Wolf7pay Trends: What Makes This Platform So Popular?

Sports |

2026-05-21 10:09:19

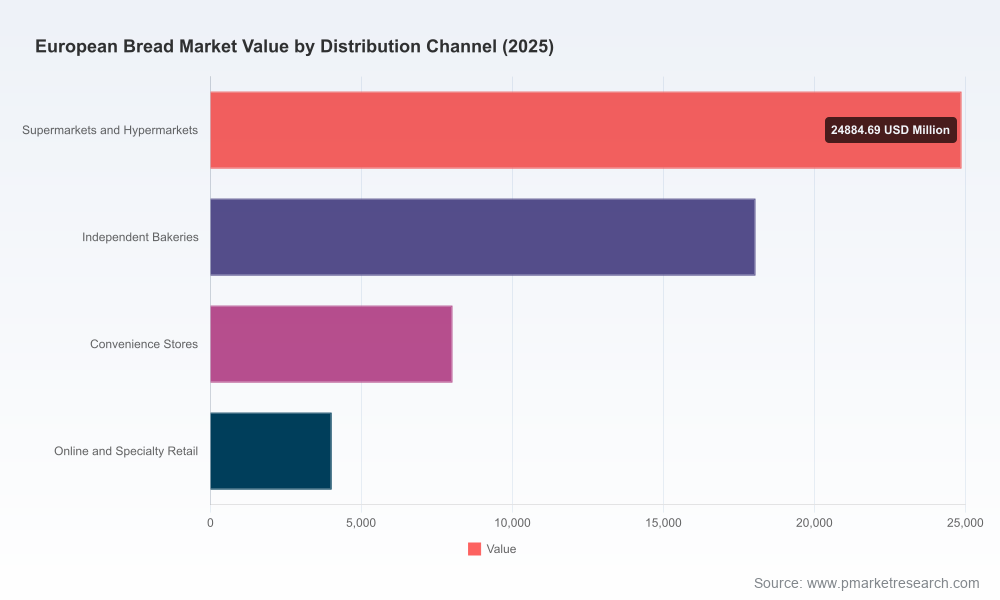

PW Consulting’s new European Bread Market report — base year 2025, forecasting 2026–2032 — is released to inform executive decisions as companies plan capital, supply‑chain and commercial strategies for 2026. At a macro level the market is sizeable and resilient: approximately USD 55.0 billion in 2025, projected to grow at a 2.5% CAGR through the forecast period and reaching roughly USD 65.4 billion by 2032. That steady headline growth masks diverging economics across channels, product forms and routes to market. This briefing highlights the practical implications of those dynamics for 2026 decision‑makers and explains why the full report is required to translate our findings into actionable plans.

European Bread Market

Timing pressure: regulatory and input‑cost events accelerating between mid‑2026 and end‑2026 require near‑term allocation of capex and commercial resources.

European Bread Market

Tactical clarity: the market structure (moderately consolidated with CR3 at ~28.5% and CR5 at ~38.2%) creates specific windows for scale plays, targeted M&A and channel partnerships; our analysis converts that structure into deal‑level guidance.

European Bread Market

Operational readiness: supply‑chain stress tests and SKU economics in the report give procurement and operations teams the tools to defend margins in a rising commodity price environment.

Raw‑material inflation and procurement risk. Wheat futures spiked materially into 2026 (c. USD 666 / Bu as of 20 May 2026, up ~21% year‑on‑year). For baking businesses this is an urgent cash‑flow and margin issue: procurement teams must decide how much to hedge, which long‑term supply contracts to pursue, and where yield‑improvement investments provide a faster margin response than price increases.

Regulatory inflection points. Two regulatory shifts are especially immediate: the EU Packaging and Packaging Waste Regulation (PPWR) coming into force in August 2026 — requiring higher recyclability and recycled content — forces packaging redesign programmes and supplier requalification; and UK mandatory fortification of non‑wholemeal wheat flour with folic acid becoming fully enforceable from December 2026 will affect formulations, labelling and production flows for products sold into the UK. Both create compliance costs but also product differentiation opportunities.

Channel and consumer trends. Convenience, freshness perception and health credentials continue to re‑shape demand. Bake‑off and frozen models that reduce last‑mile complexity are attractive to foodservice and QSR customers, while retail buyers demand both cost efficiency and sustainable provenance. Online and out‑of‑home channels are growing in strategic importance; the report maps the cost‑to‑serve and margin profile of each route to market to help prioritise investments.

Margin pressure and pricing elasticity. With input cost volatility and tighter retail margins, suppliers must redesign pricing architectures (base price, promotions, trade funds) so that each channel captures appropriate value without eroding shopper demand. Our price‑elasticity models show where limited price increases will be absorbable and where product reformulation or pack resizing is a more durable strategy.

