Global Vegan Rice Cake No Artificial Color Market Growing at 5.9% CAGR Through 2034

Other |

2026-06-15 12:04:37

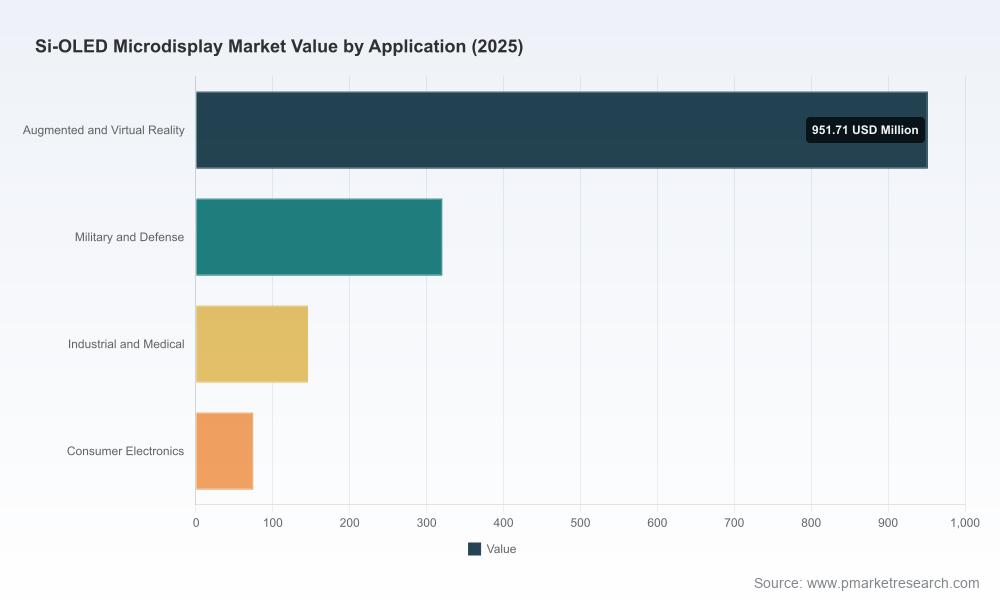

PW Consulting’s latest market research on Silicon‑backed OLED (Si‑OLED / OLEDoS) microdisplays illuminates a market on a steep growth trajectory, driven by near‑eye computing, defense modernization, and new industrial and medical form factors. The global Si‑OLED microdisplay market—which we modelled comprehensively across 2020–2025 and through a 2026–2032 forecast horizon—is expanding at a multi‑year compound annual growth rate (CAGR) of 29.85%. Aggregate market value has moved from the low hundreds of millions in 2020 to a materially larger industry by 2025, and we project near‑term scale inflection in 2026 as new capacity and procurement cycles ramp. This briefing synthesizes the strategic implications for executives and investors considering decisions in 2026; the full report (linked at the end) contains the detailed segment, regional, and supplier economics that underlie these conclusions.

Si Oled Microdisplay Market

Acceleration from adoption to procurement: The market’s compound momentum—from a modest base in 2020 to an industry measured in the low billions by mid‑decade—means product qualification cycles across AR/VR vendors and defense prime contractors are now transitioning into production commitments and capacity expansion. Our 2026 baseline reflects this shift from prototyping to commercial deployment.

Si Oled Microdisplay Market

Scale economics will become visible: The map from lab to fab is narrowing. In our forecast, the market size increases markedly in 2026 relative to 2025 as new production lines and public market capital raise activities come online, compressing unit costs and enabling price points that broaden addressable consumer and enterprise segments.

Si Oled Microdisplay Market

Policy and defense procurement are amplifiers: Large, multi‑year defense programs and supplier selections are accelerating demand for ruggedized, high‑brightness Si‑OLEDs. Recent government and prime‑contract awards, alongside ITAR‑sensitive manufacturing zones, are reshaping sourcing strategies and supplier selection criteria.

Our aggregated market model shows a pronounced expansion through the forecast window. From a base in 2025, the market grows into 2026 and beyond with a 29.85% CAGR across our 2026–2032 forecast. This implies that companies that secure supply, secure IP, or secure channel partnerships early in 2026 will capture disproportionate share as the market scales. The valuation of near‑term capacity and IP is therefore not linear—minor advantages in integration, yield, or optics partnerships translate to outsized commercial returns.

Sony Semiconductor Solutions Corporation — A technology leader with mature OLEDoS SKUs and a roadmap toward higher brightness and pixel density. Sony’s recent product introductions position it as a benchmark supplier for high‑resolution AR/VR optics and camera EVFs. For strategic buyers, Sony represents a low‑execution‑risk partner with clear product performance credentials.

eMagin Corporation — A US fabs‑based specialist with defense and industrial pedigree and ITAR compliance; its direct patterning approaches and white‑OLED architectures continue to attract mission‑critical applications where ruggedization and certification paths matter.

SeeYA Technology — A pure‑play Si‑OLED entrant that completed a public listing and announced capacity expansion in 2026. For strategic investors and OEMs seeking volume and cost leverage, newly public pure‑plays are important to watch for aggressive capacity monetization and partnership offers.

