Recombinant Collagen Market 2026: Strategic Imperatives from PW Consulting’s New Industry Insight

Executive preview

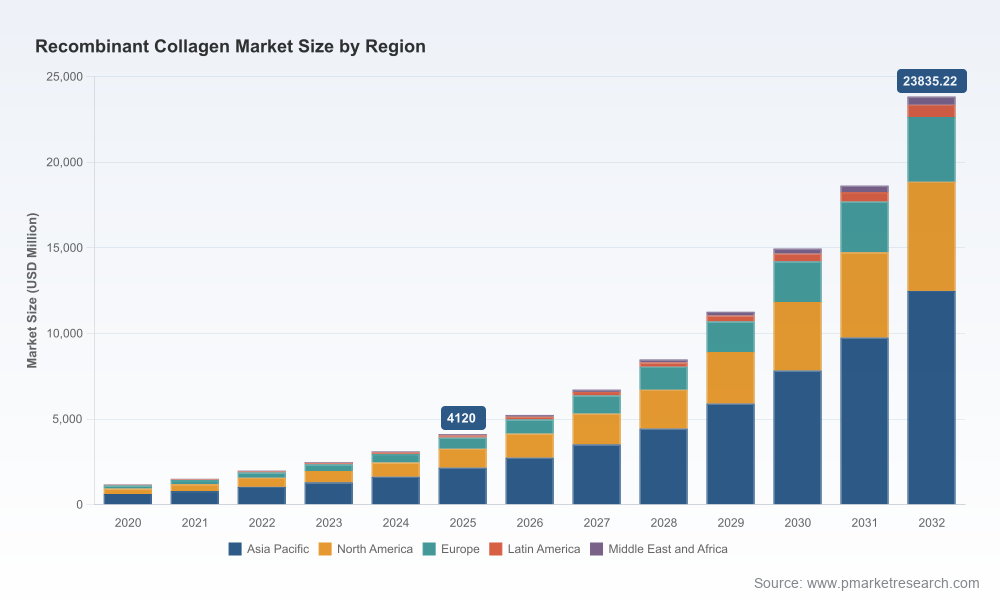

PW Consulting’s latest market study on recombinant collagen delivers a compact, decision-ready intelligence package designed to inform corporate strategy in 2026. Anchored on a 2025 base year and a detailed forecast for 2026–2032, the study quantifies a market that expanded rapidly in the first half of the decade—rising from approximately USD 1.18 billion in 2020 to about USD 4.12 billion in 2025—and that we project to exceed USD 23.8 billion by 2032 under a compound annual growth rate (CAGR) of 28.5% across the forecast window. These headline numbers capture the scale and velocity of change; our report translates them into practical actions for R&D, manufacturing, commercial, and M&A teams.

Recombinant Collagen Market

Why 2026 is a strategic inflection point

2026 is not just another year on the calendar: it marks the transition from early-adopter commercialization to broad-based industrialization for recombinant collagen. Several converging forces—regulatory recognitions, clinical-grade product launches, ton-scale production facilities coming online, and breakthroughs in bioprinting and fiber-spinning—mean that incumbent players and newcomers alike must make hard choices about where to compete, how to secure supply, and how to accelerate product-market fit.

Recombinant Collagen Market

Our forecast model quantifies the upside available to firms that execute on one or more of three value plays: platform therapeutics and implantables, aesthetic and functional skincare, and industrial-scale biomaterials (e.g., fibers and dressings). The report prioritizes these plays by commercial readiness, margin profile, and capital intensity, giving executives a short-list of immediate bets versus longer-horizon options.

Recombinant Collagen Market

What the PW Consulting report delivers — operationally focused

- Proprietary market model: Scenario-driven revenue projections (2026–2032), sensitivity analysis around price erosion, adoption curves, and reimbursement timelines.

- Go-to-market playbooks: Action templates for licensing, OEM partnerships, and vertically integrated strategies, tailored for medtech, cosmetics, and research-supply companies.

- Technology and cost maps: Comparative analysis of expression systems, downstream purification workflows, and unit economics under varied scales.

- Regulatory and clinical pathway grid: Country-specific timelines, key evidentiary thresholds, and fast-track mechanisms relevant to implantables, injectables, and device-adjacent products.

- Supply-chain risk dashboard: Concentration heat maps, alternative sourcing scenarios, and tactical mitigation plans for single-point failures.

- M&A and partnership playbook: Valuation heuristics, earn-out structures, and integration checklists for acquiring process-enabled IP versus market-ready products.

- Investor-ready exhibits: One-page strategy briefs and investor memos that translate technical milestones into financing tranches and valuations.

Trailer principle: what we intentionally withhold here

In line with the “trailer” approach, this release demonstrates the depth and practical orientation of our study while intentionally omitting granular subsegment share tables, region-by-region revenue splits, and detailed pricing trajectories. These high-value annexes—critical for transaction diligence and tactical procurement—are available within the full report hosted on our site.

