PW Consulting Forecast: Truck-Based Fuel Tankers Market to Expand at a 4.85% CAGR During 2026–2032

Other |

2026-07-02 12:41:06

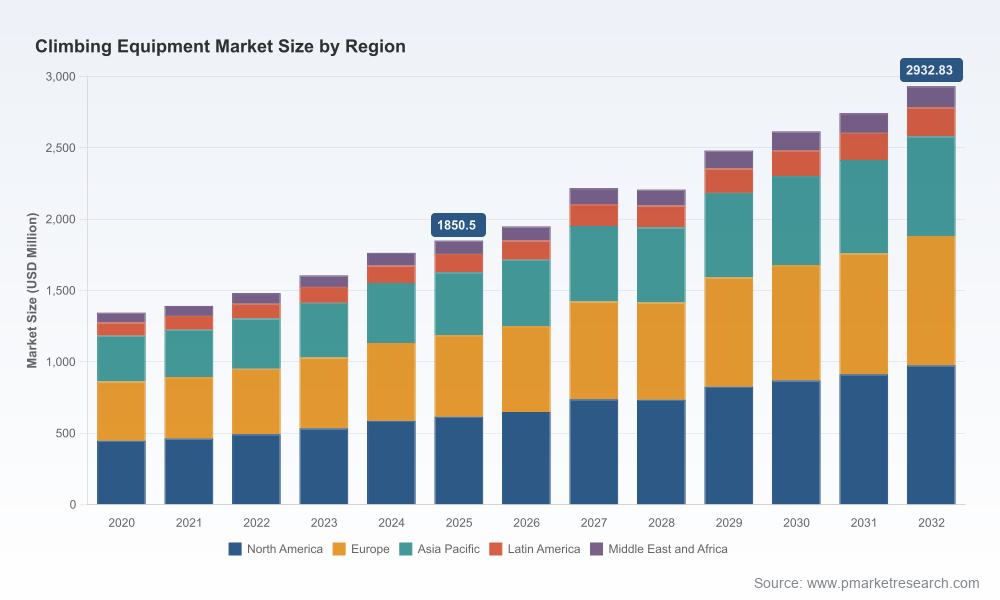

PW Consulting today publishes a forward-looking briefing drawn from our full Climbing Equipment Market report (base year 2025, forecast period 2026–2032). With the global market approaching roughly USD 1.85 billion in 2025 and projected to follow a compound annual growth rate (CAGR) of 6.8% across the forecast window, the sector is entering a phase shaped as much by regulatory recalibration and raw-material pressure as by product innovation and channel evolution. This press release outlines the report’s strategic value for 2026 decision-making, highlights the industry dynamics that will matter most to executives and investors, and previews the actionable tools included in the full study.

Climbing Equipment Market

Timing: 2026 is a pivot year. The market is expanding from a solid consumer base created by a wave of indoor gym openings and heightened outdoor participation; the pace and composition of that expansion will determine winners and losers across product categories and channels.

Climbing Equipment Market

Regulatory inflection: Recent safety standards revisions and high-profile recalls have raised the bar on compliance and quality management. Companies that move early to harden testing and traceability systems will protect brand equity and unlock premium pricing opportunities.

Climbing Equipment Market

Cost and supply volatility: Material and component cost shocks — including tariff changes affecting steel and aluminum, and notable price pressure for entry-level buyers between 2022–2024 — mean procurement strategy and product engineering will directly affect margin resilience.

Market structure: The sector remains moderately unconcentrated (CR3 ~22.4%; CR5 ~38.5%), which creates both competitive intensity at scale and room for focused consolidation or niche leadership by specialty brands.

Robust market sizing and scenario modelling — base-year calibration and three scenario tracks (baseline, upside, downside) that stress-test demand against policy, macro, and participation shocks.

Go-to-market playbooks for manufacturers and distributors — channel segmentation, wholesale vs direct-to-consumer tactics, pricing ladders, and SKU rationalization frameworks that preserve margin by design.

Regulatory and product-safety roadmaps — gap analyses against updated standards, recommended testing protocols, and a compliance investment calculator to assess cost of ownership for certification programs.

Supply-chain stress tests and sourcing blueprints — multi-sourcing scenarios, near-shoring impact assessments, and a raw-material sensitivity model tied to steel/aluminum tariff pathways and polymer price swings.

Competitive landscaping and strategic scorecards — comparative KPIs, innovation posture, channel strength, and M&A readiness indices for the leading manufacturers and agile challengers.

Operational playbook for recalls and brand remediation — communications templates, warranty strategies, and insurance considerations informed by recent industry cases.

