Integral Total Station Historic Market: Strategic Outlook for 2026 Decision‑Making

Executive summary

PW Consulting’s latest market study, Integral Total Station Historic Market (base year 2025), synthesizes five years of observed market behavior and a forward-looking forecast through 2032. The report combines a rigorous market model, vendor and technology mapping, and operational playbooks to inform capital allocation, procurement, and product strategy for stakeholders across surveying, construction, mining, and infrastructure sectors. With the market exhibiting a sustained compound annual growth rate of 6.75% and an observable progression from mid‑2020s levels to a substantially higher end‑of‑decade market size, our analysis translates quantitative momentum into practical decisions for 2026.

Integral Total Station Historic Market

Market trajectory and what it means for 2026

Between 2020 and 2025 the integral total station market recorded steady expansion driven by automation adoption, cloud‑enabled workflows, and renewed infrastructure investment. The PW model captures this evolution and projects continued growth through 2032. These macro dynamics create a favorable backdrop for equipment vendors, systems integrators, and capital equipment buyers in 2026 — but not without important strategic inflection points.

Integral Total Station Historic Market

- Growth continuity: A multi‑year CAGR in the high single digits underpins a stable demand environment that supports measured capacity expansion, incremental R&D investment and selective M&A.

- Technology premium: Buyers increasingly favor integrated solutions (robotics, GNSS hybridization, cloud platforms and imaging), shifting spend from inexpensive manual units toward higher‑value, automation‑enabled systems. Suppliers that package hardware with data and lifecycle services capture disproportionate value.

- Concentration and competitive dynamics: Market concentration is meaningful — the top three firms account for roughly 62% of market value, and the top five cover approximately 75%. This structure amplifies the influence of platform roadmaps, channel partnerships and after‑sales ecosystems on market outcomes.

Strategic implications for 2026 — five investor and operator priorities

For executives planning capital expenditure, vendor managers negotiating supply agreements, and strategy teams charting product roadmaps, the report highlights five priority actions that should shape 2026 plans.

Integral Total Station Historic Market

- Move beyond unit price to lifecycle value. As automation, software and security features become standard expectations, procurement should be driven by total cost of ownership and data‑service economics rather than headline hardware discounts. Our TCO modules show how modest investments in cloud and service subscriptions alter breakeven timelines materially.

- Prioritize interoperable platforms. Integration with BIM, GIS, and existing GNSS systems reduces project friction and accelerates ROI. Suppliers offering open APIs and robust device‑to‑cloud pipelines are positioned to win longer, higher‑margin contracts.

- Mitigate supply and component risk. Sensor availability and pricing experienced episodic tightness in recent periods; procurement strategies in 2026 should include multi‑source qualification, safety‑stock policies for critical sensors, and flexible contract terms to absorb short‑term volatility.

- Incorporate security and asset protection into specification. Recent product introductions stress asset security (locating and theft deterrence) and secure cloud data management. For asset‑intensive fleets, these features reduce non‑operational downtime and insurance friction, and should be evaluated quantitatively.

- Prepare for differentiated regional demand. Infrastructure spending patterns and urbanization trajectories vary across geographies. Our scenario analyses help translate macro fiscal commitments into pragmatic procurement phasing — a tactical advantage for firms managing inventory, service networks and field training.

Competitive landscape — innovation themes and vendor positioning

The report’s vendor analysis synthesizes product portfolios, channel footprint and recent strategic moves across the industry. Several observable themes inform 2026 competitive positioning:

- Platformization and cloud services. Long‑standing instrument OEMs have shifted from standalone devices to subscription‑oriented platforms. Recent launches from leading vendors emphasize cloud data management and device security as differentiators, and the ability to monetize recurring services will be a key profit driver.

- Robotics and automation focus. Robotic total stations continue to command attention in mid‑to‑large construction and infrastructure projects because of crew efficiency gains and improved data fidelity. New product introductions over the last 24 months accelerate this trend.

- Localization and cost‑to‑serve strategies. Regional producers and value brands are closing the capability gap with competitive hardware and localized support models, compressing pricing at the entry and mid‑market tiers while enabling wider adoption.

- Strategic partnerships with construction and engineering firms. Integrative arrangements — from embedded hardware pilots to software workflow integrations — are reshaping go‑to‑market models, especially on large infrastructure programs.

Key players featured in the report include global precision brands, established platform leaders, and regional specialists. Our profiles cover headquarters, core competencies, recent product and platform launches, and a strategic assessment of R&D and channel execution. Notable market moves covered in detail include a major OEM’s integrated security and cloud platform rollout in late 2025, and earlier robotic product introductions and industry partnerships that illustrate the competitive playbook.

What the report delivers — practical, actionable content

The Integral Total Station Historic Market study is designed to be operationally useful, not just descriptive. Highlights of the deliverables include:

- Proprietary market model and forecast engine. Year‑on‑year historical reconciliation (2020–2025) and scenarios to 2032 with sensitivity levers for infrastructure spend, technology substitution, and pricing dynamics.

