Exploration and Production (E&P) Software Market to Reach USD 43.14 Billion by 2036, Driven by AI-Powered Reservoir Modeling, Cloud-Based Platforms

Networking |

2026-07-01 11:52:07

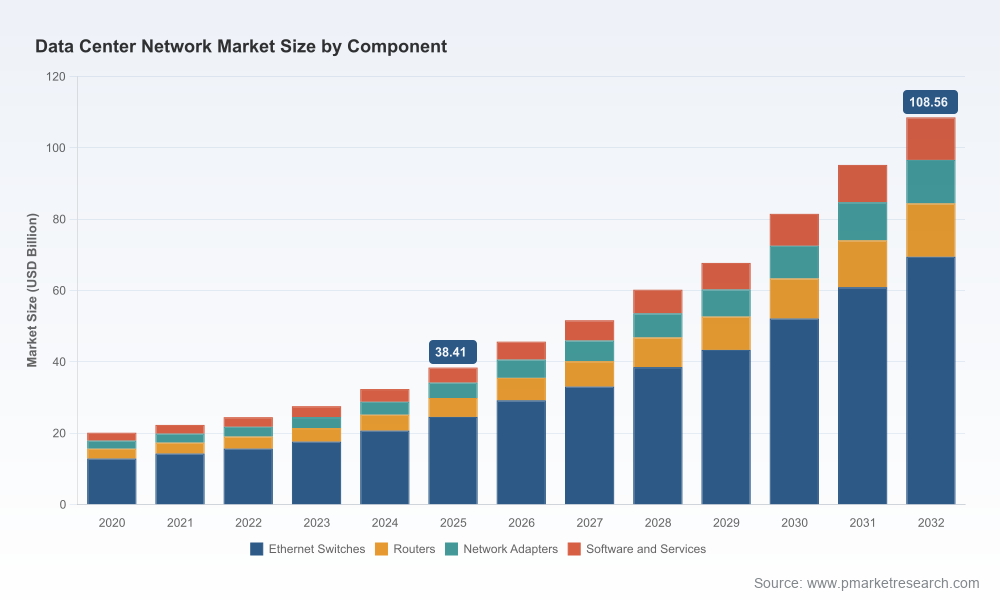

PW Consulting’s latest Data Center Network Market report synthesizes the tactical and strategic shifts that will define networking decisions through 2026 and beyond. Built from a rigorous historical series (2020–2025) and forward-looking scenario modeling across 2026–2032, the study quantifies a market accelerating under the combined forces of generative AI, hyperscale expansion, and grid/infrastructure constraints. Our headline macro: the global data center networking market expands from an estimated USD 38.41 Billion in 2025 to an anticipated USD 45.68 Billion in 2026, continuing at a compound annual growth rate (CAGR) of 15.9% over the forecast horizon. This growth underwrites major capex reallocation and supplier choices that procurement, cloud architects, and CIOs must confront in 2026.

Data Center Network Market

Demand shock from AI. The rapid deployment of large-scale AI training and inference clusters has changed the performance and topology requirements for data center networks. Bandwidth density, low-latency fabrics, and deterministic telemetry are now primary procurement criteria rather than optional performance differentials.

Data Center Network Market

Infrastructure cost externalization. New policies and industry commitments—most notably the Ratepayer Protection Pledge adopted by major cloud and AI providers—are re-shaping how grid and interconnection costs are allocated. Simultaneously, prolonged grid connection lead times in primary markets are driving operators toward behind-the-meter generation and battery co-location strategies.

Data Center Network Market

Supplier consolidation and platform convergence. The market is concentrated among a small set of technology leaders. Consolidation and strategic acquisitions are reshaping product roadmaps and integrated stacks, which affects vendor selection, interoperability risk, and long-term TCO.

Validated market sizing and growth scenarios: a transparent methodology that reconciles historical shipments, public vendor disclosures, and buy-side CapEx signals to produce base, upside, and downside forecasts for 2026–2032.

Technology maturity maps: lane-by-lane assessment of switch silicon, DPUs, Ethernet vs. InfiniBand fabrics, and optical interconnects—highlighting readiness, migration risk, and integration complexity for AI and hybrid-cloud deployments.

Vendor evaluation matrices: pragmatic criteria—performance, power-per-bit, telemetry, software ecosystem, roadmap transparency, and commercial terms—scored to aid shortlisting for RFPs and PoCs.

CapEx/Opex modeling templates and sensitivity analyses: downloadable models to stress-test vendor proposals against power, space, and interconnect timelines under multiple grid-cost allocation regimes.

Supply-chain and risk heatmaps: identification of critical component exposure (silicon families, optics suppliers, and DPU roadmaps), plus contingency playbooks for procurement teams.

M&A and partnership playbook: actionable criteria for strategic acquisitions, divestitures, and alliances to shore up fabric capabilities or accelerate time-to-market for AI-centric architectures.

The competitive topology is shaped by vendors that combine silicon, systems, and software ecosystems to serve hyperscale, colocation, and enterprise clouds. While the field includes many capable suppliers, a handful of firms dominate product roadmap influence and open-architecture adoption.

