Chromium Market Set to Reach US$ 21.3 Bn by 2031 Amid Rising Demand from Stainless Steel and Metallurgical Applications

Other |

2026-06-12 09:02:40

PW Consulting’s new Zellweger Spectrum Disorders Market report translates sparse epidemiology, concentrated commercial activity, and nascent scientific breakthroughs into a practical playbook for executives making resource-allocation decisions in 2026. Our modeling shows the overall market expanding from an estimated USD 312.95 Million in 2025 to approximately USD 493.39 Million by 2032, driven by a compound annual growth rate of 6.72% through the forecast window. Those headline numbers matter — but the tactical choices that determine who captures value will hinge on diagnostics access, regulatory pathways, and the timing of potential disease-modifying technologies now emerging from preclinical pipelines.

Zellweger Spectrum Disorders Market

The Zellweger Spectrum Disorders ecosystem remains small by conventional commercial standards but is growing at a steady mid-single-digit pace. Growth is supported by improving diagnostic throughput, incremental commercial expansion of existing adjunctive therapies, and heightened R&D activity aimed at genetic correction. At the same time, the market structure is highly concentrated, with the largest incumbents commanding the majority of commercial activity. For 2026 decision-making, that combination—finite patient numbers, reliable CAGR, and high concentration—creates a strategic environment where targeted investments, partnerships, and early payer engagement yield asymmetric returns.

Zellweger Spectrum Disorders Market

Scientific momentum: In April 2026, preclinical base editing corrected the common PEX1-p.G843D mutation in a mouse model, restoring peroxisome function and ameliorating liver pathology. This proof-of-concept materially increases the probability that gene-editing approaches will enter human proof-of-concept trials within a predictable multi-year window, radically changing long-term market economics.

Zellweger Spectrum Disorders Market

Commercial continuity and guideline support: The incumbent commercial therapy for hepatic manifestations continues to report availability and market traction, and clinical guidance in late 2025 reaffirmed its role as an approved adjunctive option for liver disease in peroxisomal disorders. That stability preserves near-term revenue visibility for established players while leaving the door open for new value propositions that address extrahepatic disease.

Diagnostics as a lever: Broader adoption of targeted genetic panels and centralized testing services is increasing diagnostic capture, shortening time-to-diagnosis, and enabling earlier intervention—factors that will determine uptake curves for any new therapeutic modalities.

The market is dominated by a small set of specialized companies and diagnostic service providers. Mirum Pharmaceuticals remains the commercial face of the only FDA-approved adjunctive therapeutic for peroxisomal liver disease manifestations and benefits from clinician familiarity and established supply chains. Diagnostics and testing providers — including both clinical genetics platforms and laboratory services companies — serve as the primary gateway to patient identification and phenotype stratification. Laboratory instrument and reagent suppliers underpin this ecosystem by enabling higher throughput and better molecular sensitivity.

Mirum Pharmaceuticals, Inc. (Foster City, CA) — markets the only approved adjunctive cholic acid therapy for hepatic manifestations. Strategic considerations: defense of coverage and reimbursement, lifecycle planning, and partnerships to position for combination strategies should disease-modifying therapies emerge.

Genetic testing platforms and laboratories (examples include Invitae, GeneDx, CENTOGENE) — control patient identification, variant interpretation workflows, and referral networks. Strategic considerations: scaling panel adoption, integration with specialty centers, and value-based contracting with payers.

Diagnostic suppliers (examples include PerkinElmer, Thermo Fisher Scientific) — supply instruments, reagents, and automation that reduce per-test cost and turnaround time. Strategic considerations: channel partnerships, co-marketing with labs, and bundling diagnostics with trials to accelerate enrollment.

Collectively, the top-tier commercial and diagnostic players account for a disproportionate share of market activity (market concentration metrics indicate a strong incumbent position). For potential entrants or investors, this concentration means the path to scale is likely to be partnership- or acquisition-led rather than purely organic.

Proprietary market model: multi-scenario demand curves, uptake timing for diagnostics and therapeutics, sensitivity analyses that translate scientific timelines into P&L and valuation impacts.

Regulatory and reimbursement playbooks: pathway maps for adjunctive therapies, gene-editing strategies, and diagnostic coverage, incorporating recent FDA history and payer precedents.

Competitive and commercial dossiers: validated profiles of incumbent and emerging players, channel maps, and supplier ecosystem analysis (instruments, reagents, lab capacity).

Decision tools: go/no-go checklists for R&D investment, M&A screening templates, licensing term comparators, and partnership scorecards tied to patient identification efficiencies.

Primary intelligence: stratified interviews with clinicians, laboratory directors, payers, and patient-advocacy stakeholders, and a synthesis of real-world treatment patterns and barriers to access.

