Antimicrobial Additives: The Science Behind Safer, Longer-Lasting Products

Art |

2026-04-20 11:26:42

As organizations accelerate cloud transformation and hybrid work architectures mature, the Desktop Virtualization Software market has become a strategic battleground for CIOs, security leaders, and infrastructure vendors. PW Consulting’s latest market research (base year 2025; historical window 2020–2025; forecast 2026–2032) synthesizes quantitative trajectories with actionable frameworks designed to inform investment, procurement, and go-to-market decisions throughout 2026. Our analysis spans commercial dynamics, supplier economics, regulatory risk, and operational playbooks — revealing what successful adopters and product leaders must prioritize next.

Desktop Virtualization Software Market

The desktop virtualization market has evolved rapidly over the last half-decade, expanding from a multi-billion dollar industry in 2020 to a substantially larger market by our 2025 base year (reported in USD Million). PW Consulting projects continued acceleration through the forecast window to 2032, underpinned by a compound annual growth rate of 12.38% (2026–2032). This growth trajectory reflects sustained enterprise demand for secure remote access, desktop consolidation, and cloud-native delivery models.

Desktop Virtualization Software Market

Market structure matters: concentration metrics show that the top three vendors capture a meaningful majority share of revenue, while the top five consolidate an even larger portion. These concentration dynamics increase the strategic importance of vendor selection, interoperability, and exit options for large enterprises and systems integrators.

Desktop Virtualization Software Market

Migration inflection: Many organizations that adopted pilot or partial VDI strategies during 2020–2024 are entering full-scale migration or refresh cycles in 2026. Decisions made this year — platform architecture, licensing model, and operational ownership — will set a 3–5 year cost and capability profile.

Security and compliance convergence: Regulatory scrutiny and sector-specific compliance (healthcare, finance, government) increasingly drive architecture choices. Enterprises must align isolation, data residency, and auditability requirements with vendor roadmaps and third-party assurance.

Operating model reset: The total cost of ownership calculus is shifting from pure infrastructure CAPEX to blended cloud OPEX, licensing, and people costs (including security and SRE functions). Detailed TCO scenarios are now table stakes for board-level signoff.

Historical revenue trends demonstrate robust expansion between 2020 and 2025, followed by a steady acceleration anticipated through 2032 under our base forecasts. The quantitative pattern — derived from recurring license revenues, managed service contracts, and cloud consumption models — indicates that vendors and channel partners who can thread hybrid deployment flexibility with hardened security controls will capture disproportionate upside.

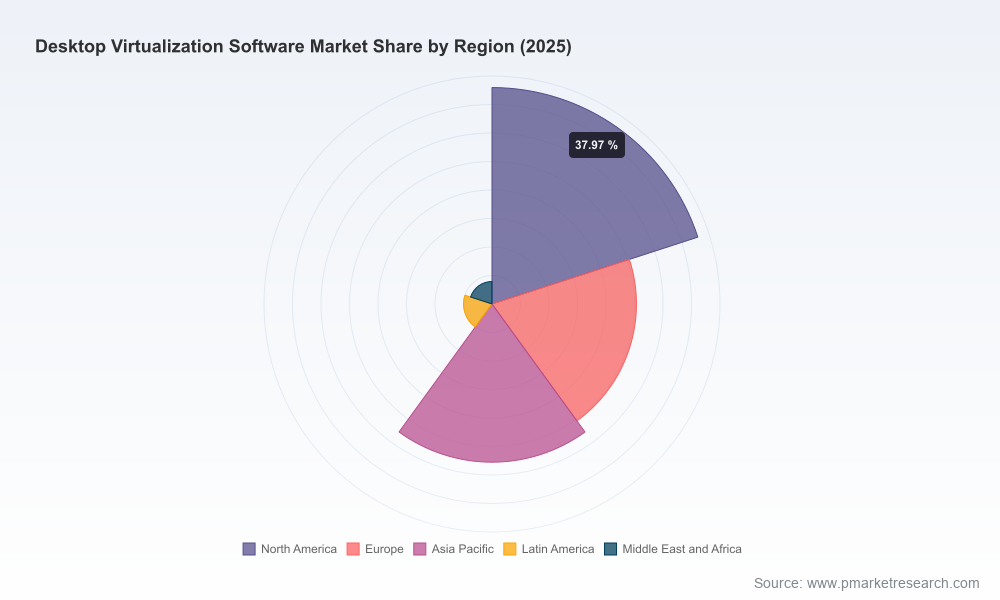

Rather than presenting granular geographic or application-level breakdowns here, we emphasize that the aggregate scale and the double-digit CAGR provide the strategic context necessary for enterprise planners: this is not a niche or transit discipline — desktop virtualization is maturing into foundational infrastructure for distributed workforces and regulated workloads alike.

The competitive map combines hyperscalers, legacy virtualization specialists, and focused innovators. Each class brings distinct levers:

Hyperscalers — with integrated cloud stacks and native identity/playbook services — are moving aggressively to embed virtual desktop capabilities into broader enterprise cloud consumption. Their propositions are attractive for organizations already consolidating other workloads to a single cloud provider.

Traditional VDI specialists — firms with longstanding protocol and endpoint optimization expertise — continue to sell differentiated performance, endpoint features, and hybrid on-prem compatibility to customers with complex latency, GPU, or data residency needs.

New entrants and niche vendors — including cost-optimized Linux-based offerings and SMB-targeted platforms — are expanding choice, particularly for price-sensitive or specialized-edge deployments.

