Fire Retardant Additives Market 2026 Strategic Brief: Turning Compliance and Commodity Volatility into Competitive Advantage

PW Consulting’s latest market study on Fire Retardant Additives distills seven years of market evolution and a seven‑year forecast into an executive playbook for 2026 decision‑makers. The global market, which crossed a USD 9.45 billion revenue threshold in 2025, is projected to expand at a 4.95% compound annual growth rate through the 2026–2032 forecast window, moving toward a mid‑double‑digit billion dollar valuation by 2032. This growth is neither uniform nor frictionless: regulatory shifts, raw‑material shocks and fast‑moving end‑market requirements are recalibrating value pools across chemistries, formulations and channels.

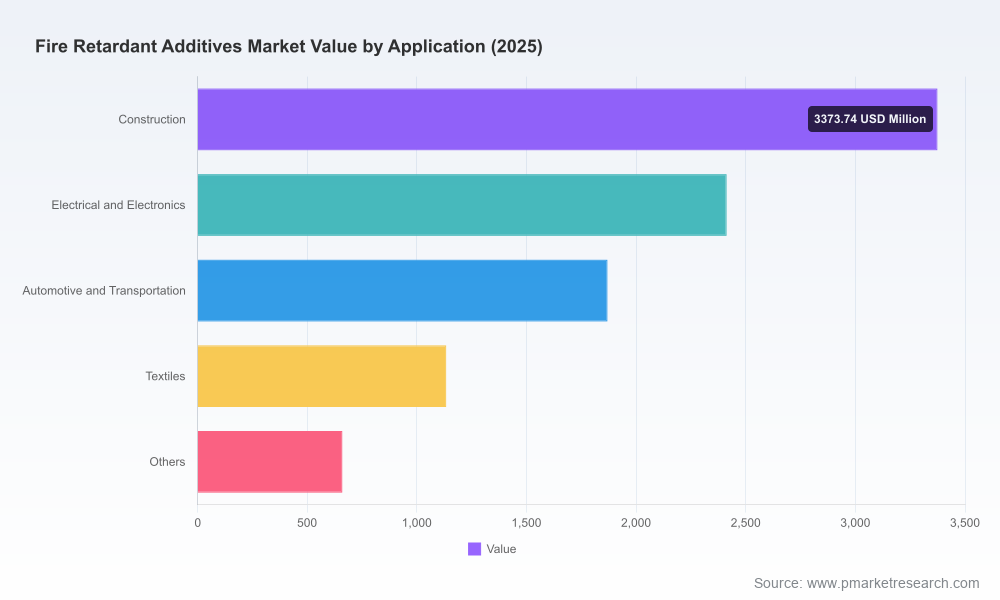

Fire Retardant Additives Market

Why this brief matters for 2026 strategy

- Translating macro momentum into near‑term cash: Our modelling shows that moderated market expansion masks attractive pockets of margin improvement driven by premium halogen‑free solutions and polymer‑compatible oligomeric phosphorus technologies.

- Risk‑weighted planning for supply and pricing: Raw‑material volatility (notably alumina trihydrate and bromine benchmarks) has compressed spot availability in 2024–25. Executives need scenario templates to quantify price pass‑through, hedging and contract re‑negotiation levers in 2026.

- Compliance as a market‑making force: Restrictive regulatory action in major jurisdictions is accelerating substitution away from legacy halogenated chemistries. This creates both disruption risk for incumbent portfolios and first‑mover advantages for compliant, high‑performance alternatives.

What’s inside the report — actionable, not academic

- Proprietary market model: Layered historicals (2020–2025) and forward scenarios (2026–2032) with sensitivity sliders for raw material cost, regulatory tightening and end‑market demand elasticity. The model is delivered in an interactive workbook so teams can run bespoke what‑ifs.

- Regulatory & standards playbook: A consolidated matrix detailing current and as‑anticipated restrictions (EU REACH updates, California and U.S. label regimes, key import tariff policies) plus compliance roadmaps for formulation, testing and documentation that reduce time‑to‑market for alternatives.

- Raw‑material stress tests: Scenario analyses for ATH, bromine and key co‑agents showing margin impact, potential supplier concentration risks, and prioritized sourcing actions (forward buys, regional re‑routing, strategic tolling partnerships).

- Technology and substitution map: Comparative performance and cost curves for aluminum trihydrate, brominated systems, antimony synergists, phosphorus‑based oligomers and emerging inorganic blends; recommended substitution pathways by compound class and end‑use friction points.

- Commercial playbooks: Go‑to‑market templates for price architecture, channel segmentation, and technical service value propositions targeted to construction, electronics, automotive and textile OEMs.

- Competitive intelligence & M&A scanner: Profiles of leading suppliers with strengths/weakness analysis, capability gaps and a scored filter to identify bolt‑on M&A targets or JV partners that accelerate access to halogen‑free IP or regional capacity.

- Investment roadmaps: CapEx prioritization guidance for capacity expansions, pilot lines for oligomeric phosphorus chemistries, and retrofits to meet emerging green‑chemistry specifications.

