Hydrolyzed Formula Milk Powder Market: Strategic Intelligence for 2026 Decision-Making

PW Consulting’s latest market study on the Hydrolyzed Formula Milk Powder market equips executive teams with the actionable intelligence required to navigate a rapidly evolving infant nutrition landscape in 2026. Drawing on a robust historical base (2020–2025) and forward-looking projections (2026–2032), the report synthesizes market sizing, competitive positioning, regulatory inflection points and supply‑side constraints to support portfolio, go‑to‑market and M&A decisions.

Hydrolyzed Formula Milk Powder Market

Market snapshot and trajectory

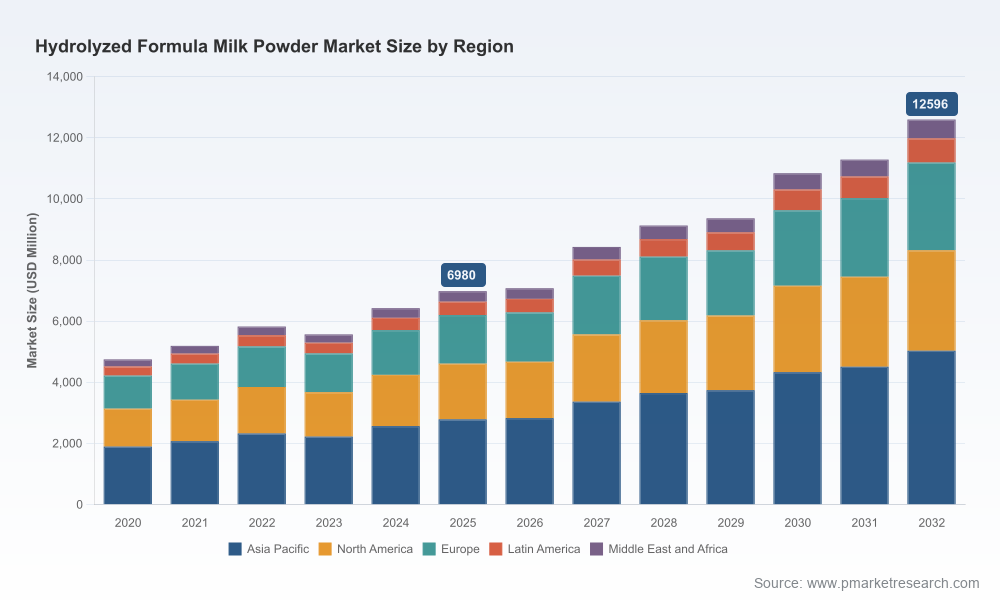

The global hydrolyzed formula milk powder market demonstrated resilient expansion through recent cycles, expanding from USD 4,750.5 million in 2020 to USD 6,980.0 million in 2025. Our forecast indicates the market will continue to expand at a compound annual growth rate (CAGR) of 8.8% over the 2026–2032 period, reaching approximately USD 12,596.0 million by 2032. That growth profile reflects a combination of demand-side drivers (heightened atopy awareness, clinical recommendations for hypoallergenic feeding where indicated, and rising early‑life health investment) and supply-side evolution (ingredient innovation, expanded hydrolysate manufacturing capacity and targeted channel expansion).

Hydrolyzed Formula Milk Powder Market

Historical dynamics reveal a market that absorbed episodic shocks and structural shifts: the recovery phases in 2024–2025 followed a brief correction in 2023, underscoring how channel disruptions, regulatory updates and raw material availability can transiently reorder demand. For executives, the headline is clear—this is a mid‑single to high‑single digit growth market with periodic volatility tied to regulations, ingredient cycles and competitive re‑pricing.

Hydrolyzed Formula Milk Powder Market

What this report contains (practical, execution‑oriented)

- Comprehensive market sizing and time‑series (2020–2025 historical; 2026–2032 forecast) with scenario analyses calibrated to regulatory and raw‑material sensitivity.

- Segmentation frameworks by product type, distribution channel and region with cross‑tabbed demand drivers and profitability overlays (note: the press release intentionally omits granular segment tables; full segmentation is accessible in the report portal).

- Supply‑chain mapping from dairy raw materials through hydrolysis processing to finished‑goods packaging, including cost buckets and bottleneck risk scoring.

- Regulatory and safety dashboard covering recent rulings and expected policy shifts, plus templates for label and compliance readiness for major markets.

- Competitive intelligence dossiers on leading players, ingredient suppliers and private‑label specialists, including capability maps, route‑to‑market comparisons and likely strategic moves.

- Actionable strategic playbooks: product prioritization (R&D roadmaps), channel optimization (pharmacy vs. e‑commerce vs. retail), pricing tactics, and M&A/partnership screening criteria.

- Primary research methodology, supplier network interviews, and a prioritized list of diligence questions for commercial and technical teams.

Why this matters for 2026 corporate strategy

- Portfolio rationalization: With the hydrolyzed category expanding at an 8.8% CAGR into 2032, firms must decide which sub‑segments merit incremental R&D investment versus which should be defended via operational excellence or price tactics. The report gives a decision matrix for that triage.

- Regulatory preparedness as a competitive moat: Recent regulatory updates in the EU (December 2025) amending protein requirements for hydrolyzed formulas and ongoing U.S. oversight signal that compliance is a continuing cost and a source of market access advantage. Firms that embed regulatory forecasting into product development will shorten time‑to‑market and reduce recall risk.

