Oligonucleotide Therapeutics Market: Size, Share, and Future Growth

Other |

2026-06-09 09:05:13

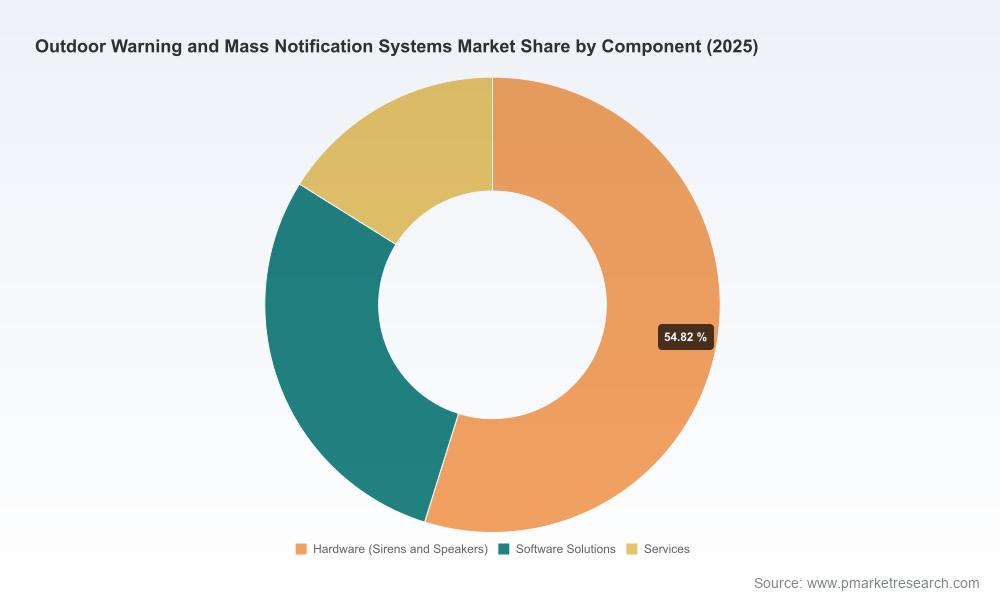

As communities, campuses, industrial sites, and government agencies reassess resilience in the face of more frequent extreme weather, civil security risks, and evolving regulatory demands, the outdoor warning and mass notification systems market is entering a decisive phase. PW Consulting’s latest market research—anchored on 2025 as the base year and projecting to 2032—shows a clear, investment-grade growth trajectory. The global market recorded USD 2,778.0 Million in 2025 and is forecast to expand at a compounded annual growth rate (CAGR) of 7.42% across the 2026–2032 period, reaching an expected USD 4,584.88 Million by 2032.

Outdoor Warning And Mass Notification Systems Market

Macro momentum: The market’s mid-single-digit-plus CAGR reflects stable demand driven by public funding programs, regulatory harmonization around digital alerting (IPAWS, polygon-based alerting), and heightened procurement activity from critical infrastructure operators.

Outdoor Warning And Mass Notification Systems Market

Decision window: 2026 is a pivotal year—legislative initiatives and grant programs are translating policy into capital deployments. Public-sector grant flows and revised federal standards will shape procurement timelines and technical specifications for the next procurement cycle.

Outdoor Warning And Mass Notification Systems Market

Integration focus: Purchasers increasingly treat outdoor warning assets as part of an orchestration layer (giant voice, sirens, IP speakers) within broader multi-channel emergency communications architectures. That raises priorities around interoperability, cybersecurity, data sovereignty, and lifecycle total cost of ownership (TCO).

Strategic buyer playbook — A procurement checklist that links mission requirements (coverage, intelligibility, integration) to procurement clauses, testing protocols, and maintenance SLAs that public safety and corporate buyers can drop into RFPs.

Technology and deployment roadmap — Comparative evaluation of hardware (electro-mechanical sirens, high-powered speakers), software orchestration layers, and managed services; migration pathways for IPAWS-compliant and polygon-capable solutions; and guidance for hybrid on-premise/cloud models under data sovereignty constraints.

Vendor selection framework — A scoring matrix combining technical fit, systems integration capability, lifecycle support, and the often-underappreciated components of installation, frequency planning, and community engagement for public deployments.

Operational scenario planning — Playbooks for common incident types (severe-weather, industrial hazmat, active shooter, evacuation) with recommended messaging sequences, siren/voice mixes, and interagency coordination protocols to maximize human response rates and reduce false alarms.

Financial and risk models — TCO templates, funding pathway mapping (grant layering, municipal bonds, public-private partnership structures), and sensitivity analyses that quantify the impact of device obsolescence cycles and maintenance backlogs.

Regulatory and funding tracker — Up-to-date analysis of funding vehicles and regulatory shifts—showing where federal programs and FCC/IPAWS mandates materially change procurement criteria and interoperability expectations.

Executive briefings and implementation sprints — A phased guide for rapid pilots, scaled rollouts, and transition management that preserves continuity of legacy warning while enabling modernization.