Market structure and competitive dynamics — what 2026 leaders must internalize

The market sits between fragmented and consolidated. The top three players collectively hold a material share of the landscape, while the top five extend that concentration further. This structure creates asymmetric opportunities: scale incumbents can leverage global distribution and regulatory expertise, while nimbler specialists can win on formulation innovation and rapid certification.

Fire Retardant Additives Market

- Clariant AG — Specialist in phosphorus‑based and halogen‑free systems. Recent product introductions show a deliberate pivot to polyolefin‑compatible halogen‑free grades, underlining an execution playbook built around differentiated formulations and sustainability claims.

- BASF SE — Strong in engineered plastics and intumescent coatings. BASF’s portfolio depth and application development capabilities make it a reference partner for OEMs seeking system‑level flame performance proofs.

- Lanxess AG — Focused offerings for flexible foams and polyurethanes. Their phosphate esters and polymeric additives address specific foam processing constraints, creating stickier customer relationships in foam‑intensive applications.

- Albemarle Corporation — Legacy strength in bromine‑based chemistries, particularly for electronics. Their market position faces secular pressure from decarbonization and circularity trends but remains relevant where performance‑cost tradeoffs favor brominated solutions.

- ICL Group Ltd — Expanding phosphorus capacity with a go‑to market emphasis on wire & cable and textile segments. Capacity moves underscore management’s view that phosphorus chemistries will take share in regulated markets.

- Huber Engineered Materials, Rio Tinto — Critical suppliers for mineral fillers (ATH, MDH) with differentiated supply chains. Price and availability of these commodities will continue to set commercial rhythms.

- FRX Polymers, Thor Specialties, Dow Inc. — Smaller and focused players advancing oligomeric phosphorus polymers, niche halogenated formulations and synergists respectively. These firms are potential partners or acquisition targets for incumbents looking to accelerate portfolio transition.

Industry dynamics shaping 2026 tactical choices

- Raw‑material dislocations: Recent spot price pressures for ATH and bromine have materially increased short‑term cost volatility. Procurement strategies in 2026 must go beyond supplier diversity to include tolling, long‑term purchase agreements and formula redesigns that reduce mineral loadings.

- Regulatory tightening: Measures restricting legacy brominated and certain antimony chemistries in core markets have shortened the window for incremental investments in those chemistries. Firms should prioritize dual‑track roadmaps that protect current revenues while accelerating validated alternatives.

- Trade and tariff realities: Recent tariff actions on imports from specific origins call for near‑term operational responses—regionalized inventory staging, re‑routing and local production partnerships—that preserve competitiveness without sacrificing margin.

- End‑market differentiation: Electronics and automotive customers are converging on stricter fire performance and low‑smoke, low‑toxicity requirements. Winning suppliers will combine application engineering, validated life‑cycle claims and logistical reliability.

Practical strategic moves for 2026

- Prioritize portfolio triage: Segment product lines into ‘‘protect, pivot, divest’’ buckets using our scoring algorithm that weighs regulatory exposure, margin durability and replacement cost.

- Accelerate certified halogen‑free offerings: Invest in pilot lines and third‑party testing to reduce certification cycle times and create defensible claims for OEMs making sustainability commitments.

- Lock supply lines for critical minerals: Negotiate multi‑year contracts with staged pricing and flexibility clauses; explore vertical partnerships or minority equity stakes in upstream specialists.

- Deploy differentiated commercial models: Bundle formulation expertise, on‑site technical support, and performance guarantees for strategic accounts to move competition away from price alone.

- Use M&A and licensing with discipline: Screen targets that either close gaps in halogen‑free IP, add scale in strategic geographies, or provide technology platforms that shorten time‑to‑market for cleaner chemistries.

- Adopt a modular R&D cadence: Mix fast‑follow product extensions with longer‑term platform bets (e.g., oligomeric phosphorus, polymeric retardants) and stage investments against regulatory milestones.

What PW Consulting recommends for 90‑day priorities

- Run a portfolio stress test with our interactive model to quantify P&L sensitivity to ATH and bromine price shocks and to potential phased regulatory bans.

- Open supplier contingency dialogues in the highest‑risk commodity lines and pilot at least one alternative sourcing route (regional supplier or toll processor).

- Initiate two targeted technical partnerships: one with an OEM to co‑develop application‑specific grades and one with a smaller chemistry innovator to secure early access to halogen‑free IP.

- Calibrate commercial messaging to emphasize validated performance and compliance — prepare sample dossiers and third‑party test reports for top 10 accounts.

PW Consulting’s Fire Retardant Additives Market report blends granular industry knowledge with executable strategic tools to inform capital allocation, product roadmaps and commercial execution in 2026. We intentionally preserve the most decision‑critical segmentation tables, regional demand overlays and company‑by‑company revenue breakdowns for the full report to ensure clients have the exclusive, high‑fidelity inputs needed to act with conviction.

Fire Retardant Additives Market

To access the complete dataset, interactive models and supplier scorecards that underpin these recommendations, visit the PW Consulting report portal or contact our industry team to request a tailored briefing.

For detailed analysis of this topic, please visit the official page:Fire Retardant Additives Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com