Europe’s bread market is served by a mix of large multinationals, regional champions and specialised bake‑off players. The report synthesises public company strategies and proprietary channel checks to profile the behaviours that will determine competitive outcomes in 2026.

Grupo Bimbo — leveraging scale and breadth across sliced, artisan and QSR bakery formats. Their acquisitive footprint and multi‑country operations make them a natural consolidator in markets where distribution scale matters.

ARYZTA AG — focused on frozen and par‑baked convenience bakery; recent capital investment in a new bun plant in Portugal signals strategic prioritisation of QSR and Iberian supply‑chain optimisation.

Lantmännen Unibake — building capability in bake‑off and frozen through M&A and targeted investments to serve both retail and foodservice customers with a bake‑at‑retail/playbook approach.

Barilla — leveraging brand and retail relationships to grow share in sliced and specialty bakery segments while testing premiumisation and health‑led propositions.

Associated British Foods / Allied Bakeries & AB Mauri — combining strong UK operational footprints with ingredient‑and‑input exposures; this group’s integrated model highlights the value of pairing ingredient supply with finished‑goods manufacturing.

European Bakery Group — as a specialised bake‑off and snack producer, this regional operator demonstrates how focused capacity and execution in selected channels produce attractive returns without scale across every geography.

Recent developments underline the strategic direction for 2026: ARYZTA’s €40m bun plant investment (Jan 2026) accelerates QSR supply capability; Lantmännen Unibake’s acquisition of Panificio San Francesco (Dec 2025) deepens bake‑off capability in Southern Europe; and industry‑level policy initiatives such as FEDIMA’s manifesto (Jan 2025) are creating new advocacy vectors for ingredient and sustainability support. Each event is analysed in the report for its competitive and operational implications.

While this release highlights core strategic themes, the full PW Consulting report is designed as an operational playbook for 2026. Deliverables include:

Market sizing and forecasting model (interactive): country and channel scenarios, with sensitivity to commodity price, regulatory compliance costs and consumer mix shifts.

SKU and channel profitability matrices: contribution margins by pack format and route to market, enabling SKU rationalisation with quantified EBIT impact.

Procurement / hedging toolkit: break‑even maps, hedging decision trees and supplier selection scorecards to manage wheat and ingredient exposure.

Packaging compliance playbook: design constraints, validated supplier list and cost‑impact timerails to meet PPWR requirements by August 2026.

Commercial negotiation playbook for retailers and QSRs: templates for trade‑funds, NPD co‑investment and private‑label levers that protect margin and shelf presence.

M&A and partnership scorecards: target prioritisation, integration‑risk templates and synergies calculator tuned to European bakery economics.

Supply‑chain stress tests: capacity utilisation scenarios, factory re‑routing plans and contingency costs to preserve service during input shocks or regulatory transitions.

Policy and stakeholder engagement guide: advocacy points and coalition strategies (e.g., with FEDIMA and retail associations) to influence near‑term regulatory decisions.

Accelerate packaging redesign now, not later. PPWR timing compresses redesign cycles — treating packaging as a strategic asset reduces later re‑work costs and supports premiumisation in retail channels.

Prioritise capacity that reduces last‑mile complexity. Investments in bake‑off and localized frozen capability are effective levers to serve QSR/foodservice growth while lowering distribution cost‑to‑serve.

Hedge raw‑material exposure and strengthen supplier partnerships. Partial hedging combined with productivity investments in yield and recipe optimisation protects gross margin without eroding demand.

Use targeted M&A to acquire capability, not volume. With market concentration uneven, bolt‑on acquisitions that add bake‑off capability, regional distribution or manufacturing tech will generate superior returns.

Rework commercial architecture to align incentives. Move away from discount‑led growth to co‑funded innovation and shared retailer/KPI frameworks that stabilise margins.

Embed regulatory scenarios into product roadmaps. Fortification and labelling rules are not compliance exercises only — they can be reframed as consumer trust and health messaging opportunities.

This briefing has outlined the strategic stakes and practical levers that matter for 2026. To convert these insights into executable plans — with country‑level segmentation, SKU‑level economics, custom scenario runs and the proprietary datasets that underpin our recommendations — access the full European Bread Market report. The complete publication contains all segment and country breakdowns, detailed competitive financials, and downloadable models that are intentionally excluded from this summary to preserve the actionable value of the primary research.

PW Consulting stands ready to brief executive teams, run bespoke scenario workshops and deliver implementation sprints targeted at 2026 milestones. For report access, briefing requests and consulting engagements, please visit PW Consulting’s European Markets page or contact our industry team for an expedited executive pack and data licence.

For detailed analysis of this topic, please visit the official page:European Bread Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com