Corn Germ Meal Market 2026 Strategic Preview: Actionable Intelligence for Executive Decision-Making

Executive summary

As the feed ingredient complex adapts to shifting protein economics and feedstock availability, corn germ meal is re-emerging as a strategically important co-product for animal nutrition and integrated processors. PW Consulting’s new market study (base year 2025; forecast period 2026–2032) synthesizes macro demand drivers, supply-side capacity changes, regulatory headwinds, and competitive positioning into a compact suite of decision tools aimed at commercial, procurement, and corporate development teams planning for 2026 and beyond.

Corn Germ Meal Market

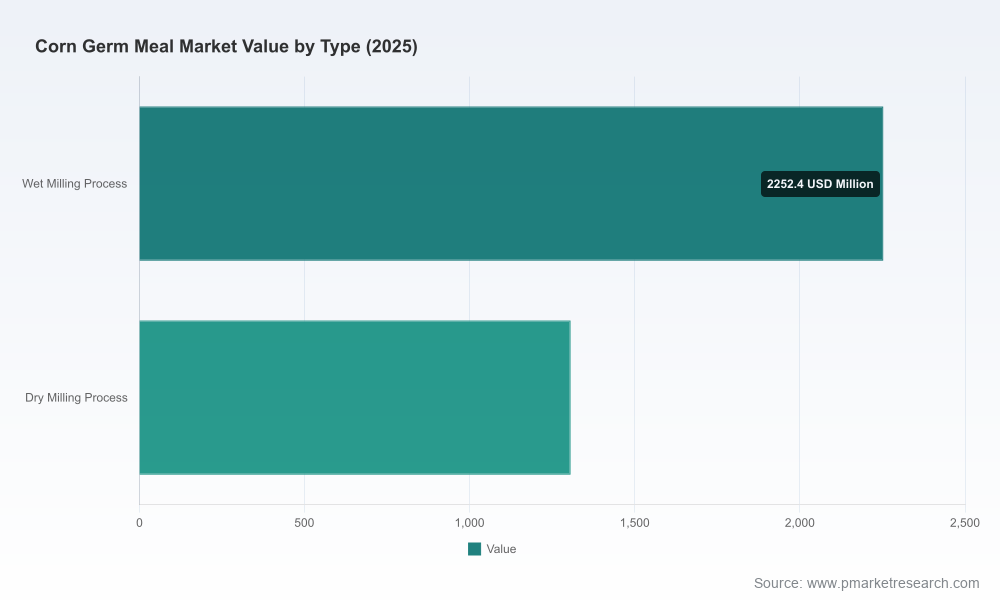

Key headline metrics: the global corn germ meal market expanded materially over the 2020–2025 period and reached an estimated USD 3,558 million in 2025. Our model projects steady expansion through the forecast horizon at a compound annual growth rate of 4.52%, with the market approaching the mid-single‑thousand‑million USD range by the end of the forecast period. This trajectory reflects a mix of demand-side formulation shifts, incremental capacity additions at wet‑milling complexes, and ongoing quality/regulatory pressures that together create both margin compression and selective premiumization opportunities.

Corn Germ Meal Market

Why this report matters for 2026 decision-makers

- From tactical sourcing to strategic supply security: Our analysis equips procurement teams with a playbook to convert co-product variability into predictable supply via contract structures, short‑term swaps, and capacity-linked off‑take arrangements.

- From product development to feed formulation: Nutrition and technical teams get a concise mapping of substitution levers (soybean meal displacement, inclusion-rate sensitivities in poultry and swine rations) together with practical trade-offs across performance, cost, and digestible energy.

- From corporate development to M&A: Investors and corporate development leaders receive an actionable target-screening framework that balances asset quality (wet‑milling throughput, extraction efficiency), regulatory compliance, and proximity to integrated feed markets.

- From risk management to compliance: Regulatory monitoring and quality assurance guidance help operations teams prioritize testing, certification (e.g., GMP+), and supplier audits to defend against contaminant exposures that can rapidly erode offtake confidence.

What the study contains — practical, ready-to-use deliverables

- Interactive market model (Excel) that allows scenario testing by feed mix, oil extraction yields, and price curves across the 2026–2032 forecast window.

- Supply-demand balance and inventory sensitivity charts that translate mill-level throughput shocks into regional availability scenarios.

- Price sensitivity and margin-impact matrices for feed formulators showing breakeven substitution points versus soybean meal and typical co-product baskets.

- Supplier scorecard templates and procurement contract playbooks (short/medium/long term) tailored to co‑product volatility and capacity ramp risks.

- M&A screening checklist and valuation adjustments for wet‑milling assets, including a CAPEX/OPEX benchmarking library and likely synergies for integrated feed/offtake strategies.

- Regulatory watchlist and quality-control protocols, including GMP+ alignment, mycotoxin mitigation pathways, and traceability best practices.

Market outlook and themes shaping 2026 strategy

Three macro themes will determine market winners and losers entering 2026:

Corn Germ Meal Market

- Demand rationalization and feed formulation elasticity: Corn germ meal’s role as a medium‑protein, energy‑dense ingredient gives feed formulators flexibility to displace higher‑cost proteins in certain ruminant and monogastric rations. Our feed-model scenarios show that modest relative price shifts between corn co-products and soybean meal materially change inclusion economics—creating tactical windows for buyers and margin pressure for commodity sellers.

