Off Road Fuel Tank Market 2026: Strategic Insights to Inform Executive Decisions

Executive summary

PW Consulting’s latest Off Road Fuel Tank Market report provides a focused operational playbook for senior executives, corporate development teams, procurement leaders, and product strategists preparing for 2026 and beyond. Built on a 2020–2025 historical base and a 2026–2032 forecast horizon, the study shows the market expanding at a steady compound annual growth rate (CAGR) of 5.48%. In monetary terms, the industry stood at approximately USD 2.20 billion in the base year and is modelled to grow toward a multi‑billion‑dollar opportunity by 2032 under the central-case scenario. The report combines quantitative forecasting with granular, transaction‑ready analysis designed to convert market intelligence into immediate commercial action.

Off Road Fuel Tank Market

Why this report matters for 2026 decision cycles

- Translate macro growth into executable targets: a clear line-of-sight from industry expansion to achievable revenue and margin objectives across product, aftermarket and OEM channels.

- Mitigate supply risk amid volatile raw materials: scenario models and procurement playbooks that preserve margin under raw-material shocks and inflation.

- Regulatory compliance as a source of competitive advantage: engineering and product roadmaps that anticipate evaporative emissions and heavy‑duty GHG requirements.

- Prioritize capital deployment: capital allocation frameworks and 100‑day commercialization plans for product line expansions, facility footprint changes, and bolt‑on M&A.

Key market dynamics shaping 2026

Three structural forces will define near‑term outcomes and should be central to any 2026 strategy:

Off Road Fuel Tank Market

- Raw‑material volatility and input cost pass‑through. Aluminum mill shapes and steel mill product prices experienced significant increases in the most recent 12‑month window, and HDPE pricing movements (notably Q2 2025 levels) are influencing cost competitiveness for plastic tank production. Our cost‑model scenarios quantify the profit impact of persistent price elevation versus rapid reversion, enabling procurement and pricing teams to select hedging and contract structures that protect margin.

- Regulatory tightening on evaporative emissions and heavy‑duty GHG standards. Ongoing EPA and CARB enforcement around permeation and evaporative emissions for small off‑road equipment (SORE), together with Heavy‑Duty Vehicle Phase 3 rules that extend into off‑highway contexts, materially affect material choices, system architecture, and testing overhead. The rapid adoption of multi‑layer plastic constructions is already visible; our regulatory matrix maps time‑to‑compliance and cost of change for key product lines.

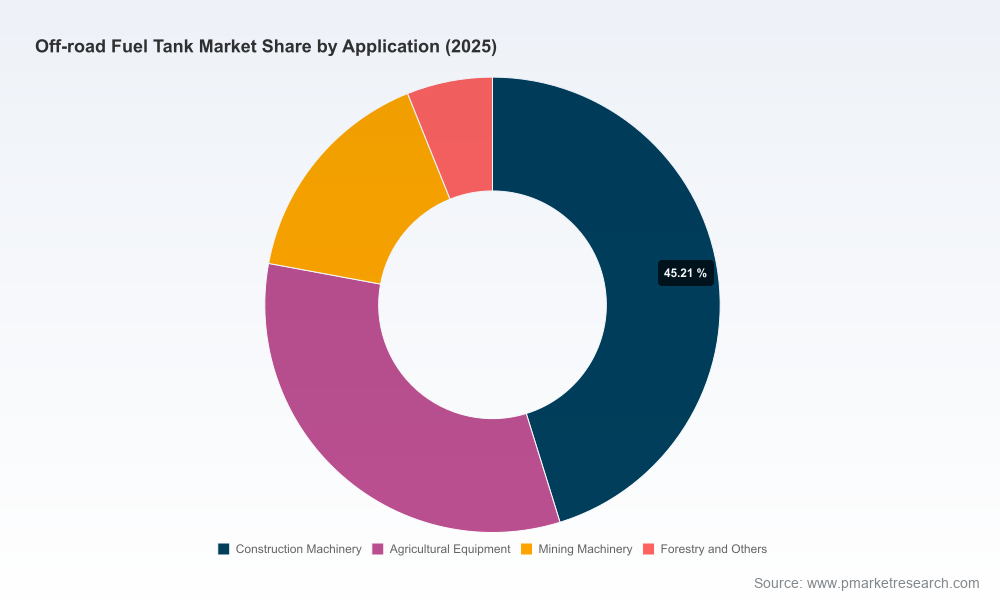

- Technology and channel bifurcation. The market is splitting into higher‑value engineered solutions (multi‑layer blow‑molded HDPE, specialized stainless/aluminum fabrications, and safety‑certified racing bladders) and volume commodity tanks. Aftermarket and auxiliary solutions for extended range remain a resilient revenue pool as end customers prioritize uptime and operational reach in off‑road applications.

Competitive landscape — what executives should know

The market is characterized by a mix of specialized metal fabricators, high‑volume blow‑molders, aftermarket specialists, and custom manufacturers serving racing and extreme‑use segments. Overall concentration indicates a moderately fragmented market: the top three players collectively account for roughly 34.3% market share and the top five for about 48.9%, leaving meaningful room for scale‑driven consolidation and niche leadership plays.

