Automatic Leak Detection Equipment Market 2026: Strategic Imperatives for Risk, Compliance, and Growth

PW Consulting is pleased to release an executive-level synthesis of our new market research brief on the global Automatic Leak Detection (ALD) Equipment market. As corporate leaders and public-sector decision-makers plan capital allocation and compliance programs for 2026, this briefing highlights the practical implications of the market’s trajectory, regulatory catalysts, competitive posture, and near-term actions that will govern value capture across industrial, utilities, and commercial end markets.

Automatic Leak Detection Equipment Market

Headline Market Outlook (data-driven)

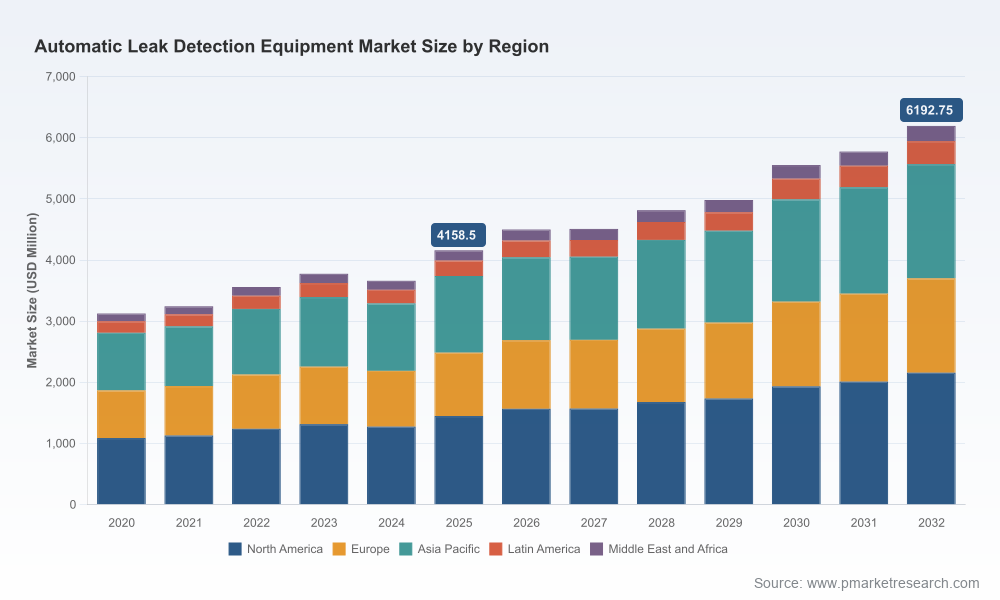

Between 2020 and 2025 the ALD equipment market expanded meaningfully, reflecting accelerated investment in infrastructure integrity and regulatory-driven retrofits. Our base-year analysis (2025) places the market at approximately USD 4.16 billion (revenue figures in USD Million). Under current assumptions and technology adoption curves, the market is forecast to grow at a compound annual growth rate (CAGR) of about 5.85% through the 2026–2032 period, reaching a mid-single-digit billion-dollar valuation by 2032. This is a volume and growth profile that justifies single-year strategic pivots for vendors and multi-year capital planning by end users.

Automatic Leak Detection Equipment Market

Why 2026 Is a Strategic Inflection Point

- Regulatory deadlines compress procurement cycles. Recent regulatory actions (notably U.S. EPA rules mandating ALD systems for certain refrigeration installations effective 2026 and phased requirements for existing high-charge equipment) create a narrow runway for compliance-driven procurement, installation, and validation. For organizations that service refrigeration, industrial process, and large commercial operations, 2026 is the year to transition from planning to execution.

- Pipeline safety standards are elevating demand for validated detection systems. Rules establishing performance standards for advanced leak detection programs for gas pipelines further expand the addressable market for pipeline operators and third-party service providers.

- Technology maturation enables commercial-scale monitoring. Advances in permanent acoustic monitoring, fiber optic sensing, and sensor-fusion analytics reduce total cost of ownership for continuous monitoring versus episodic survey approaches, accelerating O&M and managed-services opportunities.

Market Structure and Competitive Dynamics

The ALD market today is characterized by a moderate degree of concentration: the top three firms account for a meaningful share of revenue, while the top five collectively hold just over half the market. This structure signals two simultaneous realities: established vendors benefit from scale, certifications, and channel reach; yet the market remains open enough for focused challengers and specialist entrants to win pockets of value—especially where regulation or unique environmental conditions demand specialized technology stacks.

Automatic Leak Detection Equipment Market

Key vendor archetypes and competitive strengths we observed include:

- Industrial leak-test specialists: Firms with patented testing hardware and high-throughput bench systems that serve medical, automotive, and packaging OEMs are leveraging precision flow and mass-based methods to defend high-margin aftersales services and instrument replacement cycles. (Example: InterTech Development Company – Skokie, IL; see company resources for product line context.)

- Tank & pipeline monitoring incumbents: Vendors offering automatic tank gauging and digital pressurized line leak detection have deep channel relationships with fuel retail and storage operators and are positioned to grow with regulatory compliance programs. (Example: Veeder-Root – Simsbury, CT.)