The market exhibits moderate concentration: the three largest players account for roughly one-third of market revenue, while the top five approach just under half of total market value. This structure creates opportunity for specialist suppliers and systems integrators that combine domain-specific acoustic engineering with software orchestration and managed services.

Legacy manufacturers with scale (e.g., well-known siren and giant-voice producers) retain advantages in installed-base depth, field service networks, and regulatory certifications. These incumbents continue to defend public-sector contracts by bundling hardware with integration to national alerting ecosystems.

Specialist acoustic and long-range voice vendors are winning new use cases where intelligibility and directed messaging matter—military bases, campuses, and remote communities—by emphasizing voice clarity, encryption, and mobile-deployable assets.

Large systems integrators and diversified industrial technology firms are positioning on the orchestration layer, selling cross-domain solutions that integrate audible warning with visual, cellular SMS, and IoT sensor feeds.

Incumbent vendors: Product obsolescence management is now a frontline commercial theme. Buyers should require clear end-of-life roadmaps and migration allowances in contracts to avoid stranded systems and unbudgeted refresh cycles.

Specialist innovators: Emphasize differentiated capabilities—voice intelligibility at range, encrypted networked deployments, and integrated mobile trailer systems—to capture niche pockets of demand where lifecycle and performance metrics trump price.

Systems integrators and platform providers: Focus on open APIs, standards-based IPAWS/FFIEC/FCC compliance, and edge-to-cloud architectures that reconcile on-premise sovereignty requirements with cloud-based orchestration efficiencies.

Targeted public funding: Recent allocations and grant programs are lowering the cost barrier for municipalities and counties to modernize outdoor warning fleets, creating a predictable near-term procurement pipeline for vendors that can meet compliance and reporting requirements.

Standards and integration mandates: Upgrades to national alerting dashboards and polygon-aware alerting requirements are forcing a refresh of system interfaces and message templates—creating upgrade demand among buyers seeking continuous IPAWS compatibility.

Additionally, emerging legislative proposals aimed at subsidizing rapid deployment and sensor integration are likely to accelerate replacement cycles in jurisdictions that move quickly to access funds. For buyers, this translates to a narrow window in 2026 to align technical specifications with funding criteria.

Order and deployment activity from municipal and county governments demonstrates ongoing field modernization and a preference for solutions that prioritize vocal clarity and tested interoperability.

Supply-side lifecycle moves—such as last-time-buy notices for legacy IP-enabled devices—signal active product rationalization. Buyers should demand clearly defined support and backwards compatibility terms in procurement documents.

Localized public-sector testing programs are validating whole-system performance (coverage, intelligibility, backup power), creating reference cases that influence neighboring jurisdictions’ procurement choices.

Buyers (public and private): Adopt a two-track procurement strategy—(1) near-term remediation to address critical coverage gaps using proven devices and (2) a phased modernization path that prioritizes interoperability, lifecycle economics, and community engagement. Insist on IPAWS compliance, polygon alerting compatibility, and explicit cyber-hardening provisions.

Vendors: Differentiate on system integration services and lifecycle assurance. Publish migration and backward-compatibility roadmaps, and create financing structures or grant-assistance partnerships to help cash-constrained jurisdictions convert funding into deployed systems.

Investors and integrators: Look for consolidation targets that combine acoustic hardware expertise with cloud-native orchestration software, or services firms that can scale field maintenance across wider geographies.

Testing and standards bodies: Prioritize intelligibility metrics and multi-channel scenario testing as procurement thresholds; standardized test protocols reduce buyer uncertainty and speed contracting cycles.

It reduces procurement friction: By supplying contractual language, test protocols, and a validated scoring matrix, the report shortens RFP cycles and reduces bid rework.

It de-risks technology choices: The roadmap and migration scenarios model lifecycle costs under multiple technology and funding permutations to surface hidden refresh and integration costs.

It aligns funding to delivery: The report maps federal and state grant vehicles to realistic deployment timelines and compliance checklists, helping teams time requests to funding windows.

It preserves strategic ambiguity where it matters: We expose market growth, concentration patterns, regulation, and vendor positioning while omitting granular regional and application splits in this preview—deliberately. This “trailer” approach demonstrates the report’s analytical depth while encouraging stakeholders to access the full repository for transaction-ready intelligence.

For procurement teams, systems integrators, and executive leadership preparing 2026 budgets, the immediate priorities are clear: align specifications to evolving federal requirements; require robust lifecycle assurances; and sequence pilot-to-scale deployments that capture available grant funding. PW Consulting’s full report provides the granular regional, component, and end-user segmentation, vendor scorecards, and deployable contract language needed to move from intent to award—without the friction of rework or compliance risk.

Access the full market study to obtain the detailed segmentation, ranked vendor profiles, and plug-and-play procurement artifacts necessary to execute a 2026 strategy that captures both resilience objectives and fiscal discipline.

For detailed analysis of this topic, please visit the official page:Outdoor Warning And Mass Notification Systems Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com