Off Road Fuel Tank Market

- Metal and fabricators (IFH Group; Standard Technologies): These firms have deep capabilities in custom steel, stainless, and aluminum tanks, and are positioned to serve OEMs in heavy construction, military and specialty vehicles. Their competitive edge is material expertise, high‑volume welding and forming capacity, and relations with OEM engineering teams for integration in heavy‑duty platforms.

- High‑volume plastic specialists (Agri‑Industrial Plastics; Elkamet): Industry leaders in multi‑layer HDPE and blow‑molding bring scale, permeation‑compliant designs, and cost advantages for lower‑weight applications. Their production footprints and regulatory compliance experience make them first movers for CARB/EPA permeation requirements.

- Aftermarket and auxiliary system players (Transfer Flow; TITAN Fuel Tanks): Focused on extended‑range, replacement and adventure/off‑grid use, these suppliers monetize higher unit margins through product differentiation, brand recognition among end users, and direct‑to‑end‑user channels.

- Large‑capacity and specialty providers (Niece Equipment; Extreme Tanks; Harmon Racing Cells): These players serve mining, large construction, racing and specialized industrial applications with bespoke tanks, high‑capacity fuel beds and FIA‑rated safety bladders. Their value propositions emphasize durability, serviceability and field support.

Strategically, incumbents with cross‑material capability and OEM relationships can pursue adjacency plays into aftermarket and larger modular systems. Smaller specialists can remain attractive acquisition targets for firms seeking to accelerate material‑technology adoption or to add compliance capabilities.

What the PW Consulting report contains — practical deliverables

We designed the report as a toolset, not just a narrative. Highlights of the deliverables (high‑level descriptions; full segment tables and proprietary unit economics are reserved for report subscribers) include:

- Comprehensive market sizing and a 2026–2032 forecast built on bottom‑up shipment and ASP models, stress‑tested across three macroeconomic scenarios.

- Regulatory impact matrix mapping EPA/CARB permeation rules and Heavy‑Duty Phase 3 requirements to product redesign timelines and estimated compliance costs.

- Raw‑material sensitivity and procurement playbooks, including indexation templates, rolling‑hedge approaches and supplier dual‑sourcing decision criteria tied to cost‑to‑serve outcomes.

- Competitive benchmarking dossiers (detailed profiles, capability maps, estimated capacity windows and likely strategic intent) for the leading suppliers across metal, plastic and aftermarket verticals.

- Go‑to‑market modules and a 100‑day action plan for new product launches, aftermarket channel acceleration, and low‑cost manufacturing footprint shifts.

- M&A screening tool with rule‑of‑thumb valuation bands, integration risk checklists, and a shortlist of opportunistic target archetypes tuned to CR3/CR5 expansion strategies.

- Executive‑ready slide briefings and an interactive Excel model that allows internal teams to run “what‑if” scenarios for raw‑material spikes, price compression and accelerated regulatory timelines.

Priority strategic recommendations for 2026

- Lock in HDPE supply and technical partnerships. With HDPE price dynamics and new capacity changes influencing buyer conditions, secure multi‑year offtakes with flexible indexation tied to polymer price benchmarks to stabilize manufacturing costs.

- Accelerate multi‑layer and low‑permeation R&D. Invest in engineering and testing capability now to convert regulatory compliance into a product premium; early adopters capture aftermarket share and OEM specification advantages.

- Revisit metal sourcing and fabrication economics. Aluminum and steel price inflation makes re‑engineering for material efficiency and hybrid material solutions a near‑term priority; consider price‑linked supplier contracts and in‑house forming where scale justifies.

- Monetize aftermarket and auxiliary segments. Design modular, backward‑compatible auxiliary tanks and refueling systems for the growing field service and exploration markets—these products show resilience to OEM cycle volatility.

- Use targeted M&A to close capability gaps. Pursue bolt‑ons that bring permeation testing, multi‑layer molding, or large‑capacity fuel bed expertise to compress time‑to‑market and lift overall CR metrics.

- Embed regulatory scenario planning into product roadmaps. Create an early‑warning dashboard for regulatory milestones and align compliance investments with a staged revenue capture model to avoid costly late redesigns.

Conclusion — make 2026 a year of advantage, not reaction

The Off Road Fuel Tank market presents a clearly expanding opportunity for firms that can align material strategy, regulatory readiness, and targeted go‑to‑market plays. With the market growing from its 2025 base toward multi‑billion dollar outcomes by 2032 at a projected 5.48% CAGR, executives face a binary choice: act now to lock in supply, capability and regulatory competence—or accept that competitors will capture the margin and specification premium that comes with early compliance and scalable production.

PW Consulting’s report is structured to deliver the tactical and strategic inputs needed to make those decisions in 2026. For access to the complete segment breakouts, proprietary unit economics, company scorecards, and the downloadable scenario model, please visit the report page or contact PW Consulting’s industry practice to request an executive briefing and demo of the analytical suite.

For detailed analysis of this topic, please visit the official page:Off Road Fuel Tank Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com