Fertility ELISA Test Kit Market: Strategic Imperatives for 2026 — PW Consulting Preview

Executive summary

The Fertility ELISA Test Kit market is entering a phase of sustained, predictable growth driven by demographic shifts, wider access to assisted reproductive technologies, and ongoing improvements in assay performance and regulatory clarity. Our newest market study (base year 2025, historical window 2020–2025, forecast 2026–2032) quantifies this expansion and translates it into tangible strategic choices for vendors, laboratories, investors, and healthcare providers. The market in 2025 stands at USD 952.47 Million (revenue, USD Million), and under the baseline scenario PW Consulting models a compound annual growth rate (CAGR) of 6.12% over the 2026–2032 forecast interval, reaching a materially larger market by 2032. This preview highlights the report’s strategic value for decisions you will make in 2026 while deliberately withholding detailed segment-level figures — the full dataset and granular splits are available in the published report.

Fertility Elisa Test Kit Market

Market trajectory and what it means for decision-makers

From 2020 through 2025 the market has demonstrated resilience, absorbing cyclical pressure and benefiting from technology-driven enhancements in sensitivity, specificity and throughput. The modeled 6.12% CAGR to 2032 reflects a market that will reward suppliers who can simultaneously deliver regulatory-compliant products, robust quality systems, and clear clinical value propositions.

Fertility Elisa Test Kit Market

- For product leaders — a steady growth profile justifies prioritized investment in mid-life product upgrades (e.g., improved antibodies, multiplex compatibility) and in companion digital offerings that reduce lab turnaround time and improve interpretability for clinicians.

- For commercial teams — the growth runway supports diversified go-to-market models: direct supply to fertility clinics, OEM partnerships with larger in vitro diagnostic (IVD) platforms, and targeted expansion into high-volume reference laboratories.

- For investors and M&A strategists — the market exhibits moderate concentration among leading players but remains open to consolidation and bolt-on acquisitions that add assay breadth, geographic reach, or manufacturing scale.

What the PW Consulting report delivers (practical content)

This study was designed with actionability as the primary metric. It combines quantitative forecasting with practical playbooks so readers can convert insight into execution during 2026:

Fertility Elisa Test Kit Market

- Proprietary forecast model calibrated to historical shipment and revenue trends (2020–2025) and scenario-tested through 2032.

- Total market size and growth drivers, plus demand-supply overlays that highlight inflection points for pricing and capacity planning.

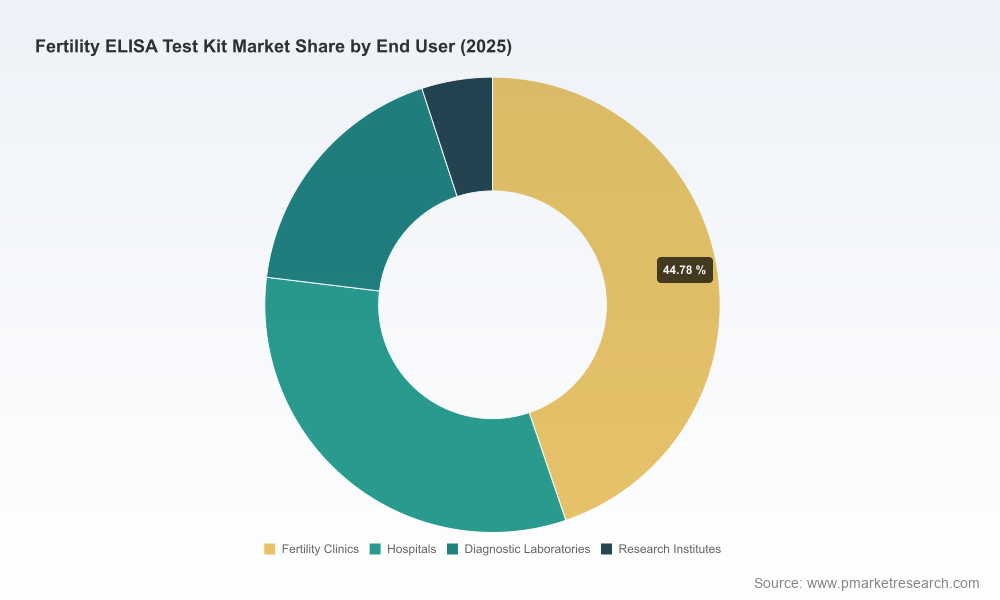

- Segment architecture (by region, product type and end user) with strategic implications for portfolio prioritization — note: the preview omits segment line-item values; the full report contains the complete split tables and regional curves.

- Regulatory pathway maps and a stepwise checklist for CE marking and U.S. market entry, aligned with ISO 13485 quality requirements and recent FDA precedents for certain fertility-related ELISA indications.

- Commercial benchmark and price-mix sensitivity analyses, including win-loss archetypes for clinical laboratories and fertility clinics.

- Operational playbooks for supply chain resilience, contract manufacturing evaluations, and GMP/ISO conformance audits.

- Decision tools including ROI calculators for new product introductions and a data collection blueprint for building real-world evidence to support payers and clinicians.

Competitive landscape: who matters and why

The competitive field is anchored by several specialist players that combine assay know-how with regulatory and distribution capabilities. Our report provides comparative supplier scorecards and strategic positioning maps; below we summarize the profile strengths of core industry participants covered in the study.

