How Bolt Company Evaluation Germany Market Share Safety Reliability Demand Surges

Other |

2026-06-15 10:41:59

As organizations plan capital allocation and product roadmaps for 2026, the filter pump market presents a blend of resilient growth, regulatory-driven disruption, and concentrated pockets of competitive intensity. PW Consulting’s latest Filter Pump Market report synthesizes macro trajectories, regulatory inflection points, and actionable go-to-market playbooks designed to guide executives — from OEM product leads to private equity sponsors and municipal procurement teams — toward higher-confidence decisions this coming year.

Filter Pump Market

Our analysis indicates the global filter pump market has expanded steadily over the past half-decade and is set to progress through the 2026–2032 forecast window at a compounded annual growth rate (CAGR) of approximately 5.65%. After a measured recovery and expansion between 2020 and 2025, the market is positioned to continue upward momentum into the late 2020s driven by energy-efficiency retrofits, growing demand in both residential and industrial water-treatment applications, and the adoption of smart controls across installed bases.

Filter Pump Market

Two strategic implications flow from that macro frame: first, mid-single-digit growth at the market level masks heterogeneity in technical adoption and margin pools; second, steady growth combined with regulatory pressure creates windows for differentiated premiumization and cost-out plays.

Filter Pump Market

Regulation accelerates product cycles: Energy-efficiency standards in major markets have moved the baseline for acceptable product performance. Where variable-speed and motor-efficiency rules have rolled out, incumbents and challengers alike must either invest in compliant platforms or plan for rapid phase-out of legacy models. That creates a narrow window for product-transition strategies that preserve aftermarket revenue.

Digitalization separates winners from also-rans: Smart controls and system-level integrations (e.g., pool automation ecosystems and remote monitoring for industrial filtration) are becoming table stakes in many contracts. OEMs who can pair hydraulic performance with software-enabled service models gain outsized lifetime value.

Operational scale and specialization both matter: Market concentration metrics show that the top-tier suppliers account for a meaningful share of revenue, but not so large as to eliminate opportunities for niche specialists — particularly in corrosion-resistant, high-chemistry, and industrial wastewater segments. For investors, this implies differentiated M&A strategies: buy scale in core segments or acquire specialization for premium niches.

Upgrade and upsell installed bases. For manufacturers and distributors, prioritize retrofit kits, variable-speed conversions, and service contracts in regions where replacement cycles are short and energy tariffs are high. These offerings can be introduced with limited capital expenditure but have attractive margins due to labor- and service-led revenue.

Modularize product platforms. Adopt a platform architecture that allows shared motor, control, and sealing subsystems across centrifugal and positive-displacement lines. Modularization reduces time-to-market for compliant variants and enables faster responses to regional regulation changes.

Pursue software-enabled monetization. Embed remote diagnostics and predictive maintenance features that feed subscription or outcome-based contracts. Owners in commercial pools, municipal treatment, and industrial facilities increasingly value uptime and energy transparency over unit price.

De-risk supply chains strategically. Identify critical components (motors, seals, electronic controllers) and dual-source them, or secure capacity via contract manufacturing arrangements. Given the market’s split between global OEMs and regional specialists, resilience in procurement will be a differentiator during 2026 procurement cycles.

Make focused M&A moves. For private equity and strategic buyers, look for tuck-in targets that fill capability gaps (corrosion-resistant materials, specialty filtration media, or smart control IP) rather than broad-scale consolidation at elevated multiples.

Executive playbooks: Tailored strategic recommendations for OEMs, distributors, facility owners, and investors, including product roadmaps, retrofit bundle strategies, and service pricing templates designed for 2026 procurement realities.

Regulatory impact mapping: A dynamic view of how recent and pending energy-efficiency standards affect product lifecycles by equipment class, with decision trees to prioritize engineering investments.

Technology deep dives: Comparative analyses of motor technologies, variable-speed drive architectures, materials for chemical resistance, and the economics of integrated sensing and controls.

Commercial benchmarking: Go-to-market templates, channel-margin models, and pricing sensitivity scenarios that enable fast scenario planning for 2026 bid cycles.

Deal origination support: A vetted list of acquisition targets and partnership candidates, with operational red flags and integration playbooks tailored to different buyer archetypes.

On-the-ground validation: Primary interviews with industry procurement leads, field tests of emerging variable-speed systems, and supply-chain stress-tests give you confidence that recommendations have practical grounding.

The competitive fabric of the filter pump market is composed of large, brand-led incumbents and specialized manufacturers. Established providers such as Pentair, Hayward, Grundfos, and Xylem continue to invest in energy-efficient and smart-pump technologies, while specialized suppliers — including corrosion-resistant product lines from Filter Pump Industries (part of Finish Thompson) and compact, value-oriented offerings from firms targeting above-ground pool segments — sustain vigorous competition at the channel level.

Recent product and portfolio developments point to several persistent themes:

Product awards and catalog refreshes: Recognition for intelligent variable-speed pumps and refreshed product catalogs signal continued emphasis on energy-efficiency positioning and broad channel enablement.

