Canine Oral Chewable Tablet Market Insights and Growth Trends

Other |

2026-06-25 12:36:49

PW Consulting’s new Industrial Belt Tensioner Market study (base year 2025; forecast 2026–2032) delivers a rigorous, decision-focused view of a market that is both mature in core segments and dynamic at the technology and supply-chain edges. With the global market assessed at USD 1,609.85 Million in 2025 and projected to expand to USD 1,775.08 Million in 2026 — following a compound annual growth rate (CAGR) of 6.08% through the forecast window — this report is designed to convert market intelligence into executable strategies for procurement, product development, M&A, and industrial operations planning in 2026 and beyond.

Industrial Belt Tensioner Market

Timing: 2026 is a pivot year. The market trajectory mapped in our model shows near‑term growth, intermittent softening, and further expansion toward 2032 — creating a narrow window for capturing share, optimizing manufacturing footprints, and adjusting procurement levers.

Industrial Belt Tensioner Market

Cost pressure: Pronounced volatility in key inputs (natural rubber and steel) — observed as swings of 20–35% annually in recent industry data — is elevating unit cost risk. The report translates those raw-material dynamics into scenario-based cost curves to support hedging and supplier contracting decisions.

Industrial Belt Tensioner Market

Regulatory momentum: Recent updates to EU emissions standards (March 2025) and parallel efficiency pushes in other jurisdictions are accelerating demand for energy-efficient tensioning solutions. Our analysis quantifies likely adoption vectors and product implications for engineering and aftermarket services.

Competitive balance: The market displays a moderate level of concentration (CR3 ~38.5%; CR5 ~52.7%), which means incumbent leaders retain pricing and channel advantages but there is meaningful room for agile challengers and niche specialists to scale via targeted investments or strategic partnerships.

Executive playbook: A tightly focused 10–point plan for senior leaders covering portfolio prioritization, capex triage, aftermarket monetization, and 12‑month supplier negotiation checklists.

Market sizing & methodology: Transparent bottom‑up and top‑down reconciliations, replacement-cycle models, OEM vs aftermarket demand mapping, and probability-weighted scenario outputs for 2026–2032.

Cost-to-serve and procurement toolkit: SKU-level margin sensitivity, raw-material exposure matrices, hedging hypotheses, and contract clauses that mitigate the 20–35% input volatility observed across rubber and steel markets.

Product roadmaps & R&D prioritization: Use-case driven guidance on where to invest in automatic tensioning systems, vibration-damping materials, and digital tension monitoring to align with emissions and efficiency regulations.

Supply chain and manufacturing playbooks: Location-agnostic models for footprint optimization, dual-sourcing strategies, inventory buffers calibrated for cyclical demand, and reshoring vs outsourcing decision matrices.

Commercial & go‑to‑market templates: Channel segmentation frameworks, pricing ladders, and aftermarket service propositions that convert higher uptime and predictive maintenance into recurring revenue.

Competitive & M&A intelligence: Target screening filters, valuation benchmarks, integration risk checklists, and three acquisition archetypes (bolt-on, capability buy, and geographic scale) with expected payback curves.

Risk register & mitigation playbooks: Regulatory, input-cost, demand-shift, and supply-disruption scenarios with trigger thresholds and contingency actions tailored to 2026 board-level decisions.

Data annex & modeling file: Machine-readable datasets and a model workbook that allow clients to run custom scenarios and validate hypotheses against our base case and downside/upside cases.

Transition toward energy efficiency: Regulatory pressure and corporate sustainability commitments are steering buyers to tensioning systems that reduce frictional losses and enable lower power draw across belt-driven assets.

Aftermarket monetization: With installed bases aging in certain end-markets, aftermarket parts, refurbishment, and condition-based services are becoming higher-margin opportunities for manufacturers and distributors.

Technology convergence: Sensors, condition monitoring, and automatic-adjustment mechanisms are increasingly embedded in new product designs — creating differentiation for suppliers who can offer integrated hardware + software solutions.

Input-cost management as a competitive lever: Firms that secure cost advantages through material substitution, long-term supply agreements, or vertical integration will achieve sustainable margin uplift.

Our competitive assessment synthesizes company disclosures, product portfolios, and go-to-market footprints to map strategic vectors across leaders, specialists, and regional challengers. Below are high‑level profiles and strategic implications for nine core players covered in the report.

Gates Corporation (Denver, CO, USA) — Broad portfolio depth: Gates’ extensive industrial lineup and engineering credentials make it a default partner for large OEMs; their strength is scale and product breadth, which supports multi‑region contracts and integrated service offerings.

Fenner Drives (Manheim, PA, USA) — Specialty systems and self-adjusting designs: Fenner’s T-Max rotary and linear tensioners are differentiated by ease of installation and low maintenance, positioning them well in retrofit and HVAC segments.