- Ansh Labs (Webster, TX) — recognized for its focused immunoassay expertise in reproductive markers. Notable strengths include a clinically validated AMH ELISA with CE-marked variants and proprietary monoclonal antibodies targeted to clinically relevant AMH isoforms. This depth in antibody science translates into a strong clinical story for ovarian reserve assessment and IVF outcome support.

- DRG International (Springfield, NJ) — a diversified ELISA manufacturer with a broad hormone assay menu. Competitive advantage lies in established assay platforms (e.g., estradiol and steroid panels) and a history of supplying assays used in ovulation induction monitoring and endocrine evaluations.

- Monobind (Lake Forest, CA) — offers a wide IVD ELISA portfolio that includes FSH, LH, prolactin and beta-hCG. Their AccuBind kits position them as a turnkey supplier for labs that require validated kits across endocrine and reproductive panels, supported by a strong distribution footprint.

- Sure Bio‑Tech (USA) — an export-oriented supplier with manufacturing and regulatory emphasis on GMP/ISO 13485 and CE compliance. The company’s model focuses on scalable production and affordability for international markets while maintaining a product range that addresses core fertility testing needs (AMH, LH, FSH, prolactin).

Market concentration metrics in our analysis indicate partial clustering among the top vendors, creating both competitive pressure and strategic acquisition opportunities. In particular, the top three to five firms account for a meaningful portion of industry revenue (concentration metrics are included in the full report), but substantial niche and regional gaps remain for agile entrants and differentiated technologies.

Regulatory, quality and reimbursement dynamics

Several structural factors shape the short- to mid-term market environment:

- Regulatory pathways — ELISA-based fertility assays, especially those intended to inform clinical decisions (e.g., menopausal status, ovarian reserve), are subject to formal regulatory scrutiny. In the U.S., certain intended uses have historically required FDA 510(k) clearance or de novo authorization. In Europe, CE marking remains a primary market access route, with notified body engagement for devices under the IVD regulation framework. Our report provides a decision tree mapping regulatory risk to commercialization timelines.

- Quality systems — ISO 13485 conformance and GMP processes are not optional for suppliers targeting clinical laboratory and hospital channels. Contract manufacturers and suppliers without documented quality systems face material barriers to scale.

- Reimbursement contours — fertility-related hormone assays typically fall under standard clinical laboratory coding and payer policies rather than dedicated fertility codes. This coding environment places a premium on generating cost-effectiveness and clinical utility evidence to secure favorable lab reimbursement and hospital adoption.

Near-term opportunities and risks

For 2026 decision cycles, PW Consulting highlights a set of prioritized opportunities and key risks:

- Opportunity: Evidence-led differentiation. Vendors that invest in prospective performance studies and publish clinical utility data for specific indications (e.g., IVF staging, PCOS stratification) will unlock premium pricing and payer recognition.

- Opportunity: Platform interoperability. Kits designed for compatibility with high-throughput analyzers and laboratory information systems reduce adoption friction in centralized labs.

- Risk: Regulatory misalignment. Mis-specifying intended use claims can materially delay market entry and increase development costs; early regulatory strategy de-risks time-to-revenue.

- Risk: Supply concentration. Dependence on single-source critical reagents or single-region manufacturing leaves suppliers exposed to geopolitical and logistic disruptions.

Actionable strategic moves for 2026

Based on scenario modeling and supplier interviews, PW Consulting recommends a set of practical actions for organizations planning their 2026 roadmaps:

- Prioritize compliance upgrades — align documentation, supplier audits and design controls to ISO 13485 standards now to avoid delayed market access windows.

- Invest selectively in clinical studies — target RCT or real-world cohorts where improved assay performance would demonstrably influence clinical decisions (IVF protocols, ovarian reserve counseling).

- Adopt hybrid commercial channels — balance direct engagement with fertility clinics and strategic partnerships with reference labs to optimize coverage while managing sales expense.

- Evaluate M&A as a speed-to-market tactic — acquire complementary assay portfolios or regional distribution networks rather than duplicating R&D effort.

- Boost supply chain visibility — dual-source critical reagents, regionalize manufacturing capacity, and stress-test packaging/logistics for export markets.

- Build payer dossiers early — use health economic models and local cost data to support reimbursement conversations in priority markets.

Why PW Consulting’s Fertility ELISA report is mission-critical for 2026 planning

Leadership teams making 2026 investment and market-entry decisions need more than broad trends; they need tools that translate growth projections into operational choices. Our report delivers:

- Validated top-line forecasts (base year 2025) and scenario-tested outcomes through 2032 to stress-test capital allocation decisions;

- Competitive benchmarking and supplier scorecards to prioritize partners or targets for acquisition;

- Regulatory playbooks and reimbursement templates that compress time-to-market and accelerate commercial adoption;

- Action-oriented ROI models and implementation checklists tailored to product, geography and buyer-type.

Next steps

This industry preview illustrates the strategic lens and operational depth of the full Fertility ELISA Test Kit market study while intentionally withholding the granular segment-level tables that are essential for executable plans. To access the complete dataset — including regional, product-type and end-user splits, supplier market shares, scenario outputs, and the downloadable decision tools — please consult the full report available through PW Consulting’s research portal. Clients and potential partners may also request a bespoke briefing to translate findings into a customized 2026 action plan.

For detailed analysis of this topic, please visit the official page:Fertility Elisa Test Kit Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com