- Vendor benchmarking toolkit. A repeatable matrix comparing product functionality (automation, range, sensor integration), commercial models (capex vs. subscription), channel structure and after‑sales capabilities; each profile includes recommended negotiation levers for procurement teams.

- Commercial playbooks. Channel and direct sales strategies segmented by account archetype (national infrastructure, contractor fleets, surveying specialists) with go‑to‑market priorities for 2026 and templated service agreements.

- Operational templates for field teams. Calibration and compliance checklists aligned with ISO testing protocols and land‑survey accuracy standards, along with sample field validation protocols for new units and fleet on‑boarding.

- Risk and resilience planning modules. Supply‑chain mitigation options, critical component sourcing maps and an inventory hedging framework tailored to sensor and EDM supply cycles.

- ROI and investment cases. Pre‑built calculators that translate device and service choices into project‑level economics, enabling CFOs and project managers to make data‑driven tradeoffs.

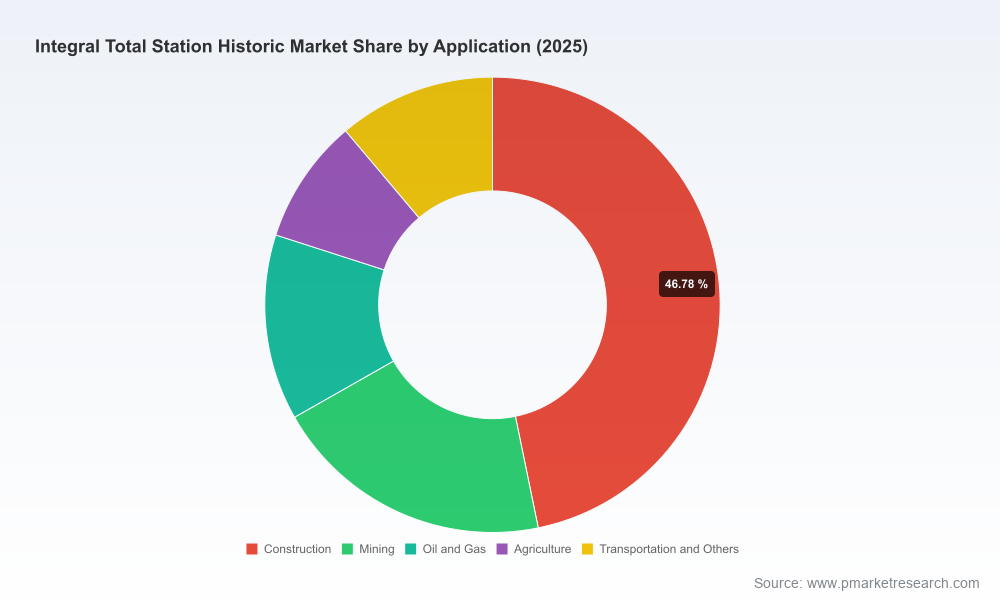

For confidentiality and strategic reasons this release refrains from reproducing the granular regional and application splits, and detailed vendor share tables included in the full report; these are available exclusively to report subscribers.

Regulatory and materials context

Surveying equipment manufacturers and buyers operate within established calibration and testing regimes. Alignment with ISO calibration protocols and project‑level accuracy standards (including land title survey tolerances) is non‑negotiable for large projects and is covered in the report’s compliance module. On the supply side, elective component markets — notably sensors and imaging subsystems — experienced intermittent tightness during peak demand periods. The recommended supplier strategies in the report emphasize qualification of alternate sources, strategic inventory and contract designs that share risk between suppliers and buyers.

How to use the report in 2026 planning cycles

We recommend three immediate uses for C‑suite and operational teams preparing 2026 plans:

- CapEx prioritization. Use our TCO and scenario outputs to re‑rank equipment investments based on lifecycle economics rather than one‑time purchase price.

- Vendor negotiation and contracting. Leverage the vendor benchmarking and negotiation playbooks to secure bundled hardware‑software agreements with clear service‑level and upgrade pathways.

- Field modernization roadmap. Implement the operational templates to reduce commissioning time, standardize calibration practices and accelerate productivity gains from automation investments.

Conclusion — strategic value proposition

The Integral Total Station Historic Market report translates market momentum into concrete strategic choices for 2026. With a steady growth trajectory and pronounced consolidation among leading vendors, the coming year will reward organizations that align procurement to lifecycle economics, embrace interoperable platforms, and insulate supply chains against component volatility. PW Consulting’s study provides the market modelling, vendor intelligence and executional tools required to convert industry trends into defensible, measurable operational outcomes.

Next steps

For teams seeking the full dataset, granular segmentation, vendor share tables and downloadable operational templates, the complete report and accompanying briefing packages are available from PW Consulting. Contact our research team for a tailored briefing that maps the report insights to your organization’s priorities for 2026.

For detailed analysis of this topic, please visit the official page:Integral Total Station Historic Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com