Kopin, BOE, MICROOLED, Seiko Epson, OLiGHTEK, OLEDWorks — Each brings differentiated value: Kopin’s defense system integrations; BOE’s process scale and tandem‑OLED brightness strategies; MICROOLED and Seiko Epson’s optical engine integrations for wearables; specialist US and European players offering niche, high‑reliability parts.

Market concentration is meaningful: our CR3 and CR5 measures indicate a market where the top three firms account for the majority of industry revenue and the top five consolidate an even larger share. For buyers, this highlights a dual dynamic—supply security via incumbent suppliers, and opportunity via partnerships with emerging challengers that may offer aggressive pricing or specialized IP.

Silicon backplanes + OLED stack — the performance lever: The pairing of standard CMOS silicon backplanes with OLED emissive layers is the technical core of the Si‑OLED opportunity. This combination delivers ultra‑high pixel density, contrast and power profiles optimized for head‑mounted displays. Recent prototype work by research institutes and industrial labs demonstrates continued progress on high‑voltage backplanes and pixel‑level power management—both determinants of next‑generation battery life and image quality.

Optical subsystem integration: Near‑eye systems are system‑level products. Display characteristics must be balanced with waveguides, freeform optics, and eye‑box requirements. Companies that can offer module‑level solutions (display + optics + driver + thermal) will command premium positioning with OEMs seeking integration risk reduction.

Manufacturing and capacity risks: Yield curves for microdisplay fabs are steep. New entrants with public capital infusions intend to expand production, but time to yield stabilization matters. Our strategic playbook emphasizes staged capacity commitments, dual‑source qualification, and options for in‑country production to align with defense procurement constraints.

Supplier strategy: Move from single‑vendor prototypes to dual‑qualified supply for critical SKUs by Q4 2026. Negotiate milestone‑based commitments that link price declines to yield and volume thresholds.

Product strategy: Prioritize modular optical engines that allow display swaps without major mechanical redesigns. This hedges against unexpected changes in supplier roadmaps while accelerating time‑to‑market.

Commercial models: Consider hybrid buy‑and‑co‑develop structures for suppliers that offer both IP and production capacity. For strategic OEMs, minority equity in a key supplier can secure allocation at scale.

Regulatory & procurement readiness: For companies pursuing defense contracts or regulated industrial tenders, ITAR compliance, in‑country assembly options, and supply‑chain pedigree audits must be part of procurement timelines.

The full Si‑OLED Microdisplay Market report is built as a hands‑on decision support kit for 2026. Key components include:

Quantitative market model (2020–2025 historical, 2026–2032 forecast) with scenario analysis and sensitivity to adoption curves and price elasticity.

Investment and capacity playbook: capex timelines, lead‑time risk matrices, and production yield ramps modeled for established fabs and new entrants.

Supplier profiles and vendor scorecards assessing technology, capacity, IP ownership, certification readiness, and commercial posture.

Go‑to‑market templates for OEMs and ODMs—module specification checklists, qualification roadmaps, and contracting templates oriented to minimize time to production.

Strategic M&A and partnership candidate list with high‑level rationale, integration risk assessments, and value‑creation levers (cost synergies, IP pools, channel access).

Risk register: technology obsolescence timelines, geopolitical supply constraints, and regulatory touchpoints with mitigation playbooks.

If you are an OEM: Use the market model to justify earlier production commitments and negotiate volume‑phased pricing tied to yield improvement milestones.

If you are a supplier: Prioritize demonstrable yield improvement and optical module partnerships that reduce OEM integration cycles; consider capital partnerships to scale capacity with lower balance‑sheet risk.

If you are an investor or private equity sponsor: Favor targets with defensible IP, customer commitments, and clear pathways to qualification in defense or enterprise verticals where margins are higher and cycles are longer.

Public capex announcements and fab‑ramp timing from pure‑play Si‑OLED providers.

Defense procurement awards and prime contractor supplier lists that indicate program allocations for head‑mounted displays.

Prototype demonstration metrics: brightness, power per pixel, and yield progression in commercial fabs.

Optical module qualification timelines and OEM design wins that presage consumer and enterprise adoption.

For executives planning strategic moves in 2026, the choice is between reactive procurement and proactive positioning. The market’s projected CAGR of 29.85% and the commercially visible expansion from 2025 into 2026 mean that early contractual positions, flexible product architectures, and supply‑chain resilience will separate winners from followers. PW Consulting’s full report provides the underlying segment analytics, supplier economics, and executable templates to convert insight into action—without which 2026 purchasing and partnership windows risk being suboptimally allocated.

To access the full dataset, segment breakdowns, supplier scorecards, and our proprietary financial model, please refer to the PW Consulting Si‑OLED Microdisplay Market report landing page. The full report contains the detailed segmentation and monetary models required to build investment cases, negotiate supply agreements, and plan capacity expansions for 2026–2032.

For detailed analysis of this topic, please visit the official page:Si Oled Microdisplay Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com