the clearance pathways and sponsored post‑market trial activity for selected devices have already changed messaging to surgeons and multidisciplinary tumor boards. The competitive consequence is clear: defenders must accelerate real‑world evidence (RWE) campaigns while challengers should use targeted clinical programs to justify access in highly selective patient segments.

Our on‑the‑ground interviews and commercial due diligence point to five levers that will separate winners from also‑rans in 2026:

Each lever is unpacked in the full report with practical playbooks, contract language examples, and sensitivity models that allow commercial teams to stress‑test revenue and margin outcomes under different adoption scenarios.

Beyond market sizing and high‑level trends, the report is intentionally operational. Highlights include:

Recent regulatory clearances and guideline updates have moved cryoablation from niche curiosity toward an accepted option in selected early‑stage settings. These clinical endorsements materially reduce the friction for payers and procurement committees. At the same time, coding clarity—where available—has created predictable reimbursement flows that providers can use to evaluate new programs.

For manufacturers and investors, the immediate strategic task is twofold: (1) accelerate payer economics dossiers that translate clinical outcomes into facility and system level savings; and (2) expand evidence packages to demonstrate comparative effectiveness across competing ablative modalities. The report contains templates and payer‑facing economic models that teams can adapt to support local coverage determinations and hospital‑level value analyses.

Based on our integrated market, clinical, and commercial analysis, PW Consulting recommends that executive teams prioritize the following actions in 2026:

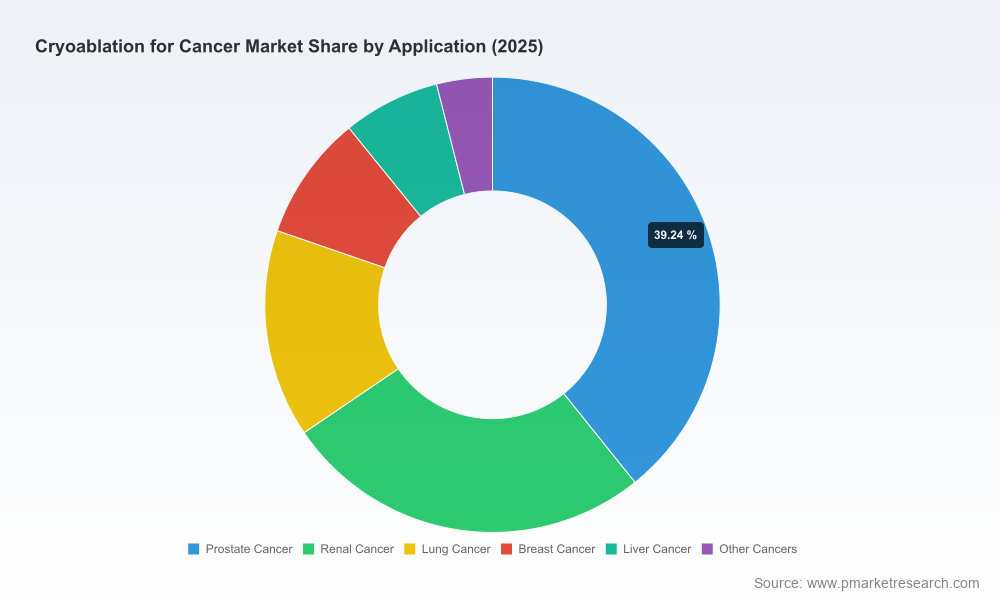

This intelligence brief captures the strategic contours that will matter for 2026 decision cycles. PW Consulting’s full Cryoablation For Cancer Market report provides the underlying data tables, proprietary segmentation by product, application, and region, as well as downloadable models and slide decks designed for board and investor briefings. If your 2026 plans hinge on a clear, executable understanding of this market — from clinical pathways to procurement playbooks — the full report and our advisory services will provide the working analytics and bespoke recommendations needed to act confidently.

Contact PW Consulting to schedule a briefing or to license the full report and model. Our teams can also perform tailored scenario modeling or competitor due diligence to support M&A, new product launches, or payer contracting strategies.

— PW Consulting, Strategic Advisory & Industry Intelligence

For detailed analysis of this topic, please visit the official page:Cryoablation For Cancer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com