- Acoustic/permanent monitoring specialists: Companies focused on correlating noise loggers, hydrophones, and permanent network monitoring are rapidly commercializing solutions for municipal and private water networks where non-revenue water and failure prevention are prioritized. (Example: GUTERMANN AG – Zug, Switzerland.)

- Gas-specific sensor manufacturers: Manufacturers of helium, hydrogen, refrigerant and vacuum leak detection equipment continue to be essential to manufacturing and service ecosystems where trace gas methods or portable gas detection are required. (Example: INFICON – Bad Ragaz, Switzerland.)

- Utility-focused vendors: Suppliers of ground microphones, acoustic correlators, and pipe locators maintain direct relationships with utilities and service contractors performing survey, pinpointing, and repair validation. (Example: Hermann Sewerin GmbH – Gütersloh, Germany.)

Recent Developments Shaping Vendor Strategy

- Product introductions in late 2025 and early 2026 have emphasized higher sensitivity and permanent monitoring capabilities for plastic pipe networks and high-speed precision testing for manufacturing QA/QC.

- Trade show participations and demonstrations at major industry events underscore vendors’ push to translate lab performance into field-validated workflows—an important credibility bridge for large buyers.

- Regulatory milestones—particularly the EPA’s 2026 ALD requirement for new large-charge refrigeration appliances and the PHMSA’s 2025 standards for pipeline leak detection—are driving both retrofit waves and specification changes in procurement documents.

What Our Report Contains: Practical, Decision-Ready Deliverables

PW Consulting’s full report is designed to be operationally actionable for C-suite, procurement, engineering, and compliance teams. Key deliverables include:

- Top-down and bottom-up market sizing, with forecast scenarios through 2032 that reflect regulatory adoption curves, retrofit schedules, and technology substitution effects;

- Vendor benchmarking and decision matrices that evaluate technology fit, TCO, certification status, and service model (capex sale vs. managed detection-as-a-service);

- Procurement playbooks and specification templates aligned to regulatory requirements and performance standards (including test protocols and acceptance criteria);

- Technical due diligence checklists for sensor fusion deployments (acoustic + fiber-optic + gas trace), integration requirements, and cybersecurity considerations for permanent monitoring networks;

- Case studies and retrofit pilots outlining implementation timelines, staffing, and O&M impacts for municipal water utilities, pipeline operators, and large refrigeration sites;

- Investment and M&A perspectives highlighting consolidation targets, partnership archetypes, and integration risks for strategic acquirers and specialist private equity.

Strategic Recommendations for 2026 Decision-Makers

For manufacturers and vendors

- Prioritize compliance-oriented product bundles that pair detection hardware with validated reporting and certification support—this reduces buyer friction for regulated customers.

- Invest in field validation capabilities and service contracts; buyers increasingly prefer suppliers who can demonstrate end-to-end performance in comparable operational environments.

- Pursue partnerships and selective bolt-on acquisitions to fill capability gaps in analytics, permanent monitoring, or channel coverage rather than chasing broad organic expansion alone.

For buyers—utilities, pipeline operators, large facility owners

- Accelerate audit and inventory programs to identify assets within regulatory scope and prioritize retrofits based on exposure and repair lead times—compliance windows are fixed and enforcement is increasing.

- Evaluate detection systems on total lifecycle cost and operator burden; capital cost parity is less important than maintainability, false-alarm rates, and integration with SCADA/asset management systems.

- Consider managed-service or performance-contract models to shift implementation and validation risks to vendors with demonstrable field track records.

For investors and strategic acquirers

- Target firms that combine sensor excellence with software-led analytics and recurring revenue—these are likely to command premium valuations as the market consolidates.

- Monitor regulatory enforcement patterns to identify near-term demand shocks that can justify accelerated deployment pipelines and service rollouts.

Risks and Sensitivities

The market’s upside is conditioned by several sensitivities: timing and enforcement of regulatory requirements, availability of installation and calibration labor, and the rate at which end users accept subscription-based monitoring versus capex procurement. Technology risk includes potential false positives/negatives in harsh environments and integration challenges across heterogeneous asset bases. Our scenario analysis quantifies these sensitivities and offers mitigation strategies—detailed models and contingency plans are provided in the full report.

Why PW Consulting’s Report Is Your 2026 Playbook

Organizations making decisions in 2026 need more than trendlines; they need executable plans. Our report combines proprietary market sizing, vendor capability matrices, procurement-ready templates, and field-proven implementation playbooks. It is designed to move teams from strategic intent to operational execution within regulatory windows and capital planning cycles.

Accessing Full Intelligence

This executive briefing deliberately highlights the report’s strategic contours and operational value while preserving the granularity that drives competitive advantage. Detailed segment-level breakdowns, regional and application revenue tables, vendor scorecards with quantitative scoring, and downloadable implementation templates are available in the full PW Consulting publication. For procurement teams, technical leads, and investors requiring the underlying datasets and model access, please visit our report page to request the complete analysis and supporting files.

Contact PW Consulting’s industry practice to schedule a briefing or to request a tailored workshop that maps this market intelligence to your organization’s roadmap and risk profile.

For detailed analysis of this topic, please visit the official page:Automatic Leak Detection Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com