- Supply‑chain resilience: Milk‑based hydrolysates—particularly whey hydrolysate—are projected to account for the dominant share of protein hydrolysate ingredient consumption in 2026. That concentration creates both scale advantages for incumbent dairy suppliers and exposure for finished‑goods manufacturers; our report models inventory strategies and dual‑sourcing options to mitigate price and availability shocks.

- Channel and private‑label dynamics: The category is influenced by a mix of branded specialty products and retailer private labels. Our analysis provides negotiation playbooks for retailers and manufacturers that optimize margin capture while protecting brand equity.

- M&A and partnership signals: High market concentration among the top players (our analysis shows the top three firms control a material majority of market revenue, with the top five even more dominant) creates pockets of attractive consolidation targets—either technology owners (hydrolysis capability, peptide characterization) or regional scale players with distribution reach.

Competitive landscape: who shapes the market

The category is anchored by multinational infant‑nutrition brands that combine clinical credibility, broad distribution and scale manufacturing with specialist ingredient suppliers that underpin product formulation.

- Nestlé: A global leader with clinically positioned extensively hydrolyzed formulations, benefiting from broad product reach and R&D investment in hypoallergenic nutrition. Their portfolio illustrates the premium, clinically validated positioning that commands trust in markets where pediatric guidance drives purchase.

- Danone (Nutricia): Operating with dedicated hypoallergenic brands and an expanding U.S. presence, Danone leverages clinical trial evidence and channel partnerships to accelerate adoption in pediatric and specialty pharmacy segments.

- Mead Johnson (Reckitt) and Abbott Nutrition: These U.S. incumbents combine hospital, clinical and retail channels to secure category leadership in key markets. Their product breadth—spanning extensively hydrolyzed therapeutic formulas and specialized bases—creates a high‑barrier competitive set for newcomers.

- Perrigo and private‑label manufacturers: Their scale in contract manufacturing and store brands exerts downward pricing pressure while offering retailers margin flexibility. For suppliers, winning private‑label contracts can fill plant utilisation but compress margins.

- Regional and specialty brands (Meiji Group, HiPP) and ingredient suppliers (Arla Foods Ingredients, FrieslandCampina): These players sustain regional preferences and provide the whey and hydrolysate ingredients that make product differentiation possible. Ingredient firms are strategic partners in formulation and a source of technological differentiation.

Collectively, the competitive set demonstrates a layered ecosystem: brand owners compete on clinical evidence and channel access; private labels compete on value and availability; ingredient suppliers shape technological trajectories. Our report includes actionable matrices that map each named company’s strengths, typical strategic playbook, and likely next moves—detail we intentionally omit from this release to preserve the tactical value of the full study.

Regulatory and raw‑material dynamics—implications for 2026 actions

- Regulation: The European Commission’s December 2025 update to protein requirements for hydrolyzed formulas introduces new compliance categories effective January 2026. In parallel, U.S. labeling rules and FDA oversight continue to govern permissible claims tied to hypoallergenic benefits. Companies should prioritize label audits, dossier updates and post‑market surveillance protocols to avoid market interruptions.

- Ingredients: Milk‑based hydrolysates (notably whey hydrolysate) are poised to remain the dominant input in 2026, reinforcing the importance of long‑term offtake agreements, capacity investments, and technical co‑development with ingredient suppliers to secure formulation flexibility and price predictability.

- Quality and traceability: Increasingly stringent regulatory expectations and consumer scrutiny mean traceability and batch‑level quality documentation are commercial differentiators. Early investment in digital traceability and GMP upgrade programs will shorten certification lead times and reduce disruption risk.

How to use this report in 90, 180 and 360 days

- 90 days: Run rapid portfolio health checks using our prioritization tool—identify SKUs to accelerate, maintain, or sunset; initiate label and regulatory gap analyses for urgency markets.

- 180 days: Negotiate or renegotiate supplier contracts for hydrolysate inputs; pilot dual‑sourcing for critical ingredients; commence targeted clinical or consumer studies that support differentiated claims.

- 360 days: Execute channel expansion pilots in higher‑growth markets and finalize at least one strategic partnership or bolt‑on acquisition to secure formulation IP or distribution reach, guided by our M&A screening criteria.

What’s intentionally withheld here (and why)

To preserve the consultative value of the full study, this press summary omits the granular segmentation tables and specific regional/application share figures that decision teams use for financial modeling and target setting. Our report contains those tables, precise market split figures and downloadable financial models on the report landing page—access to which provides the full dataset needed for board‑level deliberations and transaction diligence.

Conclusion and next steps

For executives preparing 2026 strategies, the hydrolyzed formula milk powder market represents a compelling growth corridor—characterized by durable demand, regulatory momentum and concentrated competitive dynamics. Success will depend on integrating regulatory foresight, ingredient risk management and channel strategy into product and capital allocation decisions. PW Consulting’s full report delivers the data, diagnostic tools and playbooks required to convert market trends into defensible, high‑return actions.

Contact PW Consulting to request the full report, gain access to the segmentation datasets, and schedule a strategy workshop tailored to your organization’s market position.

For detailed analysis of this topic, please visit the official page:Hydrolyzed Formula Milk Powder Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com