Competitive landscape: leaders, challengers, and new models

The recombinant collagen ecosystem is now varied and strategically distinct. Our competitive analysis divides the landscape into three archetypes: industrial fermentation platforms, biotech innovators focused on product differentiation (bioinks, ingestibles, and engineered polypeptides), and regionally dominant manufacturers pursuing scale and vertical integration.

- Platform and quality champions: Companies such as Evonik Industries (Essen, Germany) have moved to supply clinical-grade recombinant collagen-like platforms suitable for medical-device development and bioprinting applications—signaling a shift toward GMP-compliant offerings that enable clinical programs.

- Biotech differentiators: CollPlant Biotechnologies (Rehovot, Israel) has demonstrated notable advances in plant-based rhCollagen bioinks and preclinical milestones in full-sized implant bioprinting; Geltor (United States) and Jellatech (United States) exemplify firms pairing synthetic biology with product-led differentiation in ingestibles, skincare, and biopharma applications.

- Scale and vertical integrators: Several large manufacturers, particularly in Asia, are capitalizing on early mass-production runs and close ties to contract-manufacturing and cosmetic brands. These players are moving quickly from raw-material supply toward finished-goods collaboration models.

Recent, market-shaping developments (selected)

- Sep 2025 — Evonik launched a clinical-grade recombinant collagen-like platform suitable for clinical trials and medical device development, reducing a common bottleneck for firms seeking GMP inputs.

- May–Oct 2025 — CollPlant disclosed preclinical success in 3D bioprinting of large implants and subsequently reported head-to-head bioink study results that bolster its competitive positioning in regenerative and aesthetic medicine.

- Mar 2026 — CollPlant received a Nasdaq compliance-period extension while advancing its platform, an important governance reminder for investors following public biotech trajectories.

Production, process, and regulation: the underpinning dynamics

Production science continues to evolve quickly. Recombinant collagen manufacturing is dominated by microbial fermentation, with widely reported expression-performance differentials between hosts—laboratory and pilot studies cite expression yields up to ~3.02 g/L in Escherichia coli and up to ~10.3 g/L in optimized Pichia pastoris strains. These yield differentials materially affect capex payback and cost per gram at scale.

Regulatory signals are equally consequential. Notable approvals and certifications—such as the first Class III implantable recombinant-collagen medical device authorization in China and reported FDA certification of a 100% human-sequence-identical recombinant product—create precedents that shorten commercialization timelines for comparable products. Meanwhile, industrial-scale manufacturing facilities (including sites with multi-ton annual capacities) and public funding for fiber-spinning collaborations indicate a near-term shift from bench to bulk.

Strategic implications for 2026 planning

- Portfolio prioritization: Firms must decide whether to invest in platform-grade manufacturing, product development (aesthetic/therapeutic), or commercial partnerships. The report’s scenario models highlight break-even horizons under multiple adoption curves.

- Supply-security as a competitive moat: Given concentration and capital intensity in manufacturing, securing long-term offtake or joint-venture access to GMP-capable collagen supply is now a defensive necessity for downstream companies.

- Regulatory-first product design: Product specifications should be engineered to satisfy higher evidentiary bars up front, reducing time-to-market risk and avoiding costly reformulations after regulatory feedback.

- R&D focus: Prioritize host-strain optimization, downstream purification cost reduction, and formulation strategies that enable premium positioning (e.g., clinical-grade bioinks, implantable fibers).

- M&A and partnerships: Tactical acquisitions of process IP, small-scale GMP facilities, or exclusive supply agreements are likely to deliver faster route-to-market than greenfield buildouts for many firms.

How executive teams should use this study in 2026

- Use the market model to stress-test investment cases over conservative and aggressive adoption scenarios.

- Leverage our regulatory and clinical grid to set milestone-based funding tranches and to align C-suite timelines with regulatory submission windows.

- Run a six-week rapid diligence using our supplier risk dashboard to determine whether to lock multi-year supply contracts, pursue capex, or pursue strategic JV partners.

- Apply the M&A playbook to value target companies by isolating process-enabled value from market-enabled value—critical for negotiating earn-outs and integration terms.

Concluding note and next steps

The recombinant collagen market presents a rare combination of rapid growth and technical complexity. With a base-year vantage of 2025 and a forecast that projects a multi-billion-dollar opportunity through 2032 at a 28.5% CAGR, senior executives must treat 2026 as the year for decisive structural moves: secure supply, hedge regulatory risk, and prioritize product profiles that can unlock premium channels. PW Consulting’s full report provides the granular subsegment data, supplier scorecards, and financial models required to operationalize these strategies. For access to the complete annexes and to commission a bespoke briefing for your executive team, please visit our official report page.

For detailed analysis of this topic, please visit the official page:Recombinant Collagen Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com