Rack and Pinion Construction Elevator Market — Strategic Outlook for 2026: PW Consulting Report Preview

Executive teaser

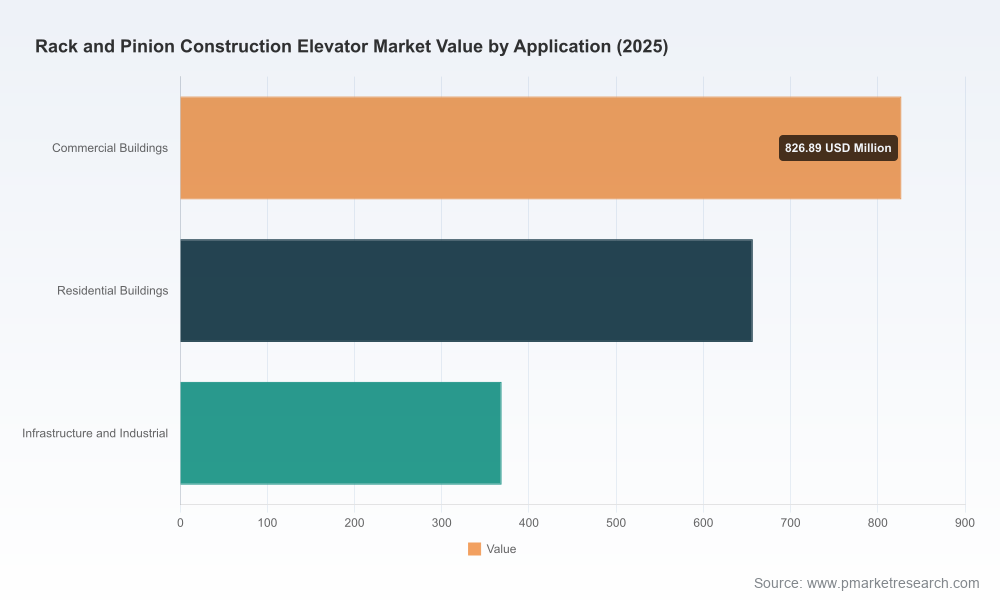

The global rack and pinion construction elevator market is at an inflection point. Our proprietary sizing places the market at USD 1,852.08 Million in the 2025 base year and projects a rise to USD 2,085.39 Million in 2026, advancing at a 7.0% CAGR through the 2026–2032 forecast window to reach approximately USD 2,974.03 Million by 2032. These headline figures reflect a convergence of construction activity in dense urban markets, renewed industrial maintenance cycles, and an increase in safety and compliance-driven replacement spend.

Rack And Pinion Construction Elevator Market

Why the 2026 planning cycle should treat this report as mission-critical

- Budget calibration: The report translates market growth assumptions into practical capital and operating budget scenarios for 2026 procurement cycles, enabling firms to time purchases, rentals and spare-part hedges against price swings.

- Supplier strategy: It maps vendor capabilities against operational requirements (capacity, speed, certification, service footprint), turning competing product claims into comparable procurement scorecards.

- Regulatory readiness: With proposed updates to ASME A17.1 and persistent OSHA requirements for construction hoists, the report delivers a compliance playbook that informs both equipment spec and maintenance cadence.

- M&A and partnership screening: The analysis identifies logic-driven targets and partnership archetypes for fleet expansion, rental consolidation, and local manufacturing partnerships—critical for players seeking scale in 2026.

- Risk-adjusted sourcing: We model raw material exposure—particularly steel price volatility—and outline mitigation strategies for 12–48 month procurement horizons.

What’s inside (practical, actionable deliverables)

This is not a high-level slide deck. The full report is a toolkit designed to be operationalized during 2026 decision cycles. Key components include:

Rack And Pinion Construction Elevator Market

- Methodology and reproducible market model — transparent assumptions, demand drivers, and scenario variants for conservative, base, and accelerated growth paths.

- Total market size and near-term forecasts (2026–2032) with sensitivity testing for commodity-driven cost shocks and construction activity shifts.

- Procurement playbooks — request-for-proposal templates, scorecards for OEM and rental suppliers, and negotiation levers tailored to one-off purchase, fleet refresh, and long-term rental contracts.

- Vendor benchmarking — capability matrices that evaluate product families on certification, load profiles, speed, maintenance requirements, spare-parts lead times, and aftermarket service networks.

- Regulatory and safety roadmap — actionable checklists to align equipment selection and on-site processes with OSHA 1926.552, and guidance on the anticipated ASME A17.1 revisions (definitions, equipment siting, periodic testing requirements).

- Raw-material and cost-pass-through modelling — forward curves and stress tests informed by recent steel market moves to quantify the impact on procurement, pricing and gross margins.

- Lifecycle cost calculators for buy/rent/refurbish decisions, including recommended replacement intervals for safety components and testing cadences.

- Scenario-driven go-to-market playbooks for OEMs, rental operators, and contractors — from local service footprint strategies to digital telematics adoption for predictive maintenance.

Competitive landscape — who matters and why

The market shows a moderate concentration: the top three manufacturers collectively account for roughly 31% of reported industry volume, while the top five approach half the market. For decision-makers, this concentration level translates into meaningful, but not monopolistic, supplier leverage: there is choice — and those choices matter for service, certification and long-term uptime.

