Game Testing Service Market — A Strategic Preview for 2026 Decisions

PW Consulting’s latest Game Testing Service Market report (base year 2025; forecast 2026–2032) is designed as a decision-grade playbook for executives, procurement leaders and studio heads preparing investments and sourcing strategies in 2026. The market has moved beyond incremental QA contracts: it is now a high-velocity service ecosystem shaped by automation, platform certification complexity, and regulatory scrutiny. Our analysis synthesizes market sizing, competitive dynamics, and pragmatic sourcing frameworks so leaders can act with conviction — while preserving the full dataset and proprietary segment-level intelligence behind our paywalled report.

Game Testing Service Market

Executive snapshot: scale, growth trajectory and what it means

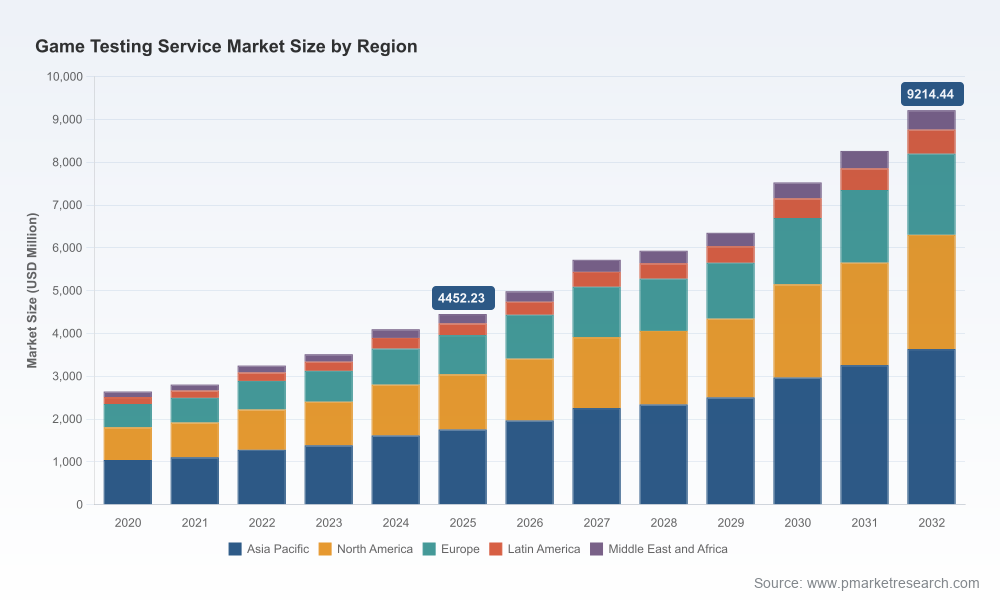

The global game testing services market has demonstrated robust expansion over the last half-decade and continues to scale as games themselves become more complex, live-service driven and regulated. PW Consulting’s market model shows a multi‑billion dollar market in 2025, with a compound annual growth rate (CAGR) of approximately 10.95% across the 2026–2032 forecast window. Under our base scenario, the market nearly doubles in scale over the forecast period, reflecting a sustained uplift in third‑party testing demand driven by mobile proliferation, cloud/VR/AR maturation, and intensifying platform and regulatory requirements.

Game Testing Service Market

For 2026 corporate strategists, that trajectory implies two realities: (1) unit pricing pressure combined with rising absolute spend as studios invest in automation, compliance and device/lab coverage; and (2) growing value for vendors who can combine deep technical testing with platform certification, localization and security expertise. These trends force a rethink of classic make-versus-buy decisions and demand new procurement guardrails.

Game Testing Service Market

Why 2026 is a strategic inflection point

- AI and automation move from experimental to operational. Leading providers are deploying AI-driven regression and playtesting capabilities to reduce manual cycles and accelerate release cadences. This is changing the economics of regression testing and shifting value capture toward vendors that can operationalize machine-assisted QA at scale.

- Regulatory and platform complexity increases vendor value. Compliance checks — spanning data privacy, monetization mechanics and child-protection rules — are no longer peripheral. Studios increasingly rely on specialist testers who embed regulatory checklists and platform certification workflows into their QA pipelines.

- Service breadth matters. Clients prefer partners offering integrated testing, localization QA, certification support and, in some cases, co-development. Buyers value single-vendor coordination of cross-functional delivery for global launches.

- Consolidation and specialization co-exist. Market leaders are consolidating capabilities through tuck-ins and platform launches, while niche specialists capture premium margins in areas like compatibility across device matrices and VR/AR performance testing.

Competitive landscape — what the leading providers are doing (and why it matters)

The competitive map is diverse: a handful of large, global service providers coexist with regional specialists and engineering-led boutiques. The market shows a moderate level of concentration: top-tier providers collectively command substantial share, but there remains meaningful opportunity for differentiated specialists.

- Keywords Studios (Dublin) continues to position itself as the largest, full-spectrum provider. Recent strategic moves — including a 2025 acquisition to strengthen mobile testing capabilities and the early‑2026 launch of an AI-assisted testing platform — signal a platform-first play to capture regression and large-scale QA spend. For clients, Keywords represents a low-friction supplier for global AAA rollouts and complex certification pipelines.

- Lionbridge Games emphasizes localization and linguistic QA alongside compliance services. Its strengths are global delivery models and established relationships with publishers launching across multiple markets, making it an attractive partner for studios prioritizing market-specific releases.