- Incremental wet‑milling capacity and co‑product dynamics: Leading processors continue to optimize extraction yields and line utilization, which periodically increases corn germ meal availability. Recent capacity moves at strategic facilities are already translating into tighter production rhythms and renewed competition for offtake contracts.

- Quality, certification, and regulatory scrutiny: The industry continues to tighten controls around contaminants—mycotoxins, pesticide residues, and heavy metals—making certification and documented traceability a source of commercial differentiation rather than mere compliance.

Competitive landscape — who matters and why

The market remains characterized by a diverse set of global and regional operators, with a modest degree of fragmentation: the largest players collectively capture less than one-third of the market, leaving ample room for regional champions and specialized processors. PW Consulting’s company dossiers focus on capability vectors that matter to buyers and investors:

- Archer Daniels Midland Company (ADM) — Chicago, USA: A major wet‑milling operator with integrated processing footprints. ADM’s recent expansion at a key Nebraska facility underscores a strategy of incremental capacity investment to secure co‑product streams and capture value across the oil extraction-meal value chain.

- Cargill, Incorporated — Minnetonka, USA: A global agribusiness leader with broad wet‑milling exposure; competitive advantage derives from logistical reach and integrated merchandising of co-products into regional feed markets.

- Bunge Limited — St. Louis, USA: Operates corn processing facilities that yield corn germ meal alongside oil extraction — their asset optimization and trading platforms are crucial for smoothing seasonal availability swings.

- Ingredion and Tate & Lyle — (US/UK): Both bring ingredient-specialist capabilities and application development muscle, which matters where quality and co-ingredient synergies command premia.

- Roquette, Grain Processing Corporation, AGRANA, Jungbunzlauer, COFCO, Gulshan Polyols, Zhucheng Xingmao: Regional and specialized operators that play critical roles in local supply chains; some, like Jungbunzlauer, leverage certifications (e.g., GMP+) to access higher-value feed contracts.

Strategic implications: buyers should map supplier portfolios to three axes — availability, certification/quality, and logistics — and avoid equating scale with reliability. Regional processors with strong QA regimes can command price differentials in premium feed channels.

Recent developments worth watching in early 2026

- Major processors continue to invest in germ extraction efficiency; one leading operator announced a double-digit percentage uplift in production capacity at a key midwestern wet‑mill, signaling potential availability increases in proximate feed markets.

- Industry-level production metrics are being tracked monthly by official reporting systems, giving buyers timely visibility into crush and co‑product outputs — an essential input for short‑horizon procurement decisions.

- Certification and contamination controls remain a focal point: several European wet‑mill operators have reinforced GMP+ and related protocols, limiting downside risk for feed buyers but increasing compliance complexity for suppliers.

Risk map and mitigation playbook for 2026

Key risks and corresponding mitigations we recommend for immediate attention:

- Quality and contamination spikes: Implement tiered testing regimes, prioritize GMP+ or equivalent certified suppliers, and embed contingency sourcing clauses in offtake contracts.

- Price and substitution volatility: Use the report’s price-sensitivity model to establish hedging bands and formula‑based pricing clauses that protect both buyers and sellers from abrupt feedstock swings.

- Capacity shocks at wet mills: Negotiate staggered delivery windows, co‑product buffers, and optionality into logistics chains; consider strategic inventory holdings where carrying costs are justified by supply risk.

- Regulatory and trade friction: Maintain a compliance dashboard monitoring GMP+, import/export certifications, and mycotoxin limits to avoid sudden market exclusions.

How to deploy the research in 90 days

- Week 1–2: Run the provided market model on your core feed formulations to identify immediate substitution opportunities and breakeven price points.

- Week 3–6: Use the supplier scorecard and procurement playbook to renegotiate short‑term offtakes and test alternatives against certified regional processors.

- Week 7–12: Apply the M&A screening checklist to any inbound asset deals or JV prospects; validate valuation adjustments with CAPEX/OPEX benchmarks included in the study.

Conclusion: Positioning for upside and defensibility in 2026

The corn germ meal market presents a pragmatic mix of opportunity and operational risk in 2026. For feed producers, formulators, and processors, the near-term prize lies in converting co‑product variability into predictable, quality‑assured feedstreams while extracting margin through application-specific premiumization and logistics optimization. For investors and strategic buyers, the most attractive targets will be assets that combine extraction efficiency, robust quality controls, and direct proximity to feed demand centers.

PW Consulting’s Corn Germ Meal Market Report is designed as a decision‑grade toolkit: not just narrative, but a set of models, playbooks, and templates you can apply immediately. To preserve the commercial value of our segment-level modeling and granular supply‑side analytics, we’ve presented a high‑level preview here — the full report contains the detailed breakdowns, downloadable models, and company-level scorecards that will be central to 2026 planning cycles.

Next steps

Contact PW Consulting to access the full report and downloadable toolset, including scenario-ready Excel models, supplier scorecards, and the company dossier library. The complete dataset (including region- and application-level splits, monthly production series, and the full competitive benchmarking suite) is available on the report landing page and through our client portal.

For detailed analysis of this topic, please visit the official page:Corn Germ Meal Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com