Fully Rugged Tablets Market: Strategic Imperatives for 2026

Executive snapshot

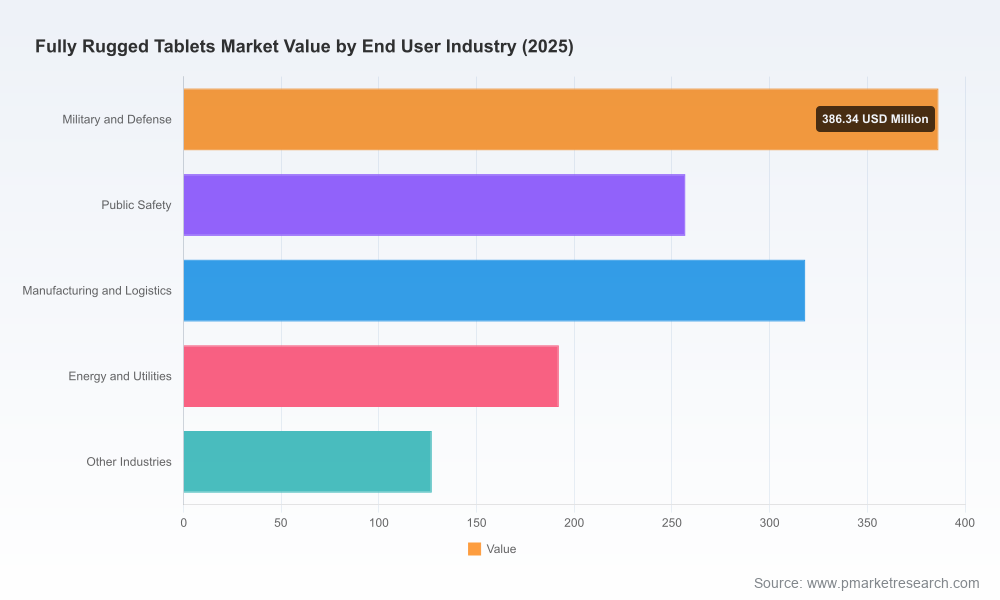

As field operations, defense programs, and asset-intensive industries accelerate digital transformation, the fully rugged tablet market has matured into a distinct strategic arena. PW Consulting’s latest market study shows the sector reached approximately USD 1,280.5 Million in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 7.35% through the 2026–2032 forecast window—driving the market well past the USD 2 billion mark by the end of the period. For executives planning 2026 product roadmaps, procurement cycles, or M&A activity, this report provides the decision-grade intelligence necessary to convert market momentum into sustainable advantage.

Fully Rugged Tablets Market

Why the report matters for 2026 decisions

- Timing procurement and product launches: The reported growth trajectory implies accelerating replacement and fleet expansion cycles across utilities, logistics, public safety, and defense. Buyers and OEMs must align sourcing, certification and production milestones to capture the next wave of tenders.

- Risk-calibrated supply strategies: Prolonged lead times and material cost pressures mean that a ‘just-in-time’ approach without strategic buffers will increase project risk and total cost of ownership (TCO).

- Regulatory and security positioning: With standards and export rules evolving rapidly, the right compliance and security posture will be a competitive differentiator in government and critical infrastructure procurements.

Market dynamics shaping 2026 strategies

- Component supply pressure. Demand for high-performance x86 processors in rugged designs has extended lead times. Our synthesis of industry signals indicates processor lead times stretching to 20–24 weeks in early 2025, creating a material sequencing and inventory planning challenge for OEMs and system integrators.

- Standards evolution. The MIL‑STD‑810H refresh in 2024 tightened thermal and vibration test protocols for fully rugged devices. Organizations bidding for defense and certain government contracts must ensure device portfolios meet both the letter and the interpretive expectations of updated test regimes.

- Geopolitical constraints. Export control adjustments on advanced semiconductors impose practical limitations on supplier choice and market access for vendors serving markets under restricted trade conditions. This requires contingency sourcing and, in some cases, architectural redesigns that can affect time-to-market and bill-of-materials (BOM) cost.

- Input-cost inflation. Specialized materials—most notably chemically strengthened aluminosilicate glass used in hardened displays—saw double-digit price moves in recent quarters. Screen-cost inflation ripples through aftermarket pricing, warranty economics, and replacement policy design for fleet customers.

- Consolidation and concentration. The market is meaningfully concentrated at the top, with leading vendors controlling a majority of commercial supply. That concentration creates both stability and competitive pressure: small-to-midsize players must find defensible niches or partner pathways to scale.

What the PW Consulting report delivers (practical, non-academic outputs)

This study was structured as an applied intelligence product for commercial leaders, procurement heads, product managers and investors. Key deliverables include:

Fully Rugged Tablets Market

- Tactical buyer playbooks — procurement calendars aligned to component lead-time scenarios, negotiation checklists for extended warranties and service-level agreements (SLAs), and a supplier risk scoring matrix that translates supply-chain indicators into procurement triggers.

- Product and engineering guidance — design tradeoff frameworks (durability vs. weight vs. thermal dissipation), BOM sensitivity analyses, and a decision tree for choosing between x86 and ARM platforms in ruggedized deployments.