Rack And Pinion Construction Elevator Market

- Alimak Group AB (Stockholm, Sweden) — Positioned as the global reference in temporary and permanent rack-and-pinion systems, Alimak’s breadth of certified solutions and global service footprint make it a primary partner for multinational contractors. Strategic implication: prioritize Alimak for large-scale projects where global warranty and synchronized spare-part logistics matter.

- GEDA GmbH (Germany) — GEDA’s in-house manufacturing and industrial project track record make it a go-to for engineered solutions in power, petrochemical and high-rise construction. Strategic implication: evaluate GEDA for technically demanding retrofit or shutdown projects where bespoke structural components are required.

- STROS (Czech Republic) — As a price-competitive supplier with strong ANSI-compliant models, STROS is commonly present in US fleets via partners. Strategic implication: target STROS for cost-sensitive, high-volume rental programs, while validating local service coverage.

- USA Hoist / Mid-American Elevator Company (Crest Hill, IL, USA) — Known for heavy-duty, high-capacity series, they are a strategic choice for projects demanding speed, capacity and domestic manufacturing. Strategic implication: domestic contractors should weigh USA Hoist where lead time and local support minimize operational downtime.

- Century Elevators (Alimak Group) — Specialist in permanent rack-and-pinion installations; recommended for industrial facilities and permanent vertical transport programs where lifecycle planning and integration with plant systems are priority.

- McDonough Elevators (USA) — A major fleet operator and service provider: offers sales, rental, refurbishment and maintenance. Strategic implication: commercial contractors can accelerate project mobilization using McDonough’s rental and refurbishment options to avoid capex and shorten lead times.

- UCEL Inc. (Canada) — Strong at North American installations and industrial maintenance lifts; recent thought leadership highlights scalable lifts for shutdowns and maintenance. Strategic implication: consider UCEL for cross-border projects requiring CSA and ANSI compliance with Canadian logistics know-how.

- BrandSafway (USA) — Turnkey provider with engineering and nationwide service capability: attractive to general contractors seeking single-vendor responsibility for installation and maintenance.

- Maspero Elevatori (Italy) — Longstanding European specialist; recommended where custom engineering and legacy compatibility matter.

- Ficont Industry / 3S Lift (China) — CE-certified suppliers attractive on cost and for regional markets; assess carefully on spare parts availability and long-term warranties.

Industry dynamics and near-term risks

- Raw materials: Steel price dynamics are a leading short-term profit risk. Market indicators show a material step-up in hot rolled coil pricing into early 2026 — a variable that materially impacts OEM cost bases and aftermarket spare-part economics. The report quantifies the pass-through scenarios and recommended contracting approaches.

- Regulation & safety: OSHA 1926.552 remains the operational baseline for US construction hoists; anticipated revisions to ASME A17.1 will require firms to revisit equipment definitions, siting practices and periodic testing regimes — all of which have CAPEX and OPEX implications that we model in the report.

- Maintenance cadence and lifecycle costs: Industry practice requires twice-yearly testing of critical hoist safety devices with component replacement typically every three to four years. For fleet operators, these cycles should be budgeted into 2026 service agreements and CAPEX plans.

- Fleet strategies: Rental versus ownership decisions are being re-evaluated as lead times lengthen, commodity volatility increases and contractors manage project cashflow. We provide decision trees and breakeven horizons that help determine when to rent, buy new, or refurbish.

- Product development: New model introductions are accelerating (for example, recent 2026 model announcements by regional manufacturers). These introduce both upgrade opportunities and compatibility concerns for fleets — another reason to prefer modular, serviceable platforms.

A 2026 tactical playbook — nine immediate moves for executives

- Stress-test 2026 procurement plans against a 20–40% steel-cost shock and adopt indexed price clauses where possible.

- Pre-qualify two OEMs and two rental operators for major projects to create competition and redundancy in delivery timelines.

- Lock a three-year spare parts and critical component program with guaranteed lead-times and service SLAs.

- Embed regulatory-change clauses in supplier agreements to allocate costs should ASME revisions impose new testing or equipment upgrades.

- Run a pilot telematics program on 5–10% of fleet to validate predictive maintenance ROI and reduce unexpected downtime.

- Evaluate refurbishment over replacement for mid-life units to conserve capex and accelerate deployment.

- Identify one strategic M&A or partnership target in 2026 that improves regional service density or fills a technology gap.

- Establish a cross-functional procurement–operations–safety steering committee to reduce specification gaps and accelerate deployment.

- Prioritize staff training for on-site safety device testing and document adherence to the twice-yearly testing cadence.

Recent signals market participants should not ignore

- Supplier thought leadership and case studies highlight the increasing use of scalable rack-and-pinion lifts for industrial shutdowns to reduce downtime — a proposition supported by multiple North American service providers.

- New model launches in early 2026 promise improved payload-to-footprint ratios; buyers must weigh improved performance against spare-parts commonality and certification timelines.

Final note — the “trailer” to the full intelligence

This preview demonstrates the analytical depth and operational focus of the PW Consulting Rack And Pinion Construction Elevator market study but intentionally omits the granular regional, type and application split tables that clients use to build procurement-level budgets and deployment plans. If you are preparing 2026 capital allocations, vendor negotiations, or M&A scoping, the full report includes the critical microdata (regional and application allocations, supplier share tables, and downloadable model files) and step-by-step playbooks you will need to execute.

Contact PW Consulting to access the complete report and supporting datasets — and to schedule a bespoke briefing that translates these market insights into an executable 90-day plan for your organization.

For detailed analysis of this topic, please visit the official page:Rack And Pinion Construction Elevator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com