Global Middle East Cold Plasma In Healthcare Market Forecast to 2034

Other |

2026-03-31 05:41:31

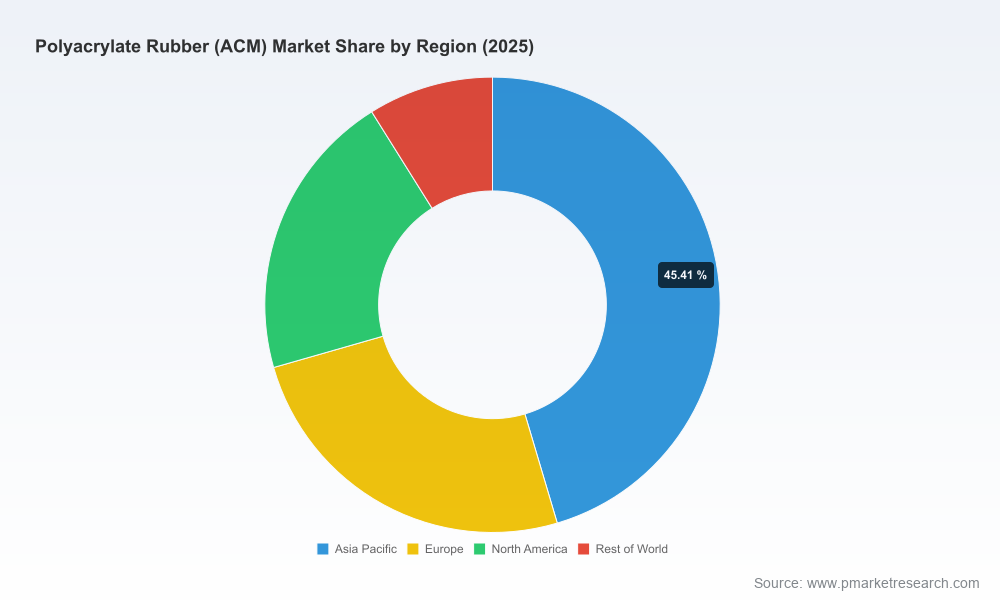

PW Consulting’s latest market study on polyacrylate rubber (ACM) synthesizes five years of historical performance and a seven-year forecast horizon to deliver an actionable perspective for executives planning capital allocation, sourcing strategies, product roadmaps and M&A through 2032. Built on a rigorous bottom‑up model, the report quantifies a market trajectory that expands from USD 922.45 Million in 2025 to an expected USD 1,032.0 Million in 2026 and reaches USD 1,306.65 Million by 2032 — a compound annual growth rate (CAGR) of approximately 5.1% across the forecast period. These headline metrics are a baseline for scenario planning; the value for corporate leaders lies in the report’s strategic translations of what that growth means for competitive advantage, cost exposure and timing of investments.

Polyacrylate Rubber Acm Market

2026 is a transitional year for ACM: demand drivers in engineered automotive elastomers continue to evolve while upstream volatility in acrylic monomers and regional regulatory scrutiny create episodic supply disruptions. Companies that act early to secure supply, optimize product portfolios, and hedge input cost exposure will lock in margins while competitors react to spot cycles.

Polyacrylate Rubber Acm Market

The market’s structural concentration — with the leading three players controlling a clear majority and the top five nearing double‑digit dominance — creates differentiated routes to scale, technology access and long‑term contracts with OEMs. For buyers and investors, understanding where an organization sits relative to these concentration dynamics is essential for negotiating terms and identifying partnership or consolidation opportunities.

Polyacrylate Rubber Acm Market

Our modelling shows that modest, predictable market growth masks heterogeneity across product, application and region. The gross figures above should therefore be used as strategic signposts rather than operational blueprints: the most valuable strategic moves will be those informed by high‑granularity data in the full report.

Upstream price movements remain a primary determinant of producer margins and pass‑through risk. Ethyl acrylate — a principal ACM feedstock — averaged roughly USD 1,397 per metric ton (about USD 1.40/kg) with regional variance in early 2026. Separately, major monomer suppliers implemented nominal price uplifts (for example, a USD 0.12/lb increase announced by a leading supplier in March 2026), demonstrating the persistent sensitivity of ACM economics to monomer pricing, energy and logistics factors.

Regulatory and operational events in China have influenced global short‑term supply availability. Mandated environmental inspections and staggered power‑load controls reduced local spot volumes in early 2026, contributing to a double‑digit percentage uptick in reported domestic ACM prices in March 2026. These episodes underscore the importance of multi‑source procurement and local inventory buffers for downstream manufacturers.

Despite episodic spikes, Q4 2025 saw notable preservation of producer margins owing to diminished volatility in key feedstocks. That transient stability created a limited window for contract renegotiation and inventory optimization ahead of the 2026 uplift in demand.

