The Rise of Commercial LED Strip Fixtures in Modern Lighting Solutions

Other |

2026-05-12 10:02:25

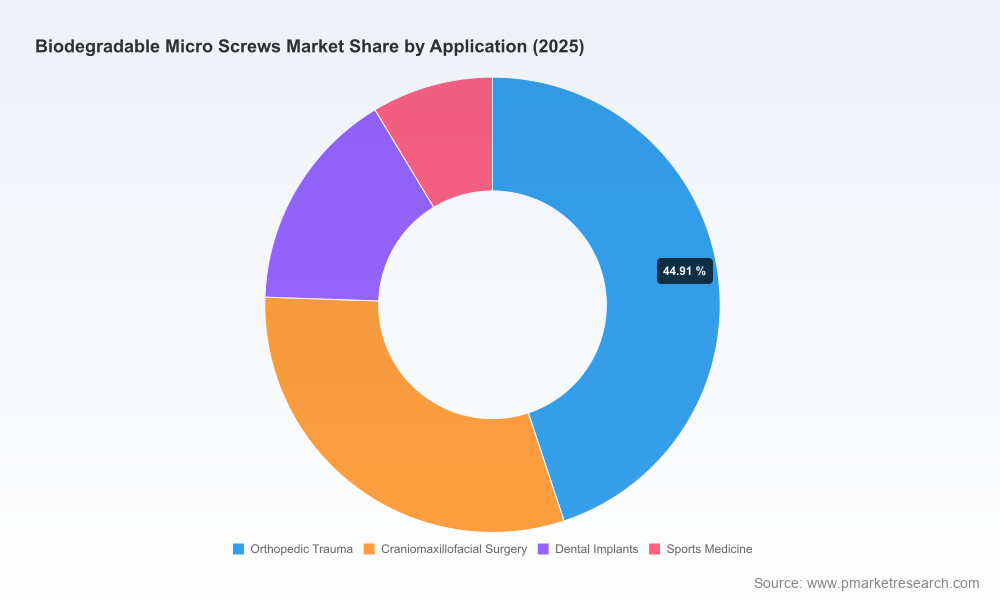

PW Consulting’s latest market research on the Biodegradable Micro Screws market delivers a tightly focused, decision-oriented intelligence package for executives planning 2026 strategies. The global market, which reached approximately USD 308.6 million in our base year (2025), is projected to expand at a compound annual growth rate (CAGR) of 8.45% through the 2026–2032 forecast horizon, reaching a substantive multi-hundred-million-dollar opportunity by 2032. This trajectory reflects a sustained shift in surgical practice toward temporary fixation solutions that eliminate implant removal, improve patient outcomes, and reduce downstream costs.

Biodegradable Micro Screws Market

Timing and momentum: 2026 is a pivotal year where regulatory progress, reimbursement signals, and raw-material dynamics converge to re-shape competitive advantage. Companies that align product, regulatory and commercial playbooks now will capture disproportionate share of the accelerating adoption curve.

Biodegradable Micro Screws Market

Risk-reward calibration: The market is neither a winner-takes-all segment nor fully fragmented — our concentration analysis shows a measurable presence of established innovators alongside agile challengers, creating windows for targeted M&A, licensing, and distribution partnerships to scale quickly.

Biodegradable Micro Screws Market

Upstream cost exposure: Feedstock and alloy markets are producing short- and medium-term price signals that will influence margin planning, sourcing strategies, and contract structures. Executives must integrate procurement scenarios into product and pricing models.

Actionable market sizing and scenarios: A transparent topline model that reconciles historical performance (2020–2025) with our 2026–2032 forecast, including upside/downside scenarios tailored to regulatory and reimbursement inflection points.

Go-to-market playbooks: Segmented commercial strategies for OEMs, distributors, and clinical partners that map sales channels, instrumentation compatibility needs, and surgeon engagement templates for high-impact use cases.

Regulatory & reimbursement matrix: A country-by-country decision tree highlighting likely pathways, expected review timelines, and reimbursement levers that materially affect time-to-revenue.

Cost and supplier benchmarking: Unit-level cost models, margin sensitives to feedstock prices, and a prioritized supplier shortlist for medical-grade biopolymers and magnesium alloys.

Clinical adoption and KOL playbook: Evidence-generation roadmaps (IDE/clinical trial designs, registries, real-world evidence) to accelerate surgeon adoption and payer recognition.

Competitive and IP landscape: Synthesized profiles of the leading incumbents and emerging players, with gap analyses identifying white-space opportunities in product form factors, instrumentation, and labeling claims.

M&A and partnership scorers: Transaction screening tools to value tuck-ins, platform buys, and geographic expansion targets based on commercial fit and regulatory tailwinds.