BRECOflex (Eatontown, NJ, USA) — Precision belt components: Focused on timing tensioners and idlers, BRECOflex competes on customization and tight-tolerance applications where reliability is mission-critical.

Lovejoy Inc. / Timken (Downers Grove, IL, USA) — Vibration mitigation specialist: Their elastomeric, self-adjusting solutions address uptime and shock-absorption needs in heavy-duty industrial applications.

Dayco (Roseville, MI, USA) — Product-line expansion and targeted heavy-duty launches: Recent 2025 expansions and new heavy-duty tensioners demonstrate a push to win in severe-duty and fleet applications; these moves increase aftermarket penetration and cross-sell potential.

Continental AG (Hanover, Germany) — Integrated accessory drive competence: Continental leverages systems-level engineering to offer tensioners and pulleys as part of broader drive solutions, which matters for OEMs seeking single-source suppliers.

Bando Chemical (Osaka, Japan) — Component systems for industrial belts: With strengths in auto-tensioners and components for ribbed and flat-belt systems, Bando is oriented toward system stability and long-run durability.

SKF (Gothenburg, Sweden) — Measurement and precision units: SKF’s portfolio combines tensioner units with measurement and maintenance tooling, positioning them well for condition-based service programs.

B&B Manufacturing (La Porte, IN, USA) — Custom and certified production: ISO-certified, with a focus on custom drives and tight turnaround for OEMs and repair shops.

Recent market activity reinforces these strategic postures. Dayco’s 2025 product-line expansion and heavy-duty launches signpost a concerted push into larger industrial niches. Trade-show showcases from other large suppliers underscore aftermarket and accessory drive diversification as a common strategic theme for 2026.

Immediate supply-risk assessment: Use our supplier-exposure matrix to identify top 10 SKUs by raw-material exposure and enter hedging or fixed‑price agreements for the near term.

Product roadmap re‑scoping: Prioritize three engineering initiatives that yield measurable energy-efficiency or predictive-maintenance benefits within an 18‑month R&D horizon.

M&A and partnership pulse-check: Screen targets that provide sensor integration, aftermarket channel access, or localized manufacturing to accelerate time-to-market under tightening emissions and efficiency requirements.

Commercial repositioning: Launch a service-bundled offering for aftermarket customers focused on availability and energy savings; use pilot programs in priority geographies to prove value before scaling.

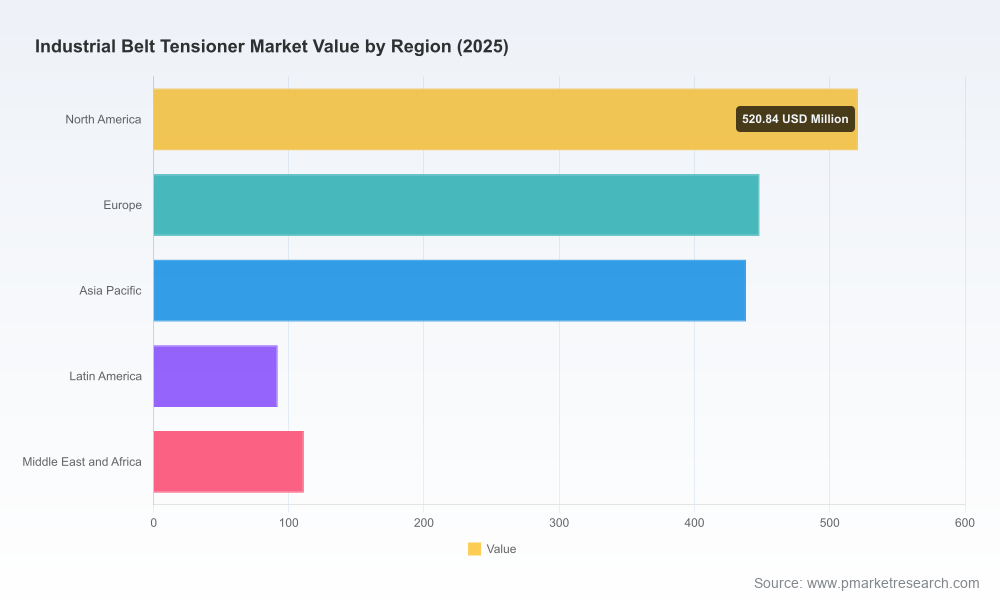

This briefing outlines the strategic value of our Industrial Belt Tensioner Market report for 2026 but deliberately omits granular segment-level figures and regional/application splits to preserve the research depth available in the full study. Clients and licensees receive the complete dataset, vendor scorecards, model workbook, and executable playbooks necessary to operationalize the insights described here.

To obtain the full report, dataset, and a complimentary briefing with one of our senior industry analysts, please visit the PW Consulting report page (link available via PW Consulting distribution channels). Our team will walk you through the scenario models and translate findings into a custom 90‑day action plan aligned to your objectives.

For detailed analysis of this topic, please visit the official page:Industrial Belt Tensioner Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com