Product integration and automation partnerships: Integration of pump lines with automation ecosystems underscores the move from component sales to system sales — a trend that favors firms able to deliver both hardware and software experiences.

Strategic acquisitions: Consolidation activity focused on specialty technologies (e.g., corrosion-resistant materials or specialized filtration media) highlights the willingness of larger players to buy capability rather than build from scratch.

For executives, the competitive takeaway is clear: invest selectively in platform-level capabilities that create barriers (e.g., service ecosystems, integrated controls) while watching for acquisition targets that accelerate entry into high-margin niches.

Energy-efficiency regulations enacted in multiple jurisdictions are reshaping allowable product specifications and accelerating the replacement of legacy single-speed pumps. Variable-speed solutions can materially reduce operational energy consumption in many applications, presenting an opportunity to offer lifecycle-cost-based value propositions rather than competing solely on upfront price.

In practice, region-specific motor and energy rules mean that product managers must build compliant variants and retrofit pathways into their 2026 roadmaps. Firms that proactively adapt to these rules and combine them with data-driven service models will capture greater lifetime value from customers and avoid disruptive, higher-cost redesigns later.

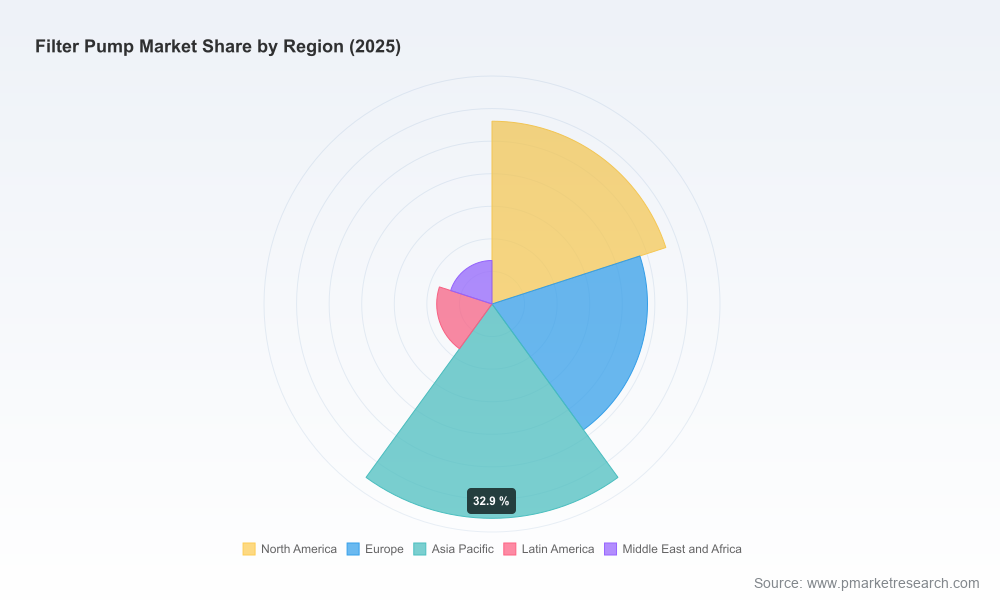

The market exhibits moderate concentration: a cluster of global players captures a significant share of revenue while a long tail of regional and application-specific suppliers remains active. That structure creates two distinct investment plays for 2026:

Scale play: Consolidate channel reach and global manufacturing footprint to drive unit-cost efficiency and accelerate penetration into commercially attractive geographies.

Specialist play: Acquire material- or application-specific capabilities (e.g., corrosion-resistant pumps, industrial wastewater configurations, or smart filtration media) where pricing power and margin profiles are stronger.

Quarter 1: Run a regulatory gap assessment across core and adjacent product lines. Prioritize retrofits and compliant SKUs for immediate channel release.

Quarter 2: Launch a pilot subscription or service bundle with select commercial accounts to validate pricing and technical integration for remote monitoring.

Quarter 3: Evaluate two acquisition targets: one for scale (manufacturing or distribution) and one for capability (materials, controls). Conduct commercial diligence using PW Consulting’s integration playbooks.

Quarter 4: Roll out a modular platform strategy for the following product generation, incorporating motor and control commonality to reduce time-to-market and regulatory redesign risk.

2026 will separate firms that merely comply with new product rules from those that convert regulatory pressure into a competitive moat. The market’s steady mid-single-digit growth provides a favorable backdrop, but the real value will accrue to companies that combine product modernization, service-enabled monetization, and tactical M&A. PW Consulting’s Filter Pump Market report arms decision-makers with the strategic frameworks, commercial templates, and validated market signals to make those moves with confidence.

For decision-makers seeking the full set of operational playbooks, competitive profiles, and scenario-modeled forecasts — including interactive tools to stress-test your strategy against regulatory and pricing shocks — download the complete PW Consulting Filter Pump Market report. The report contains proprietary benchmarking, detailed company dossiers, and the granular guidance required to execute your 2026 plan.

For detailed analysis of this topic, please visit the official page:Filter Pump Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com