- Regulatory & certification roadmap — a step-by-step checklist for MIL‑STD and other certifications, plus an impact assessment of security certifications such as FIPS on procurement eligibility in public-sector tenders.

- Commercial and GTM playbook — prioritization matrices to match go-to-market strategies with vertical demand profiles, partner play suggestions (channel OEM, systems integrator, and value-added reseller strategies), and pricing levers to protect margin under raw-material inflation.

- Investor diligence toolkit — a sector scorecard, scenario-based valuation sensitivity to supply shocks, and M&A heat maps that highlight asset classes likely to generate scale or technological leapfrogging.

Competitive landscape — what firms are doing and why it matters

The competitive field is anchored by vendors with established rugged portfolios and certification expertise. Our qualitative benchmarking of leading suppliers reveals three persistent strategic archetypes:

Fully Rugged Tablets Market

- Platform leaders optimizing scale and certification. Vendors with deep heritage in rugged computing continue to invest in platform robustness, multi-generation certification, and services that reduce procurement friction for large institutional buyers.

- Feature-focused innovators targeting specialized workflows. Several firms concentrate on verticalized capabilities—barcode subsystems, hot-swappable batteries, or extreme-display technologies—to win in logistics, first responder, and energy markets where workflow fit outweighs unit economics.

- Cost-competitive challengers adopting modularization. Newer entrants and select OEMs are pursuing modular designs and outsource-heavy supply chains to reduce time-to-market and undercut incumbents on standardized, high-volume deployments.

Representative vendor notes (operational highlights, not market share assertions):

- Getac continues to iterate on high-performance, defense-grade platforms and recently launched a large-screen model with next-gen Intel processors and enhanced ingress protection—an example of premium-spec expansion targeted at defense and heavy field-service use cases.

- Panasonic’s Toughbook family remains a benchmark in public-safety and mission-critical deployments, and recent updates emphasize sustained connectivity (e.g., 5G), extended battery life and Windows-based application compatibility important to large enterprise IT stacks.

- Dell’s rugged portfolio blends desktop-class manageability with ruggedized mechanicals; recent certification milestones underscore positioning for secure government procurement channels.

- HP, Zebra (Xplore), DT Research and MobileDemand demonstrate differentiated tactics—ranging from enterprise service integration and utilities-focused feature sets to logistics-optimized scanning and battery-swappability—that create defensible vertical positions.

Strategic implications by stakeholder

- For enterprise buyers — Build a procurement timeline that pre-qualifies devices for updated certification windows and incorporates multi-supplier strategies to mitigate lead-time exposure. Prioritize total cost over unit price when fleet uptime is revenue-critical.

- For OEMs and component suppliers — Invest now in certification capabilities, modular product architectures that reduce lead-time dependency on specific components, and alternative sourcing for high-risk inputs (e.g., display glass and specialty connectors).

- For investors and PE sponsors — Focus on assets that provide vertical integration into services (field maintenance, logistics support) or proprietary certification know-how. Valuation should factor in near-term supply risk scenarios and the time required to funnel products through stricter certification protocols.

- For public-sector purchasers — Insist on supply-chain transparency clauses and certification traceability. Consider longer-term service contracts to smooth vendor investment in certification and resilience.

How to use this report to shape a 90-day action plan for 2026

- Week 1–2: Align internal stakeholders on priority verticals and deploy the report’s procurement playbook to establish target delivery windows and contingency inventory levels.

- Week 3–6: Execute supplier due diligence using the risk-scoring templates; begin negotiation of staggered deliveries and price-escalation clauses tied to quantifiable material indices.

- Week 7–10: Validate product designs and certification timelines; commence pre-certification trials where feasible to de-risk proposal timelines for tenders expected in late 2026.

- Week 11–12: Finalize go-to-market partnerships, lock in initial production slots, and brief investor or board constituencies with scenario-based financials from the report’s modeling suite.

What we’re intentionally holding back (and why you should read the full report)

In line with our “trailer” approach, this press summary presents the strategic takeaways and high-impact implications without the granular segmentation tables, vendor share matrices and downloadable financial models that are central to transaction and procurement-level decision-making. The full report contains the proprietary segmentation, region- and vertical-level adoption curves, supplier scorecards, and build-your-own-scenario Excel models that practitioners use to convert strategy into executable plans. These datasets are essential for granular bid pricing, localized sourcing decisions, and M&A screeners—areas where small differences in assumptions materially change outcomes.

Closing recommendation

2026 will be a turning point: organizations that proactively align procurement cadence, certification readiness, and component sourcing will convert a growing market into durable advantage. The market’s steady mid-single-digit CAGR masks significant strategic inflection—those who treat rugged computing as a systems problem (technology + supply + certification + service) rather than a unit-sale exercise will capture outsized value. PW Consulting’s full market dataset and practical toolkits are designed to shorten the time from insight to impact for leaders operating in this space.

To access the full report, models and supplier scorecards, visit the PW Consulting research portal and request the Fully Rugged Tablets Market study. The complete package provides the closed-loop intelligence required for high-stakes 2026 decisions.

For detailed analysis of this topic, please visit the official page:Fully Rugged Tablets Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com