Crow`s Feet Treatment Market Insights and Growth Trends

Other |

2026-06-22 13:29:30

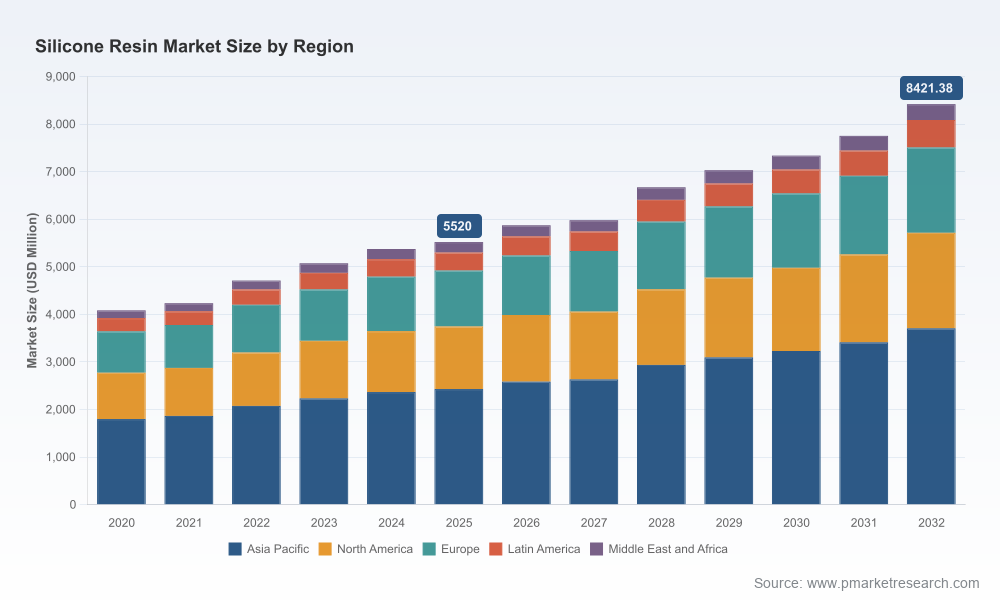

The global silicone resin market has entered a structural growth phase. After expanding from approximately USD 4,085.4 million in 2020 to USD 5,520.0 million in 2025, PW Consulting’s latest analysis projects a continued acceleration through the next planning cycle, reaching an estimated USD 8,421.4 million by 2032. Our forecast for 2026–2032 embodies a compound annual growth rate (CAGR) of 6.22%. For commercial leadership teams preparing 2026 budgets and strategy roadmaps, this report is designed to be the single most practical, decision-ready intelligence asset.

Silicone Resin Market

Demand inflection: Electrification, higher-performance coatings, and expanding use in advanced electronics are creating durable end-market pulls for specialty silicone grades. These are not short-term cyclical upticks but structural shifts that require product, channel, and capex realignment.

Silicone Resin Market

Supply-side stressors: Upstream feedstock and logistics changes are raising operating risk. Notably, metallic silicon prices moved materially higher in late 2024, driven by energy cost inflation — a factor that reverberates through resin cost bases and margin plans.

Silicone Resin Market

Regulatory and trade complexity: Regional chemical regulations and trade measures are altering cost-to-serve and certification requirements. Examples affecting formulation choices and market entry are already in force and will influence 2026 commercialization strategies.

This study is purpose-built for executives who must convert market intelligence into operational choices for 2026. The report goes beyond high-level forecast charts to include:

End-to-end demand-supply model calibrated to 2025 base-year performance, with scenario outputs for downside, base, and upside cases covering 2026–2032.

Supplier and product scorecards that benchmark quality, capacity, regulatory readiness, and customer reach across the competitive set, enabling rapid sourcing decisions.

Practical capex and inventory stress-tests: dynamic templates to size production investments and buffer inventories under alternate demand and raw-material cost scenarios.

Commercial playbooks for route-to-market decisions, including value-based pricing templates, margin waterfall analysis, and contract-clause templates to protect against feedstock volatility.

Regulatory compliance checklists and a policy watch that translate EU and other jurisdictional controls into product, labeling, and supply-chain actions.

M&A and partnership playbook: criteria for identifying bolt-on specialty resin targets, integration planning checklists, and synergies quantification templates.

The silicone resin market exhibits a mix of global leaders and specialist regional players — a structure that creates opportunities for scale players and niche innovators alike. Market concentration metrics indicate a materially consolidated top tier (CR3 and CR5 levels consistent with mid-high single digit concentration), which means that while incumbents exert pricing and distribution influence, there remains room for differentiated entrants with technical/ regulatory advantages.