Cisco Systems — With ongoing silicon and system investments, Cisco continues to position itself as a provider of end-to-end AI-optimized fabrics for both hyperscale and enterprise data centers. Recent announcements around next-generation ASICs demonstrate its emphasis on scalability and high-link-count fabrics suitable for AI workloads.

Arista Networks — Arista’s focus on high-throughput Ethernet platforms and data center fabrics targets cloud and AI clusters where throughput-per-watt and operational automation are decisive. Product refreshes aligned to new Broadcom silicon generations aim to lower TCO while preserving feature parity for cloud-native operations.

Juniper Networks (now integrated with HPE) — Following acquisition activity, Juniper’s portfolio—combined with an enterprise and edge systems provider—creates an integrated path for customers seeking a unified stack from edge to core with strong routing and AI-native switch functionality.

NVIDIA — Beyond GPUs, NVIDIA’s expansion into Spectrum and InfiniBand switching and DPU-enabled architectures is reshaping how AI clusters are interconnected. Its strategy emphasizes accelerated networking, adaptive routing, and offload capabilities for AI data paths.

Broadcom — As a foundational silicon supplier, Broadcom’s high-capacity ASIC families continue to dictate performance baselines across multi-vendor switch platforms, influencing both vendor differentiation and upgrade cycles.

HPE, Dell, Huawei, Extreme Networks, Nokia — These vendors complement the ecosystem with integrated systems, optical interconnects, and regionally differentiated go-to-market approaches. Choice among them now hinges on integration depth, lifecycle support, and regional compliance considerations.

Recent strategic moves underline the competitive dynamics: major product launches from Cisco and Arista underscore the race for AI-optimized silicon and fabrics; and large-scale M&A activity—exemplified by HPE’s integration of Juniper—accelerates portfolio consolidation. These shifts require procurement teams to re-evaluate interoperability, lock-in exposure, and migration pathways in 2026.

Grid policy is now an active procurement consideration. Corporate pledges and state-level regulations are shifting interconnection and grid-upgrade costs onto large load customers in some jurisdictions. The practical effect: data center operators are modeling behind-the-meter generation and storage as part of network TCO and site selection.

Connection lead times are not theoretical—it is common for primary markets to experience grid interconnection waits measured in years. This delays deployment and raises the business value of architectures that can be staged or scaled non-linearly.

Industry standards bodies and benchmarking frameworks (e.g., Uptime Institute Tiers) remain decisive in RFP language and SLA validation. Network designs that support Tier III/IV expectations around concurrent maintainability and redundancy command premium pricing and stricter qualification gates.

Silicon and DPU roadmaps matter. The choice between ASIC families and DPU-enabled platforms alters software architecture, telemetry, and security postures. Procurement must align with long-term software ecosystems, not just box-level performance.

Optical and interconnect sourcing is a gating factor for scale-out AI clusters. Optical vendor strategies and inventory constraints can create multi-quarter delays—early engagement and longer lead-time contracts are essential risk mitigators.

Power and cooling constraints now drive network topology. Higher port speeds and denser switch fabrics increase rack-level power density, requiring integrated planning across networking, compute, and facilities teams.

Prioritize architecture-first RFPs. Frame RFPs in terms of fabric-level requirements (throughput, telemetry, deterministic latency) and lifecycle costs rather than individual device specs.

Stress-test vendor bids against grid-cost scenarios and behind-the-meter solutions. Use CapEx/Opex models to examine outcomes under different interconnection cost allocations and battery-integration options.

Negotiate for software portability and telemetry openness. Ensure telemetry standards and APIs are contractually defined to avoid future lock-in and to enable third-party observability overlays.

Build supply-chain resilience into procurement timelines. Include multi-source clauses for optics and critical silicon, and prioritize vendors with transparent lead-time commitments.

Consider blended vendor strategies. For many organizations, the optimal path blends hyperscaler-grade fabrics for AI clusters with more standardized enterprise solutions for business-critical workloads—governed by a unified management plane.

PW Consulting’s Data Center Network Market report is designed as an operational playbook for executives and procurement teams. The full report contains granular subsegment forecasts, regional build-out scenarios, vendor scorecards, downloadable financial models, and RFP language templates—all calibrated to help you make defensible networking investments in 2026.

In this briefing we intentionally present high-level strategic findings and the macro market trajectory—our “trailer”—to inform initial planning. For detailed line-item forecasts, component-level sizing, and vendor-specific migration pathways (the datasets that agencies and vendors will use to shape negotiations), access the full report and accompanying toolkits on PW Consulting’s portal.

PW Consulting remains available for tailored briefings, vendor-selection workshops, and bespoke TCO modeling to support 2026 procurement cycles. In a year where network architecture choices will materially affect AI performance, operational resilience, and long-term cost, informed, scenario-driven decisions will determine winners and laggards.

For detailed analysis of this topic, please visit the official page:Data Center Network Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com