The Falcon Is Unveiled-Residential Projects in Gurgaon

Other |

2026-07-01 11:37:50

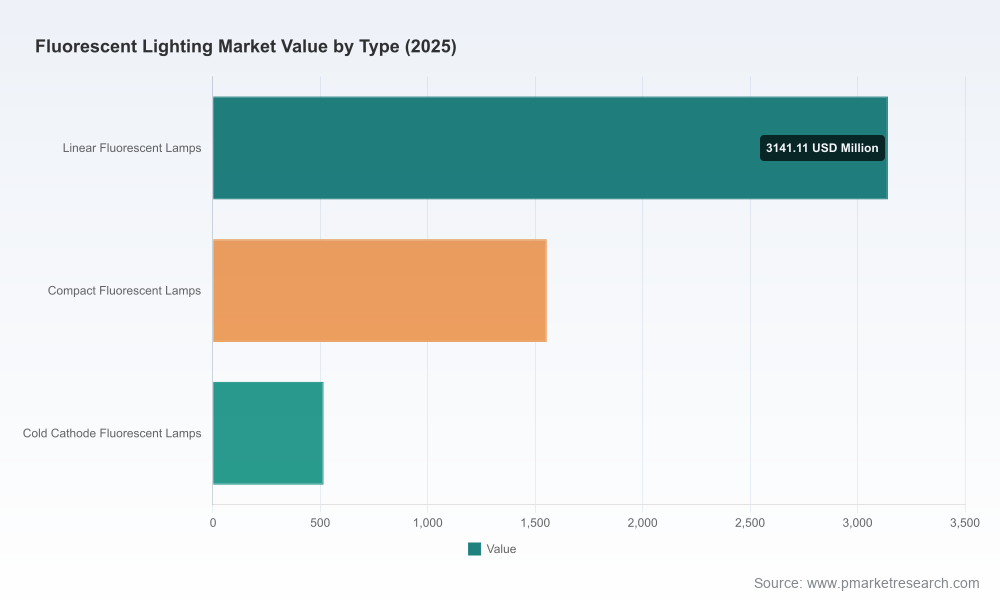

As fluorescent lighting moves from mainstream specification to niche legacy product, executives face a compressed window to optimize value, manage regulatory exposure, and rationalize portfolios. PW Consulting’s latest Fluorescent Lighting Market report — anchored on a 2025 base year and a detailed forecast through 2032 — quantifies this transition: the global market contracted from roughly 7.85 billion USD in 2020 to about 5.21 billion USD in 2025 and is forecast to continue declining (2026 projection: ~4.88 billion USD), with a negative compound annual growth rate of -11.5% across the 2026–2032 outlook. For companies that must decide capital allocation, go-to-market positioning, or M&A targets in 2026, these are not academic numbers — they are a directional imperative.

Fluorescent Lighting Market

Portfolio prioritization: A sharply contracting market compels manufacturers to decide which product lines to sustain, retrofit, or sunset. The difference between a disciplined exit and a reactive scramble will determine margin preservation in 2026 and beyond.

Fluorescent Lighting Market

Regulatory timing: Emerging and enforced regulations change the viable product set and create both compliance costs and strategic opportunities (e.g., retrofits, disposal services, and low-mercury innovations). Companies that move preemptively gain procurement leverage and customer retention advantages.

Fluorescent Lighting Market

Channel and service transformation: With replacement demand slowing, growth shifts toward specialized retrofit services, circular-economy solutions (take-back and recycling) and hybrid products. Distributors and brand owners must re-engineer commercial models to monetize services and total cost of ownership rather than only units sold.

M&A and consolidation vectors: Market contraction increases the value of scale in logistics, recycling, and retrofit capabilities. The report identifies logical bolt-on targets and valuation frameworks tailored to the current decline trajectory and regulatory environment.

Robust market sizing and scenario-based forecasts: We provide audited topline historicals and three forward-looking scenarios (base, downside, and accelerated transition) that stress-test demand under different regulatory and substitution adoption curves.

Regulatory impact maps and transition timetables: Detailed assessments of policy levers — including the EU bans and global mercury limits — and their phased operational impacts by product family and compliance cost buckets.

Supply-chain and input-cost analytics: End-to-end mapping of phosphors, rare-earth dependencies, manufacturing nodes, and tariff exposure, coupled with mitigation playbooks for sourcing and vertical integration.

Competitor benchmarking and concentration metrics: A strategic scorecard that combines product mix, channel reach, service capabilities, and financial leverage. The market’s top-tier concentration (CR3 ~38.5% and CR5 ~52.2%) is analyzed to reveal pockets of competitive advantage and takeover potential.

Commercial playbooks and pricing frameworks: Tactics for distributors, OEMs, and retrofit specialists to defend margin via value-added services, dynamic pricing, and demand-shaping contracts.

M&A screening toolkit and integration checklists: Deal screening criteria, synergies quantification, and 100-day integration priorities tailored to acquisition targets in logistics, aftermarket services, and niche low-mercury manufacturing.