Market concentration metrics indicate a market where scale and technical depth matter. Leading specialty polymers and compounders have reinforced capabilities in high‑performance ACM grades (heat and oil resistance, low‑temperature performance, and durability for molded parts), while mid‑tier compounders focus on cost competitiveness and tailored formulas for Tier‑1 supply chains.

Representative competitors in the study illuminate strategic archetypes:

Technology leader: Firms with deep R&D and proprietary grades targeted at high‑temperature, oil‑resistant automotive seals and gaskets. These players command premium ASPs through performance differentiation and OEM qualification.

Compounder/processor: Players that combine compounding scale with logistics capabilities to serve global automotive programs, focusing on consistent supply to transmission and engine systems.

Regional specialists: Companies leveraging local feedstock access and proximity to large OEM clusters to win volume contracts despite narrower product breadth.

The competitive set covered in the report includes established Japanese and European technology leaders, specialty compounders from Asia and distribution partners operating in North America. Each profile maps capability, global footprint, core product strengths and strategic levers — but the full proprietary benchmarking and supplier scorecards are reserved for report subscribers.

Price actions by major monomer suppliers and regional price spikes in China signal that short‑term pass‑through risk remains real; organizations should stress‑test commercial agreements and consider indexed pricing clauses or strategic hedges.

Capacity additions by chemical and rubber process players during 2025/2026 indicate incremental supply, but lead times for specialized ACM grades and compounding capacity remain long. Tactical investments or offtake agreements executed in 2026 can therefore create durable access advantages.

Environmental enforcement in key manufacturing provinces, and power management controls, have become recurring operational risk vectors. Firms with geographic diversification or localized inventory strategies reduced exposure in prior cycles; these are effective playbooks to adapt in 2026.

Market sizing and scenario modelling (2020‑2032) with three transparent scenarios mapped to demand shocks, raw material volatility, and adoption curves in key downstream sectors.

Cost‑to‑serve and feedstock sensitivity analysis that quantifies margin impacts by input price moves and outlines hedging/contracting tactics.

Supplier stratification and risk heat maps, including a proprietary supplier scorecard for qualification, continuity risk and upgrade investment needs.

Commercial playbook templates: negotiation scripts, indexation clauses, recommended minimum inventory cover and trigger points for strategic purchases.

M&A and partnership pipeline analysis: candidate screening based on technical IP, capacity synergies and geographic footprint; modeled ROI thresholds and integration risk matrices.

Regulatory and sustainability impact assessment that identifies immediate compliance pressures and longer‑term substitution or reformulation risks driven by emissions and chemical use policies.

Prioritize supply resilience in contracting cycles. Locking multi‑year offtake agreements with staggered clauses and strategic safety stock will deliver outsized risk reduction relative to incremental inventory cost.

Accelerate qualification of premium ACM grades for safety‑critical automotive components. OEM timelines and warranty exposure favor early qualification and co‑development partnerships in 2026 and beyond.

Use the current window of relative feedstock stability to renegotiate cost‑sharing mechanisms and to build cross‑linkages with monomer suppliers for joint supply assurance programs.

Scan the competitive field for bolt‑on opportunities that provide immediate scale in compounding or local market access; target assets should be judged by integration speed and contract continuity rather than headline capacity alone.

Embed modular scenario‑based planning into annual budgeting to reflect the asymmetric impacts of episodic regional disruptions versus steady organic growth.

This briefing emphasizes strategic interpretation of headline market size and concentration dynamics. Detailed regional and application‑level splits, unit economics and proprietary supplier ratings are omitted here by design to preserve the value of the full research package and to encourage deeper engagement with transaction teams and procurement leaders.

PW Consulting recommends that executive teams commission a focused rapid diagnostic with our specialists if their 2026 capital, sourcing or product roadmap decisions require sub‑segment level inputs (for example, differentiated ASPs by automotive application or granular regional availability by grade). The diagnostic can be delivered in a two‑week sprint and includes tailored scenario runs using client feedstock exposure.

ACM is a mature but technically nuanced polymer market. The headline growth from USD 922.45 Million in 2025 to an expected USD 1,032.0 Million in 2026, and to USD 1,306.65 Million by 2032 at a 5.1% CAGR, signals a steady expansion that rewards disciplined execution rather than speculative capacity plays. In 2026, the intersection of feedstock cost dynamics, regional regulatory enforcement, and OEM product requirements will determine winners and laggards. PW Consulting’s full Polyacrylate Rubber (ACM) Market Report provides the granular decision tools — scenario models, supplier scorecards, commercial playbooks and M&A screening — required to translate these macro trends into durable competitive advantage.

For organizations preparing budgetary and strategic decisions in 2026, the question is not whether the market will grow, but who will capture the premium value created by managing supply risk, engineering differentiated grades and converting technical capability into long‑term customer commitments. Our full report is structured to convert that question into executable choices.

For detailed analysis of this topic, please visit the official page:Polyacrylate Rubber Acm Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com