Pharmaceutical and biotech strategy: Adopt a two-track approach — protect and optimize existing adjunctive therapies through payer engagement and evidence generation, while de-risking disease-modifying programs by investing in translational milestones, manufacturing readiness, and early safety strategies. Secure diagnostic partnerships early to guarantee patient flow into trials.

Diagnostics and lab services: Prioritize scale and interoperability. Investments in automated workflows, faster turnarounds, and clinician-facing variant interpretation tools will increase referral share. Consider strategic alliances with specialty centers to become the ‘default’ testing pathway.

Investors and M&A teams: Focus on assets that materially change patient identification rates, reduce time-to-enrollment for trials, or de-risk clinical translation of gene-editing technologies. Given market concentration, bolt-on acquisitions that create integrated diagnostic-therapeutic platforms can accelerate commercial returns.

Payers and HTA bodies: Prepare conditional-coverage frameworks that accommodate breakthrough gene-editing therapies while protecting payers from unproven long-term outcomes. Early dialogue with sponsors on outcomes-based contracting will be essential.

Translational risk: Preclinical correction of common mutations is promising but not determinative. Human safety, delivery challenges, and durable efficacy remain uncertain; timeline slippage could compress investment returns.

Reimbursement and access: Small patient numbers and high per-patient costs will necessitate creative payer arrangements; failure to establish reimbursement precedents could limit commercial viability of high-cost curative approaches.

Operational constraints: Laboratory capacity, skilled genomic interpretation resources, and clinician awareness are bottlenecks that can mute the realized market size even as headline incidence and diagnostic capability improve.

Strategic choices made in 2026—whether to fund a gene-editing IND, acquire a diagnostics provider, or double down on commercialization of adjunctive therapy—will determine who benefits as the market evolves. PW Consulting’s report converts epidemiology, technology inflection points, and commercial dynamics into executable plans: we do not just forecast numbers, we show how to influence the levers behind them. That includes playbooks for accelerating trial enrollment through diagnostic networks, structuring risk-sharing contracts with payers, and sequencing investments to match scientific milestones.

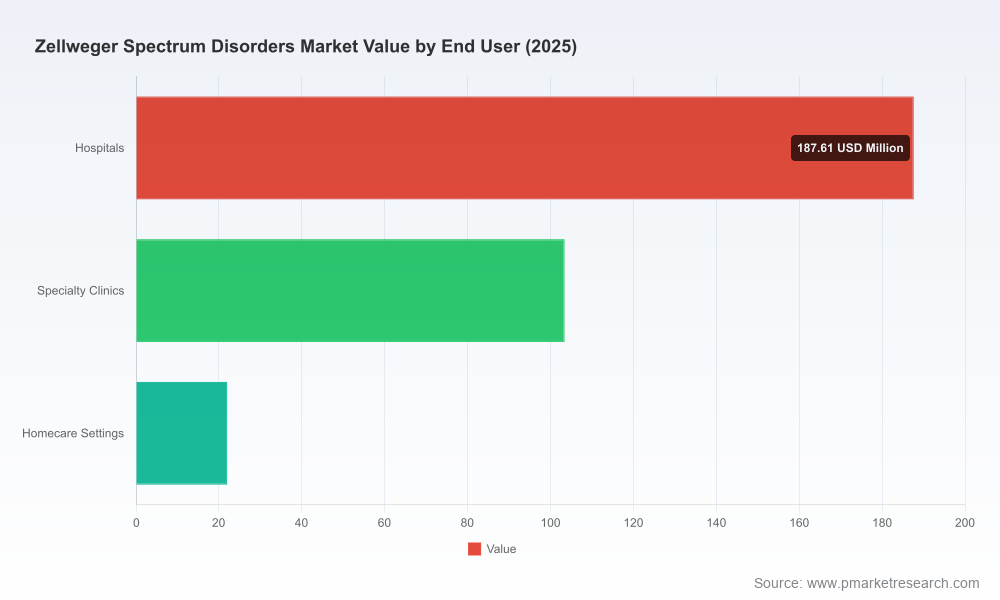

This release is intended as a strategic preview. To preserve competitive value for our clients and to ensure responsible use of sensitive segment-level data, we provide the full suite of granular forecasts, regional breakdowns, product and end-user models, and primary-source transcripts exclusively via the full report. Executives seeking transaction-ready analytics, deal-specific scenario modeling, or bespoke advisory support are invited to access the comprehensive report and consultancy services through PW Consulting’s distribution channels.

In a rare market where validated adjunctive therapy exists alongside the real prospect of genetic correction, timing and execution matter more than ever. PW Consulting’s Zellweger Spectrum Disorders Market report is built to make 2026 the year your strategy shifts from reactive to anticipatory.

For detailed analysis of this topic, please visit the official page:Zellweger Spectrum Disorders Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com