Operational readiness and compliance checklists: Practical steps to meet imminent regulatory thresholds — from labelling and certification to mercury-content documentation and end-of-life handling.

Interactive Excel models and dashboards: Fully unlocked models for sensitivity analysis, scenario toggles, and custom regional or product focus (note: detailed sub-segment datasets and proprietary tables are available in the report package and online portal).

The report contains a close-read of incumbent and challenger strategies. Leading legacy manufacturers and lighting specialists remain influential but face different strategic imperatives:

Signify Holding (Eindhoven, Netherlands; https://www.signify.com/global) — A global leader in linear fluorescent and CFL technologies, strategically positioned to manage transition through retrofit solutions and channel relationships. Their global scale and R&D provide resilience, but they must accelerate migration to non-mercury alternatives and services monetization.

LEDVANCE GmbH (Munich, Germany; https://www.ledvance.com) — Strong in professional channels with a broad fluorescent portfolio. Success depends on converting existing buyers to hybrid and LED retrofit lines while optimizing inventory of now-prohibited legacy SKUs in regulated markets.

Panasonic Corporation (Osaka, Japan; https://industrial.panasonic.com/ww/products/pt/lighting) — Focused, regionally selective product presence and industrial relationships. Their strategic options include targeted withdrawal from declining segments and redeploying manufacturing footprint into value-added projects.

Havells India, Crompton Greaves, Opple, NVC (Asia-focused players) — These companies retain channel depth in emerging markets and possess cost advantages. They must weigh incremental margins from commoditized sales against higher-margin service offerings and compliance costs as global standards tighten.

Satco, Westinghouse, MaxLite (North American players) — Distribution and retrofit expertise are core strengths. Those with hybrid product portfolios or retrofit-service capabilities will capture the last profitable waves of replacement demand, especially where tariffs alter import economics.

Collectively, the top-three and top-five firms account for meaningful share of the market (CR3 ~38.5%; CR5 ~52.2%), but the landscape still permits regional and service-focused entrants to carve defensible niches — particularly in aftermarket services, recycling, and conversion offerings.

EU policy shifts: Recent EU-level decisions effectively remove a set of conventional fluorescent lamps from the EU market, accelerating substitution in commercial and institutional segments. Firms must plan inventory and product lifecycles accordingly to avoid stranded stock and customer disruption.

Global mercury limits: International agreements introduce a new compliance floor for mercury content (5 mg per lamp from 2026), driving product redesign, testing costs, and potential retooling investments — but also opening opportunities for low-mercury premium positioning and recycling revenue streams.

Raw-material concentration: Phosphor and rare-earth supply chains are concentrated, with one country supplying the majority of global capacity. This creates price and supply shocks risk and elevates the strategic value of supplier diversification, inventory hedging, and vertical partnerships.

Trade measures: Tariff regimes — including significant duties on certain imports — materially change cost structures and regional sourcing economics. Companies must recompute landed cost models and consider near-shoring or local manufacturing for critical markets.

Manufacturers: Rationalize SKUs to focus on high-margin retrofit and service-enabled products; invest in low-mercury design and certification; create a controlled product withdrawal plan where regulation forces obsolescence.

Distributors: Develop retrofit-as-a-service propositions and tie pricing to customer energy savings and compliance guarantees; retool warehousing to handle returns and recycling.

Investors and M&A teams: Target assets that provide circular-economy capabilities (collection, recycling) and retrofit-service platforms; use downside scenario valuations that reflect the -11.5% CAGR risk profile across 2026–2032.

Procurement teams of large end-users: Lock in long-lead retrofit contracts with service SLAs and end-of-life handling clauses; negotiate supplier commitments on mercury-content disclosure and recycling.

The report combines bottom-up supplier interviews, product-level testing protocols, scenario-driven demand modeling, regulatory timeline mapping, and trade-flow analytics. Deliverables include fully auditable Excel models, playbooks for product withdrawal and retrofit rollouts, and a prioritized vendor directory to accelerate sourcing decisions. Critically, while this press summary highlights strategic insights and topline numbers, granular subsegment tables, region-by-region breakouts, and application-level revenue series are intentionally reserved for the full report and online data portal — a design choice to balance immediate strategic value with the report’s role as a primary source for client engagements.

PW Consulting’s Fluorescent Lighting Market report is structured to be a working tool for leadership teams drafting 2026 budgets, capital plans, and M&A pipelines. If your organization is evaluating exit timelines, retrofit investments, compliance roadmaps, or acquisition criteria, the report provides the models, checklists, and deal-screening tools to act decisively.

For access to the full dataset, subsegment breakouts, and the interactive scenario model, visit PW Consulting’s report page and schedule a briefing with our lighting and industrials practice. In an industry defined by rapid decline and regulatory inflection, the right intelligence in 2026 will separate strategic winners from those left managing stranded assets.

For detailed analysis of this topic, please visit the official page:Fluorescent Lighting Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com