From 2020 to 2025 the market exhibited steady expansion driven by rising clinical adoption and product innovation. With a 2025 market size of roughly USD 308.6 million and an 8.45% CAGR through 2032, executives should assume a meaningful increase in absolute demand by the end of the forecast horizon. The report’s granular scenario planning translates that macro growth into priority revenue and investment milestones for 2026 — helping leadership set R&D budgets, commercial headcount plans, and regulatory investments with quantified confidence.

The competitive field is characterized by a mix of specialized pioneers, diversified orthopedics platforms, and technology-focused challengers. Our analysis highlights several archetypal players:

Specialist innovators with proprietary alloy or polymer platforms: Companies that have built differentiated material technologies and implant portfolios are using regulatory wins to convert clinical curiosity into routine use. Recent regulatory designations and approvals have materially de-risked commercialization paths for some innovators.

Diversified orthopedics platforms: Large OEMs leverage distribution breadth and surgeon relationships to bundle absorbable options with broader procedural portfolios, pressuring independent innovators on price and access.

Nimble challengers: Smaller, focused firms compete on instrumentation compatibility, narrow clinical niches (e.g., pediatric fixation), or cost-effective supply chain models.

Notable empirical signals to factor into 2026 strategies: regulatory milestones and reimbursement recognitions have recently accelerated for several technology leaders, creating practical windows for market entry or expansion. Our competitive chapter dissects product portfolios, go-to-market footprints, clinical evidence strength, and IP posture—yet deliberately omits proprietary market-share line-item disclosures in this public preview to preserve the full value of the paid report.

Regulatory acceleration: The period up to late 2025 saw targeted regulatory pathways used to expedite select biodegradable fixation devices. Firms that strategically pursue Breakthrough Device designations or De Novo pathways have shortened time-to-clinic, which translates into first-mover advantages in key markets.

Reimbursement signaling: Transitional payment arrangements and targeted CMS pass-through recognitions for specific device constructs have de-risked U.S. adoption in certain indications. Our reimbursement playbook quantifies the impact of these mechanisms on 12- to 36-month revenue ramps.

Material selection and procurement will be decisive factors in 2026. Medical-grade biopolymers and magnesium alloys each present distinct supply and cost dynamics:

PLA and medical-grade polymer costs are fluctuating by region, reflecting feedstock and conversion pressures. Recent market checks show material pricing differentials by geography that will affect landed cost models and product pricing strategies.

Magnesium alloy supply is supported by a growing upstream market that has expanded in recent years, creating both opportunity and competition for downstream screw manufacturers who rely on consistent alloy supply and certification processes.

Our supplier benchmarking and cost-model modules provide executable procurement strategies including hedging approaches, dual-sourcing templates, and cost-to-serve analyses to protect margins while maintaining quality and certification compliance.

Surgeon acceptance of biodegradable micro screws depends on predictable resorption, instrumentation compatibility, and demonstrable patient benefits such as reduced reoperation rates. The report outlines prioritized evidence-generation paths—ranging from focused registries to randomized trials—that maximize clinical impact for constrained R&D budgets. We map KOL networks and delineate the minimal viable evidence package required to change institutional procurement decisions in targeted specialties.

Given the market’s intermediate concentration (our concentration metrics indicate leading firms capture a material but not absolute share), acquisition and partnership remain high-ROI strategies. The report includes a transaction matrix that helps executives evaluate targets against five dimensions: technology fit, regulatory status, clinical evidence, commercial channel synergy, and post-close integration complexity. For 2026, we identify partnership archetypes that unlock rapid market access without full-scale inorganic commitments.

Set a 12-month regulatory and reimbursement roadmap aligned to product filings that target high-return geographies and indications.

Re-calibrate procurement and pricing models to current feedstock scenarios; implement at least two supplier-risk mitigations for each critical material class.

Prioritize clinical studies that reduce time-to-adoption among high-volume surgeons; use registry data for payor conversations to shorten reimbursement timelines.

Evaluate targeted acquisitions and licensing deals using the PW Consulting transaction scorers to accelerate capability gaps, particularly in instrumentation and evidence generation.

This preview highlights core strategic imperatives but intentionally omits detailed split-level market allocations and proprietary company-specific revenue estimates that form the commercial backbone of our paid product. The full report contains the granular segmentation models, downloadable financial models, company scorecards, and an interactive playbook that enables executives to stress-test choices across a range of realistic 2026 scenarios.

For leadership teams ready to convert market growth into measurable competitive advantage in 2026, PW Consulting’s full Biodegradable Micro Screws Market report is a practical tool: it converts macro trends and regulatory milestones into stepwise commercial actions, procurement safeguards, and M&A lenses. Contact PW Consulting to access the complete dataset, scenario models, and tailored advisory briefings that will inform your 2026 strategic plan.

For detailed analysis of this topic, please visit the official page:Biodegradable Micro Screws Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com