Key vendors profiled in our report include market leaders that represent the strategic trade-offs facing buyers:

Microsoft Corporation — strong integration within Microsoft 365 and hybrid session models; continued enhancements extend enterprise lifecycle management and app-attach capabilities.

Amazon Web Services (AWS) — managed cloud desktop services with flexible pricing and expanded OS support; recent regional expansions and support for modern server images improve global availability and security posture.

Citrix Systems, Inc. — focused on secure remote access and high-fidelity user experience via its HDX protocol; notable policy shifts toward cloud-based licensing require planned migration handling.

Omnissa (formerly VMware) — enterprise VDI with strong hybrid and on-prem integration; continues to be selected where endpoint control and private-cloud consistency are critical.

Nutanix, Inc. — hybrid cloud play with unique hypervisor integration and channel-friendly consumption models; recent partnerships extend hybrid Azure Virtual Desktop scenarios on native hypervisor platforms.

Parallels, Inuvika, Oracle — represent SMB, open-source/Linux, and integrated cloud-database plays respectively; each targets differentiated buyer segments that prioritize cost, simplicity, or platform integration.

Notable recent developments we analyze in depth include:

AWS expanding regional availability and adding modern server image support with enhanced platform security.

Microsoft extending app-attach compatibility to newer server releases, simplifying application lifecycle and image sprawl for large estates.

Nutanix moving to enable hybrid AVD scenarios in public preview, signaling stronger vendor cooperation models between hypervisor providers and hyperscaler desktops.

Citrix’s policy-driven migration to cloud-based license activation — a posture that creates short-term migration cost and risk considerations for legacy customers.

Compliance and data sovereignty: The interplay of national data residency rules and extraterritorial reach of certain law regimes (e.g., cross-border access frameworks) makes provider selection a legal as well as technical decision for regulated industries.

Security posture and Zero Trust: Implementing Zero Trust, device compliance, and advanced monitoring within VDI introduces meaningful operational costs and often requires advanced licensing tiers or third-party tooling.

People and skills: In-house competencies for image management, SRE for virtual desktops, and hybrid networking are less common than for traditional on-prem servers; labor cost and vendor-managed service trade-offs should be modelled explicitly.

The report is purpose-built to support immediate 2026 decision cycles. Key practical deliverables include:

Executive decision frameworks that map business priorities (cost, security, UX, compliance) to platform archetypes and sensible vendor shortlists.

Scenario-driven TCO models in USD (Million unit basis), configurable for consumption vs. ownership options, licensing permutations, and staff-cost sensitivity.

Deployment playbooks and migration blueprints — from pilot sizing to enterprise rollout — including RFP templates and SLA negotiation checklists.

Vendor scorecards and interoperability matrices that evaluate performance, security controls, compliance readiness, and ecosystem lock-in risk.

Risk and compliance mapping for regulated industries, including a decision checklist for data residency and cloud-provider legal exposure.

Channel and partner engagement playbooks for systems integrators and MSPs seeking to monetize migration services and managed VDI offerings.

Case studies and implementation snapshots showcasing common pitfalls, performance tuning practices, and measurable business outcomes (user productivity, helpdesk deflection, lifecycle cost).

Adopt a modular, exit-aware architecture: prioritize solutions that allow hybrid deployment, clear data egress controls, and portable management layers to avoid deep lock-in.

Build a transparent TCO and security ledger: model licensing, operational staff, endpoint security, and compliance remediation as discrete line items to enable apples-to-apples vendor comparisons.

Plan for phased migration with clear guardrails: mandate pilot success criteria, user experience SLAs, and rollback paths. Where vendors change licensing posture (e.g., cloud-based LAS), include cost and timeline buffers.

Align procurement with legal and privacy teams early: data sovereignty constraints and the changing regulatory landscape must inform region and vendor eligibility before procurement.

Leverage ecosystem partnerships: select vendors with proven channel enablement and third-party integrations (SASE, identity fabrics, device posture) to reduce integration risk and accelerate time-to-value.

Our market sizing combines historical revenue reporting (2020–2025), vendor public disclosures, contract-level intelligence, and an ensemble forecasting approach for 2026–2032 that blends demand-side adoption curves with supply-side capacity and pricing scenarios. The reported CAGR and aggregate market trajectory reflect our high-confidence central forecast; scenario variants and sensitivity analyses are included in the full deliverable for risk-aware planning.

For CIOs and infrastructure leaders: this research translates macro momentum into practical procurement and deployment actions that reduce migration risk and optimize recurring cost.

For vendors and partners: the report clarifies where feature investments and partner motions will unlock the largest addressable opportunities over the next three years.

For investors and strategic planners: concentration metrics and vendor trajectory analysis illuminate consolidation opportunities and competitive threats within a market that is growing at a double-digit pace.

PW Consulting’s full Desktop Virtualization Software Market report contains the granular models, vendor scorecards, scenario TCOs, and region/application maps necessary to operationalize these insights. To preserve strategic exclusivity of core segmentation and pricing intelligence — and to ensure you receive the most current vendor and regulatory updates — the full datasets and playbooks are available via our official report page. Engaging with that material will allow your team to run customized scenarios and extract the specific, actionable numbers needed for procurement and technology roadmaps in 2026.

Contact PW Consulting to arrange a tailored briefing or to license the data and implementation playbooks that will underpin your desktop virtualization strategy this year.

For detailed analysis of this topic, please visit the official page:Desktop Virtualization Software Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com