- Testronic Labs and PTW / Side offer deep certification and pre‑launch expertise; both have invested in multi‑platform capabilities and co‑development services that smooth the path to platform approval. These providers are often chosen where platform certification risk is a gating factor for release timelines.

- GlobalStep, Quantic Lab, and engineering-led boutiques such as iXie Gaming and TestMatick differentiate through device labs, automation engineering and bespoke tooling tailored to publishers and mid‑sized studios.

- Regional specialists — including firms with roots in Eastern Europe, India and the Baltics — compete on delivery flexibility, cost efficiency and localized QA expertise. Their value proposition is strongest in high-volume mobile testing and compatibility coverage where modular engagement models are preferred.

Recent strategic partnerships and product launches underscore broader structural shifts. The emergence of vendor-built AI testing platforms and alliances between automated tooling vendors and service providers are accelerating workflow integration and eroding barriers to near‑continuous QA.

What PW Consulting’s report delivers — practical, procurement-ready content

Our report is intentionally operational. Beyond headline market figures, it provides the following deliverables designed to be immediately actionable for 2026 planning cycles:

- Proprietary market model and sensitivity analyses — scenario views for conservative, base and upside growth paths (2026–2032).

- Vendor assessment framework — scoring across technology, delivery footprint, platform certification experience, security/compliance capabilities and automation maturity.

- Go‑to‑market and sourcing playbooks — build vs buy decision matrices, phased onboarding templates, SLAs and performance KPIs tailored to live-service and launch-driven development rhythms.

- Procurement negotiation levers — recommended contract structures, price‑vs‑outcome tradeoffs, and a checklist for embedding compliance and data governance obligations into SOWs.

- Use cases and execution plans — from scaling compatibility testing for device fleets to integrating AI-assisted regression bots into CI/CD pipelines.

- Operational dashboards and KPI templates — for measuring defect leakage, test automation coverage, time-to-certification and ongoing cost-to-serve.

To preserve competitive integrity and demonstrate our methodology, the report provides a reproducible modelling workbook and vendor scorecards. Segment-level datasets, regional splits and price benchmarks are part of the full intelligence package and are available on our website for subscribing clients.

Strategic recommendations for 2026 decision-makers

Based on our market model and vendor assessments, PW Consulting recommends a three-track strategic approach for enterprises entering 2026:

- Modernize QA through selective automation: Prioritize investment in AI-assisted regression and playtesting where repeatability and scale exist, while retaining manual expertise for exploratory testing, compliance checks and platform certification. Structure vendor contracts to share automation ROI and incentivize tooling adoption.

- Adopt a tiered sourcing model: Combine strategic relationships with a small number of global, full-service providers for major launches and platform work, and retain specialized, regional partners for high-volume compatibility and localized QA. This hybrid model balances risk, time-to-market and cost.

- Embed compliance and security into the QA lifecycle: Make regulatory and platform requirements a defined gate in development sprints. Require vendors to demonstrate repeatable compliance test cases and to integrate evidence trails for certification authorities.

- Make vendor selection outcome-centric: Shift RFPs from output-based metrics (test hours, device counts) to outcome-based KPIs (defect escape rates, time-to-certification, automation coverage). Use vendor scorecards to weight engineering capability and platform experience alongside price.

- Factor in total cost of ownership: Evaluate vendor bids on end-to-end cost, including rework, certification cycles and live‑operations support rather than only headline unit rates. Prioritize partners who can reduce cycle times and integration friction.

Risks and watch‑items for the next 18 months

- Tooling lock-in: Vendors that bundle proprietary automation may accelerate short-term efficiency but create long-term dependence. Insist on interoperability and CI/CD integrations in contract terms.

- Regulatory changes: Evolving privacy and consumer protection rules will increase compliance testing scope; maintain a regulatory watch and require vendors to commit to rapid update pathways.

- Talent and delivery resilience: Deliveries dependent on single-region labor pools are vulnerable to geopolitical and labor-market shocks. Diversify delivery footprints and require continuity plans.

- Quality erosion through commoditization: As automation commoditizes basic test coverage, differentiation will shift to complex engineering capabilities and domain expertise. Reallocate spend accordingly.

How to use this report in 90 days

- Week 1–2: Align stakeholders on priorities — map certification, localization and live-ops risks to release timelines.

- Week 3–6: Run vendor RFx using our scorecard templates; include automation and compliance as weighted criteria.

- Week 7–10: Pilot a blended sourcing model for a discrete title or feature set; instrument KPIs from our dashboard templates.

- Week 11–12: Scale the approach across the studio portfolio, negotiate enterprise SLAs and commence automation co-investment with a preferred vendor.

Conclusion — why PW Consulting’s market intelligence matters for 2026

Game testing is no longer a back‑office checkbox. By 2026 it will be a strategic lever shaping speed-to-market, regulatory risk and player experience. PW Consulting’s report translates market-scale dynamics (including robust mid‑term growth at an approximately 10.95% CAGR) into executable vendor strategies, procurement tools and risk mitigations tailored to the realities of modern game development.

We have deliberately framed this article as a preview: it communicates our analytical depth and the operational output clients receive while reserving the report’s granular segment-level tables, regional splits and vendor share data for the full deliverable. For the complete dataset, vendor scorecards, pricing benchmarks and the reproducible market model, visit PW Consulting’s Game Testing Service Market report page or contact our client services team to schedule a briefing.

For detailed analysis of this topic, please visit the official page:Game Testing Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com