Key players assessed in the report include Dow (Midland, Michigan, USA), Wacker Chemie AG (Munich, Germany), Shin‑Etsu Chemical (Tokyo, Japan), Momentive Performance Materials (Waterford, New York, USA), Elkem ASA (Oslo, Norway), and KCC Corporation (Siheung, South Korea). Each firm exhibits distinct strategic postures: integrated commodity supply, premium specialty offerings for high-temperature or electronic applications, or regionally focused customer intimacy models.

Recent developments highlighted in our competitive analysis have direct implications for 2026 positioning:

Wacker’s capacity expansion in the Netherlands (October 2024) signals continued supplier willingness to invest in coatings-grade volumes — a move that will affect availability windows and negotiation leverage in Europe.

Shin‑Etsu’s launch of a high-heat-resistant grade for automotive electronics (June 2024) illustrates the race to capture electronics encapsulation and EV-related thermal management demand.

Dow’s REACH compliance update (March 2024) reflects proactive regulatory risk management that facilitates easier market access across tightly regulated regions.

Secure upstream feedstock and institute dynamic hedging. Given recent metallic silicon cost pressure, procurement teams should combine multi-year supply agreements with indexed pass-through clauses and defined minimum/maximum volumes to maintain flexibility.

Accelerate product differentiation toward regulated, high-value niches. Invest selectively in formulations that preempt regulatory headwinds (e.g., minimizing restricted cyclic siloxane content) and enable premium pricing in electronics and high-temperature coatings.

Reconfigure footprint around tariff and logistics realities. Tariff exposures and amended international transport codes require a reassessment of regional manufacturing and distribution nodes; nearshoring or regional stocking hubs can materially reduce landed cost volatility.

Operationalize regulatory readiness. Introduce cross-functional compliance gates (R&D → commercialization) to ensure new grades meet regional chemical and environmental standards without time-to-market penalties.

Pursue targeted M&A to buy capability, not volume. The optimal 2026 acquisition targets are specialty resin technologies, formulation IP, and customer-contracted supply arrangements rather than large-scale commodity capacity.

Run a 90-day supplier resilience audit: identify top-10 single points of failure, validate second-source feasibility, and commit to contingency stock levels tied to lead-time metrics.

Deploy the report’s pricing model across key accounts: stress-test existing contracts with 15–18 month feedstock volatility scenarios and define escalation triggers tied to objective indices.

Fast-track two product pilots that address high-growth applications (e.g., electronics encapsulation, high-temperature clearcoats), with regulatory pre-certification pathways mapped out.

Implement logistics mitigations aligned with IMDG amendments: update labeling, documentation, and training to avoid shipment delays and non-compliance penalties.

CEOs and strategy teams: Use the scenario engine to set capital allocation and M&A priorities for 2026–2028 based on credible upside and downside demand cases.

CPOs and procurement: Use supplier scorecards and hedging templates to reduce cost volatility and secure critical feedstock.

R&D and product managers: Apply the regulatory watch and formulation playbooks to accelerate compliant specialty grades to market.

Commercial teams: Implement value-based pricing and customer segmentation tools to capture margin in growth pockets while protecting volume in price-sensitive segments.

Regulatory limits on certain cyclic siloxanes and scrutiny around fluorinated chemistries affect formulation choices and green-building certification ability; companies must map product claims to regional standards before market launch.

Existing trade measures impose material differential costs depending on origin and destination; supply footprint and supplier selection should internalize these duties when modeling landed cost.

New transport labeling requirements for certain resin classifications require immediate updates to shipping and safety documentation to avoid operational holds at ports.

PW Consulting’s Silicone Resin Market report is designed as a tactical guide for 2026 decision-making: it converts a clear, data-backed growth outlook — from a USD 5,520.0 million market in 2025 to a projected USD 8,421.4 million by 2032 at a 6.22% CAGR (2026–2032) — into concrete, executable steps for procurement, product development, commercial, and corporate development teams.

We intentionally present the intellectual architecture and decision tools in this briefing while reserving full subsegment-level tables, granular regional allocations, and supplier-specific numeric market shares for the full report. This “trailer” approach demonstrates the report’s depth and immediate utility and directs practitioners to the full deliverable for transaction-grade inputs.

Leaders who need to convert 2026 plans into defensible actions should consult the full PW Consulting report for the complete dataset, downloadable models, and supplier scorecards that underpin the recommendations in this briefing. For access to the full intelligence package and bespoke advisory support, please visit PW Consulting’s report page or contact our industry team for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Silicone Resin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com