Investor-facing diligence pack — valuation start points, margin improvement levers, and a list of prioritized M&A targets aligned to strategic themes.

The climbing equipment ecosystem blends legacy alpine specialists, vertically integrated technical brands, and smaller, highly innovative players. Across that landscape, distinct strategic archetypes are emerging:

Heritage technical manufacturers (safety and rope specialists): Firms with deep testing laboratories and long-standing rope and harness portfolios have a natural advantage as standards tighten. These brands are doubling down on certified performance and leveraging reputation to defend price points.

Premium apparel and system integrators: Brands known primarily for technical outerwear are migrating further into hard goods and harness design, aiming to offer complete technical systems for performance-driven climbers and guides.

Hardware innovators and niche fabricators: Smaller, agile companies focus on high-strength carabiners, cams and lightweight alpine solutions. Their engineering-led differentiation can command premium margins but is sensitive to component cost shocks.

Gym- and consumer-focused brands: Those oriented toward indoor climbing and bouldering prioritize accessible price/feature sets, route-setting tools, and training equipment. Gym partnerships and B2B sales remain a critical growth channel.

Notable market behaviors we document in the full report include product refresh cycles timed to seasonality, expanded accessory portfolios (training tools, crash protection, eco-friendly consumables), and strategic investments in testing and certification labs following recent safety announcements.

Standards updates: The UIAA’s recent revisions to multiple standards (including helmets and energy-absorbing systems) require immediate review of product specifications, testing regimens, and label claims. Firms should inventory impacted SKUs and prioritize re-certification for higher-risk lines.

Recall playbook: High-profile recalls over the last two years have demonstrated how quickly consumer trust can erode. A robust traceability program, transparent consumer outreach, and third-party validation are now table stakes.

Liability and insurance: Underwriters are increasingly pricing product-liability risk in this space; expect higher deductibles or restrictive terms unless brands can evidence enhanced QA and post-market surveillance.

Supply-side constraints are shaping product strategy in 2026. Tariff regimes enacted in 2025 have materially affected the cost base for metal-intensive components. Meanwhile, recorded increases in consumer-facing price points in prior seasons signal limited elasticity at the entry point — a dynamic requiring careful SKU-level margin management.

Procurement levers: Strategic multi-sourcing, locked-price contracts for key inputs, and selective vertical integration (e.g., rope extrusion, harness webbing) offer pathways to margin protection.

Design for cost: Material substitution, modularity in hardware, and prioritizing high-margin accessories reduce exposure while preserving brand performance claims.

Channel repricing: A mix of value-led entry items and premium, safety-certified SKUs allows brands to segment consumers by willingness-to-pay without diluting perceived quality.

Immediate (0–6 months): Conduct a standards-impact audit, map SKUs to regulatory exposure, and create a prioritized recertification plan. Establish recall-response protocols and update public warranty policies.

Short-term (6–18 months): Rework sourcing agreements to mitigate tariffs, pilot near-shore manufacturing for high-cost components, and launch targeted premium lines backed by third-party certification to recapture margin.

Medium-term (18–36 months): Invest in R&D for lightweight, recyclable materials; expand service offerings (training, inspection, certification); and explore bolt-on acquisitions to consolidate distribution or add differentiated hardware IP.

The market’s moderate concentration and segmented demand profile create multiple arbitrage opportunities. Strategic buyers should look for targets that offer:

Proprietary engineering or production capabilities that are difficult to replicate (e.g., rope extrusion, specialized metal forging).

Strong channel relationships with gym networks and B2B procurement teams, which accelerate wallet share and recurring revenue.

Brands with credible sustainability roadmaps and traceable supply chains — increasingly important in consumer preference and institutional procurement.

The accompanying report is designed as a decision-support toolkit for 2026 strategy. Subscribers will gain access to:

Interactive scenario dashboards that let teams model pricing, tariff and participation sensitivities against revenue and EBITDA outcomes.

Company scorecards and a prioritized M&A shortlist with commercial and operational due diligence checklists.

Regulatory compliance templates, supplier audit guides, and a recall-communications playbook to reduce execution risk.

The climbing equipment market is growing steadily and predictably at the aggregate level, but beneath that headline growth lies a bifurcation: value-focused channels wrestle with cost inflation, while performance and safety-led segments reward technical excellence and certification investments. For manufacturers, distributors and investors preparing plans for 2026, the choice is clear — prioritize compliance, secure your supply chain, and double down on product and channel strategies that preserve margin while protecting brand integrity.

To access the full executive summary, methodology, interactive models, and the complete set of strategic recommendations, please visit our report page or contact PW Consulting’s Climbing Equipment practice for a briefing.

For detailed analysis of this topic, please visit the official page:Climbing Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com